Regime Detection Update

04 Jan 2015To install Systematic Investor Toolbox (SIT) please visit About page.

I did series of posts about Regime Detection using RHmm sometime ago. Unfortunately, the RHmm is no longer available from CRAN, so I want to update the repository location for RHmm package, and also replicate functionality with depmixS4 package. The depmixS4 package also allows linear constraints on parameters.

Summary:

- RHmm is available at R-Forge

- For more info about depmixS4 package, please have a look at Getting Started with Hidden Markov Models in R

Please see below updated code for the bt.regime.detection.test() function in bt.test.r at github:

library(SIT)

load.packages('quantmod')

###############################################################################

# Regime Detection

# http://blogs.mathworks.com/pick/2011/02/25/markov-regime-switching-models-in-matlab/

###############################################################################

#bt.regime.detection.test <- function()

#*****************************************************************

# Generate data as in the post

#******************************************************************

bull1 = rnorm( 100, 0.10, 0.15 )

bear = rnorm( 100, -0.01, 0.20 )

bull2 = rnorm( 100, 0.10, 0.15 )

true.states = c(rep(1,100),rep(2,100),rep(1,100))

returns = c( bull1, bear, bull2 )

# find regimes

load.packages('RHmm', repos ='http://R-Forge.R-project.org')

y=returns

ResFit = HMMFit(y, nStates=2)

VitPath = viterbi(ResFit, y)DimObs=1

# HMMGraphicDiag(VitPath, ResFit, y)

# HMMPlotSerie(y, VitPath)

#Forward-backward procedure, compute probabilities

fb = forwardBackward(ResFit, y)

# Plot probabilities and implied states

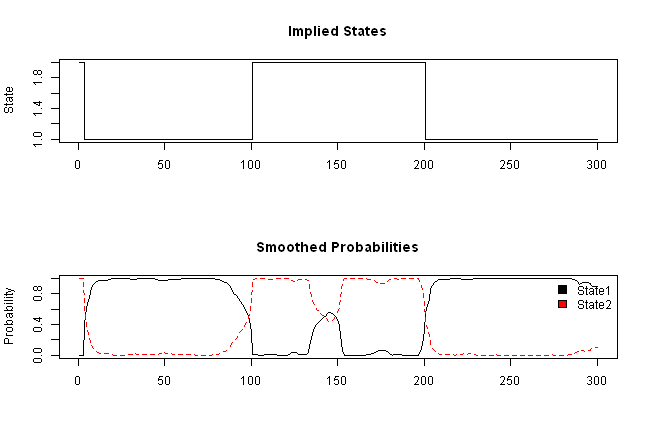

layout(1:2)

plot(VitPath$states, type='s', main='Implied States', xlab='', ylab='State')

matplot(fb$Gamma, type='l', main='Smoothed Probabilities', ylab='Probability')

legend(x='topright', c('State1','State2'), fill=1:2, bty='n')

# http://lipas.uwasa.fi/~bepa/Markov.pdf

# Expected duration of each regime (1/(1-pii))

#1/(1-diag(ResFit$HMM$transMat))

#*****************************************************************

# It also can be done using depmixS4 package

#[Getting Started with Hidden Markov Models in R](http://blog.revolutionanalytics.com/2014/03/r-and-hidden-markov-models.html)

#******************************************************************

load.packages('depmixS4')

# Construct and fit a regime switching model

mod = depmix(y ~ 1, family = gaussian(), nstates = 2, data=data.frame(y=y))

fm2 = fit(mod, verbose = FALSE)converged at iteration 69 with logLik: 125.6168

probs = posterior(fm2)

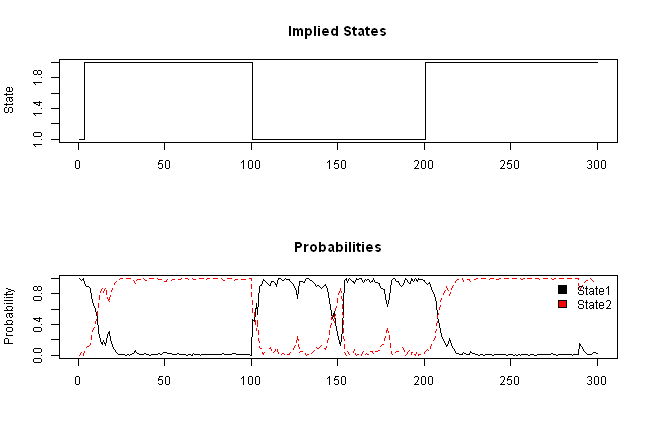

layout(1:2)

plot(probs$state, type='s', main='Implied States', xlab='', ylab='State')

matplot(probs[,-1], type='l', main='Probabilities', ylab='Probability')

legend(x='topright', c('State1','State2'), fill=1:2, bty='n')

