Visualizing Price Scenarios

06 Jun 2015To install Systematic Investor Toolbox (SIT) please visit About page.

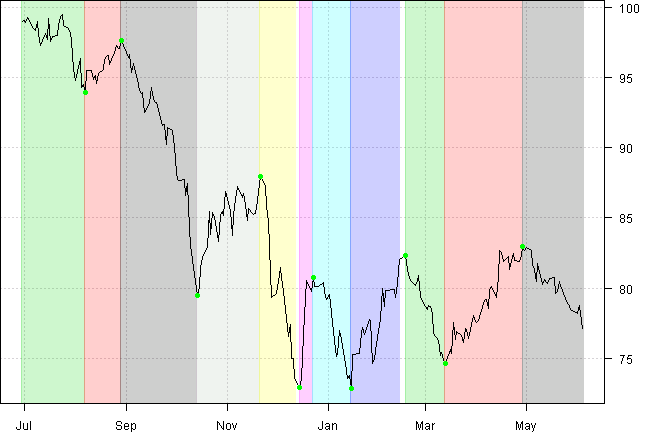

Newfound Research shared an interesting post: Volatility Through a Different Lens that features a chart of Sector Energy ETF(XLE) with historical price scenarios highlighted with various colors.

This reminded me of the post i wrote back in 2012: Classical Technical Patterns Below I will use same machinery to automatically find scenarios in historical price data.

#*****************************************************************

# Load historical data

#*****************************************************************

library(SIT)

load.packages('quantmod')

ticker = 'XLE'

data = env()

getSymbols.extra(ticker, src = 'yahoo', from = '1970-01-01', env = data, set.symbolnames = T, auto.assign = T)

for(i in data$symbolnames) data[[i]] = adjustOHLC(data[[i]], use.Adjusted=T)

bt.prep(data, align='remove.na', fill.gaps = T)

#*****************************************************************

# Find extrema

#*****************************************************************

sample = data$XLE['2014:06:30::2015:06:04']

load.packages('sm')

# find extrema

obj = find.extrema( Cl(sample) )

mhat.extrema.loc = obj$mhat.extrema.loc

extrema.dir = obj$extrema.dir

#*****************************************************************

# Map extrema to data

#*****************************************************************

x = Cl(sample)

n = len(x)

temp = c(1, mhat.extrema.loc, n)

loc = mhat.extrema.loc

for(i in 2:(len(temp)-1)) {

index = round(temp[i] - (temp[i] - temp[i-1]) / 2) : round(temp[i] + (temp[i+1] - temp[i]) / 2)

loc[i-1] = index[1] - 1 + iif(extrema.dir[i-1] > 0, which.max(x[index]), which.min(x[index]))

}

# do not allow extrema at the boundaries

margin = min(10, round(n * 0.1))

loc = loc[ loc >= margin & loc <= (n-margin)]

print(index(sample[loc]))2014-08-07 2014-08-29 2014-10-14 2014-11-21 2014-12-15 2014-12-23 2015-01-15 2015-02-17 2015-03-13 2015-04-29

#*****************************************************************

# Plot

#*****************************************************************

highlight = sample[,1] * NA

highlight[loc] = len(loc):1

highlight[1] = len(loc) + 1

dates = highlight[!is.na(highlight)]

highlight[] = ifna.prev(highlight)

plota(sample)

col = col.add.alpha(highlight, 50)

plota.x.highlight(highlight, highlight != 0, col)

plota.lines(sample)

plota.lines(sample[loc], type='p', col='green', lwd=1, pch=19)

#*****************************************************************

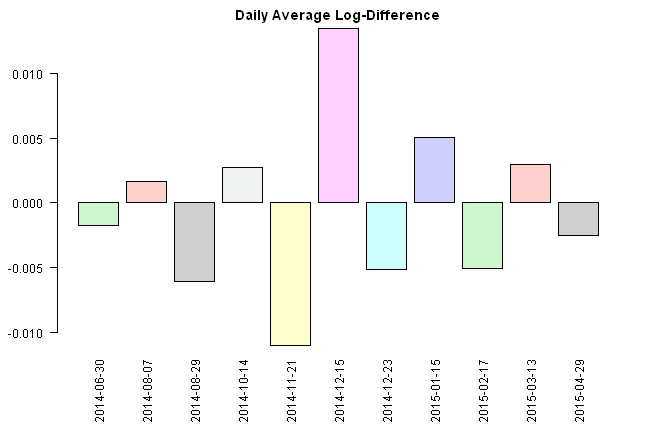

# Compute Daily Average Log-Difference

#*****************************************************************

ret = diff(log(Cl(sample)))

stat = tapply(ret, highlight, mean, na.rm=T)

temp = data.frame(date = index(dates), col=as.vector(dates), stat = stat[match(dates, names(stat))])

temp = na.omit(temp)

par(mar = c(6, 4, 2, 2))

barplot(temp$stat, col=col.add.alpha(temp$col, 50), names.arg=temp$date, las=2, main='Daily Average Log-Difference')

#*****************************************************************

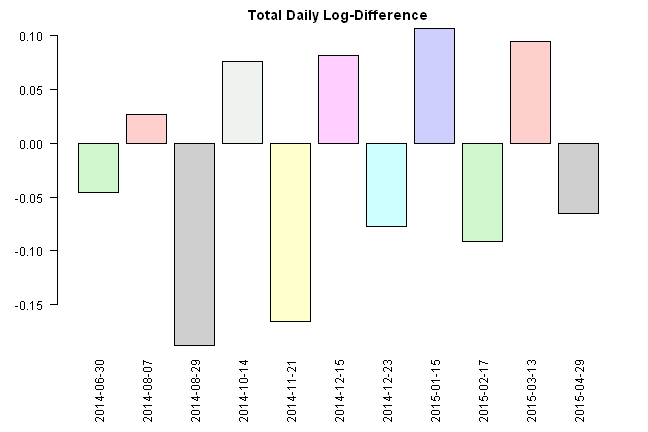

# Compute Total Daily Log-Difference

#*****************************************************************

stat = tapply(ret, highlight, sum, na.rm=T)

temp = data.frame(date = index(dates), col=as.vector(dates), stat = stat[match(dates, names(stat))])

temp = na.omit(temp)

par(mar = c(6, 4, 2, 2))

barplot(temp$stat, col=col.add.alpha(temp$col, 50), names.arg=temp$date, las=2, main='Total Daily Log-Difference')

(this report was produced on: 2015-06-07)