FX and Stop Loss

04 Nov 2014To install Systematic Investor Toolbox (SIT) please visit About page.

Tad Slaff at InovanceTech published We’re going to explore the backtesting capabilities of R post that I like. Below I will explore it a bit more.

Load Historical Prices. Let’s start with USD/CAD 4 hour bar pricesdropbox.

#*****************************************************************

# Load historical data

#******************************************************************

library(SIT)

load.packages('quantmod')

data <- new.env()

data$USDCAD = read.xts('data/USDCAD.csv', format='%m/%d/%y %H:%M', index.class = c("POSIXlt", "POSIXt"))

#plota(data$USDCAD, type='l')

bt.prep(data, align='remove.na')

if (FALSE) {

tickers = spl('USDCAD')

data <- new.env()

getSymbols.fxhistoricaldata(tickers, 'hour', data,

download=F, name.has.type = FALSE)

bt.prep(data, align='remove.na', dates='1990::')

} Create Strategies

#*****************************************************************

# Code Strategies

#******************************************************************

prices = data$prices

models = list()

dates = '2001::'

#*****************************************************************

# Code Strategies: Buy and Hold

#******************************************************************

data$weight[] = NA

data$weight[] = 1

models$Buy.Hold = bt.run.share(data, dates=dates, silent=T, clean.signal=T)

#*****************************************************************

# Code Strategies: Long

#******************************************************************

#Calculate the indicators we need for our strategy

CCI20 = CCI(prices,20)

RSI3 = RSI(prices,3)

DEMA10 = DEMA(prices,n = 10, v = 1, wilder = FALSE)

DEMA10c = prices - DEMA10

DEMA10c = DEMA10c/.0001

buy.signal = ifelse(RSI3 < 30 & CCI20 > -290 & CCI20 < -100 & DEMA10c > -40 & DEMA10c < -20,1,NA)

#Set our long entry conditions found by our algorithms and optimized by us in the last post

data$weight[] = NA

data$weight[] = buy.signal

models$Long = bt.run.share(data, dates=dates, trade.summary = TRUE, silent=T, clean.signal=T)

#*****************************************************************

# Code Strategies: Short

#******************************************************************

sell.signal<-ifelse(DEMA10c > 10 & DEMA10c < 40 & CCI20 > 185 & CCI20 < 325 & RSI3 > 50, -1 ,NA)

data$weight[] = NA

data$weight[] = sell.signal

models$Short = bt.run.share(data, dates=dates, trade.summary = TRUE, silent=T, clean.signal=T)

long.short.strategy<-iif(RSI3 < 30 & CCI20 > -290 & CCI20 < -100 & DEMA10c > -40 & DEMA10c < -20,1,iif(DEMA10c > 10 & DEMA10c < 40 & CCI20 > 185 & CCI20 < 325 & RSI3 > 50, -1 ,NA))

data$weight[] = NA

data$weight[] = long.short.strategy

models$Long.Short = bt.run.share(data, dates=dates, trade.summary = TRUE, silent=T, clean.signal=T)

#*****************************************************************

# Create Reprot

#******************************************************************

#Isolate the dates from our validation set (The data not used to train the model or create the rules, our out-of-sample test)

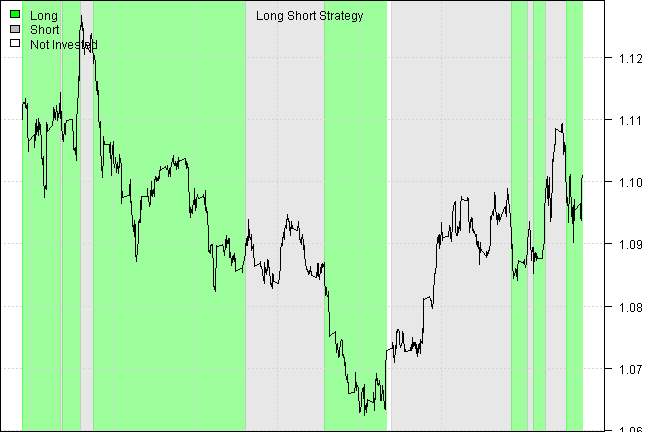

dates = '2014-02-26::2014-09-22'

bt.stop.strategy.plot(data, models$Long.Short, dates = dates, layout=T, main = 'Long Short Strategy', plotX = F)

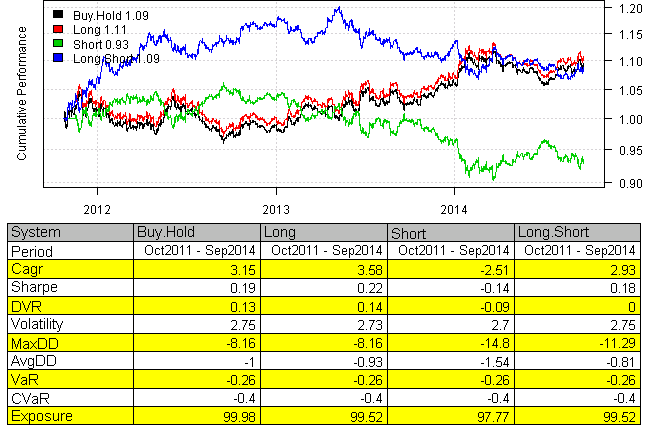

strategy.performance.snapshoot(models, T) NULL

NULL

(this report was produced on: 2014-12-07)