#*****************************************************************

# Add some data and see if the model is able to identify the regimes

#******************************************************************

bear2 = rnorm( 100, -0.01, 0.20 )

bull3 = rnorm( 100, 0.10, 0.10 )

bear3 = rnorm( 100, -0.01, 0.25 )

true.states = c(true.states, rep(2,100),rep(1,100),rep(2,100))

y = c( bull1, bear, bull2, bear2, bull3, bear3 )

VitPath = RHmm:::viterbi(ResFit, y)$statesDimObs=1

# map states: sometimes HMMFit function does not assign states consistently

# let's use following formula to rank states

# i.e. high risk, low returns => state 2 and low risk, high returns => state 1

map = rank(sqrt(ResFit$HMM$distribution$var) - ResFit$HMM$distribution$mean)

VitPath = map[VitPath]

#*****************************************************************

# Plot regimes

#******************************************************************

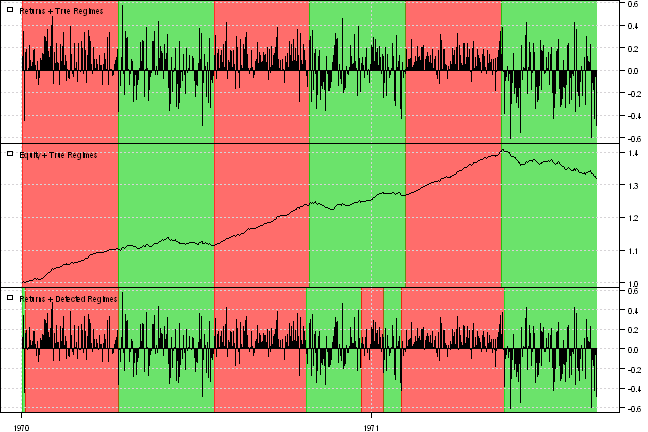

data = xts(y, as.Date(1:len(y)))

layout(1:3)

plota.control$col.x.highlight = col.add.alpha(true.states+1, 150)

plota(data, type='h', plotX=F, x.highlight=T)

plota.legend('Returns + True Regimes')

plota(cumprod(1+data/100), type='l', plotX=F, x.highlight=T)

plota.legend('Equity + True Regimes')

plota.control$col.x.highlight = col.add.alpha(VitPath+1, 150)

plota(data, type='h', x.highlight=T)

plota.legend('Returns + Detected Regimes')

Identifying Changing Market Conditions by Tad Slaff made a great tutorial on Hidden Markov Models using depmixS4 package.

#*****************************************************************

# Load historical prices

#******************************************************************

data = env()

getSymbols('SPY', src = 'yahoo', from = '1970-01-01', env = data, auto.assign = T)

price = Cl(data$SPY)

open = Op(data$SPY)

ret = diff(log(price))

ret = log(price) - log(open)

atr = ATR(HLC(data$SPY))[,'atr']

#*****************************************************************

# Construct and fit a regime switching model

#******************************************************************

load.packages('depmixS4')

index = 14:nrow(price)

temp = data.frame(ret=as.vector(ret), atr=as.vector(atr))

temp = temp[index,]

# We're setting the LogReturns and ATR as our response variables,

# want to set 4 different regimes, and setting the response distributions to be gaussian.

mod = depmix(list(ret~1, atr~1),data=temp,nstates=4,family=list(gaussian(),gaussian()))

fm2 = fit(mod, verbose = FALSE)converged at iteration 30 with logLik: 18358.98

print(summary(fm2))Initial state probabilties model pr1 pr2 pr3 pr4 0 0 1 0

Transition matrix toS1 toS2 toS3 toS4 fromS1 9.821940e-01 1.629595e-02 1.510069e-03 8.514403e-45 fromS2 1.167011e-02 9.790209e-01 8.775478e-68 9.308946e-03 fromS3 3.266616e-03 8.586650e-47 9.967334e-01 1.350529e-69 fromS4 3.608394e-65 1.047516e-02 1.922545e-130 9.895248e-01

Response parameters Resp 1 : gaussian Resp 2 : gaussian Re1.(Intercept) Re1.sd Re2.(Intercept) Re2.sd St1 2.897594e-04 0.006285514 1.1647547 0.1181514 St2 -6.980187e-05 0.008186433 1.6554049 0.1871963 St3 2.134584e-04 0.005694483 0.4537498 0.1564576 St4 -4.459161e-04 0.015419207 2.7558362 0.7297283

| Re1.(Intercept) | Re1.sd | Re2.(Intercept) | Re2.sd | |

|---|---|---|---|---|

| St1 | 0.000289759401378951 | 0.00628551404616354 | 1.16475474419891 | 0.118151350440916 |

| St2 | -6.98018749098021e-05 | 0.00818643307634358 | 1.65540488736983 | 0.187196307284941 |

| St3 | 0.000213458358141314 | 0.00569448330115608 | 0.453749781945066 | 0.156457606460757 |

| St4 | -0.00044591612667264 | 0.0154192070819596 | 2.75583620018895 | 0.72972830143278 |

probs = posterior(fm2)

print(head(probs))| rownames(x) | state | S1 | S2 | S3 | S4 |

|---|---|---|---|---|---|

| 1 | 3 | 0 | 0 | 1 | 0 |

| 2 | 3 | 0 | 0 | 1 | 0 |

| 3 | 3 | 0 | 0 | 1 | 0 |

| 4 | 3 | 0 | 0 | 1 | 0 |

| 5 | 3 | 0 | 0 | 1 | 0 |

| 6 | 3 | 0 | 0 | 1 | 0 |

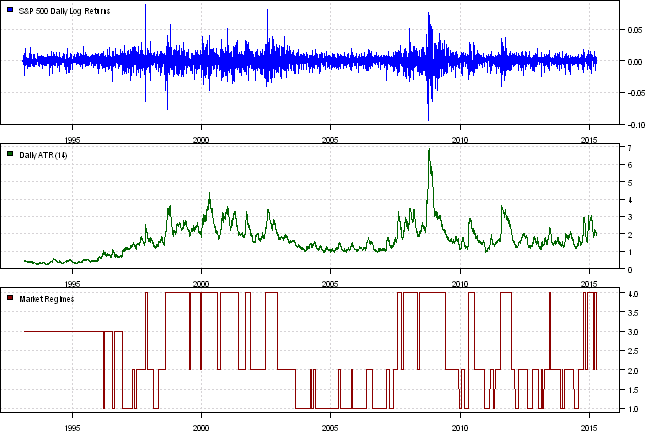

layout(1:3)

plota(ret, type='h', col='blue')

plota.legend('S&P 500 Daily Log Returns', 'blue')

plota(atr, type='l', col='darkgreen')

plota.legend('Daily ATR(14)', 'darkgreen')

temp = NA * price

temp[index] = probs$state

plota(temp, type='l', col='darkred')

plota.legend('Market Regimes', 'darkred')

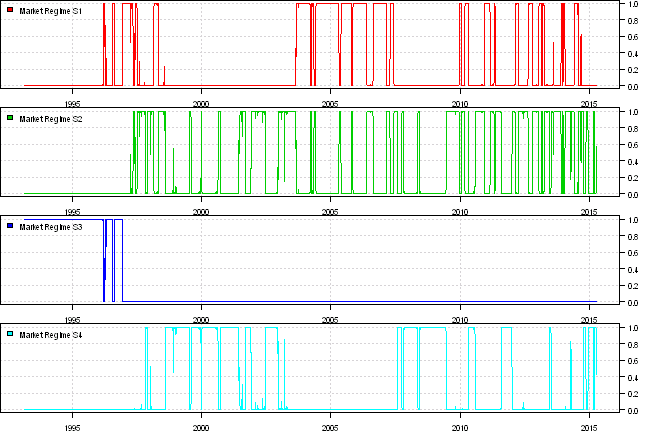

layout(1:4)

for(i in 2:5) {

temp = NA * price

temp[index] = probs[,i]

plota(temp, type='l', col=i)

plota.legend(paste('Market Regime', colnames(probs)[i]), i)

}

Please note that solution changes each time you run the above code.

(this report was produced on: 2015-04-17)