Volatility Strategy from TradingTheOdds

23 Nov 2014To install Systematic Investor Toolbox (SIT) please visit About page.

Today I want to look at the following posts:

- DDNs Volatility Risk Premium Strategy Revisited (2)

- Volatility Risk Premium Trading Volatility (Part I)

- Volatility Risk Premium: Sharpe 2+, Return to Drawdown 3+

- Chasing the Volatility Risk Premium

- Easy Volatility Investing by Tony Cooper at Double-Digit Numerics

Helmuth Vollmeier You can download a “long” XIV and “long” VXX back to the start of VIX futures 2004 from my Dropbox which is updated daily with CSI data via a small R-script. VXX: https://dl.dropboxusercontent.com/s/950x55x7jtm9x2q/VXXlong.TXT XIV: https://dl.dropboxusercontent.com/s/jk6der1s5lxtcfy/XIVlong.TXT

Ilya , Samuel update: ZIV & VXZ, reconstructed according to the method outlined in their prospectus VXZ: https://www.dropbox.com/s/y3cg6d3vwtkwtqx/VXZlong.TXT ZIV: https://www.dropbox.com/s/jk3ortdyru4sg4n/ZIVlong.TXT

Load historical data for SPY and TLT, and align it, so that dates on both time series match. We also adjust data for stock splits and dividends.

#*****************************************************************

# Load historical data

#*****************************************************************

library(SIT)

load.packages('quantmod')

tickers = spl('GSPC=^GSPC,VXMT+^VIX,VXX+VXX.LONG,XIV+XIV.LONG')

raw.data <- new.env()

raw.data$VXX.LONG = make.stock.xts(read.xts("data/VXXlong.TXT", format='%Y-%m-%d'))

raw.data$XIV.LONG = make.stock.xts(read.xts("data/XIVlong.TXT", format='%Y-%m-%d'))

# http://www.cboe.com/publish/ScheduledTask/MktData/datahouse/vxmtdailyprices.csv

raw.data$VXMT = make.stock.xts(read.xts("data/vxmtdailyprices.csv", skip=2, format='%m/%d/%Y'))

# tickers = spl('GSPC=^GSPC,VXMT+^VIX,VXX=VXX.LONG,XIV=XIV.LONG')

data <- new.env()

getSymbols.extra(tickers, src = 'yahoo', from = '1970-01-01', env = data, raw.data = raw.data, auto.assign = T)

for(i in ls(data)) data[[i]] = adjustOHLC(data[[i]], use.Adjusted=T)

bt.prep(data, align='remove.na')

bt.start.dates(data) Start XIV "2004-03-29" GSPC "2004-03-29" VXX "2004-03-29" VXMT "2004-03-29"

Next let’s compute statistics and trading signal.

prices = data$prices

spyRets = diff(log(prices$GSPC))

spyVol = runSD(spyRets, n=2)

SPY.VOL = spyVol*100*sqrt(252)

SMA.VOL = SMA(prices$VXMT - SPY.VOL, n=5)

signal = SMA.VOL > 0Now we ready to back-test our strategy:

#*****************************************************************

# Code Strategies

#*****************************************************************

models = list()

data$weight[] = NA

data$weight$XIV = iif(signal, 1, 0)

data$weight$VXX = iif(signal, 0, 1)

models$strategy = bt.run.share(data, clean.signal=F, silent=T)

data$weight[] = NA

data$weight$XIV = iif(signal, 1, 0)

data$weight$VXX = iif(signal, 0, 1)

models$strategy1 = bt.run.share(data, do.lag=2, clean.signal=F, silent=T)and create reports

Create Report:

#*****************************************************************

# Create Report

#*****************************************************************

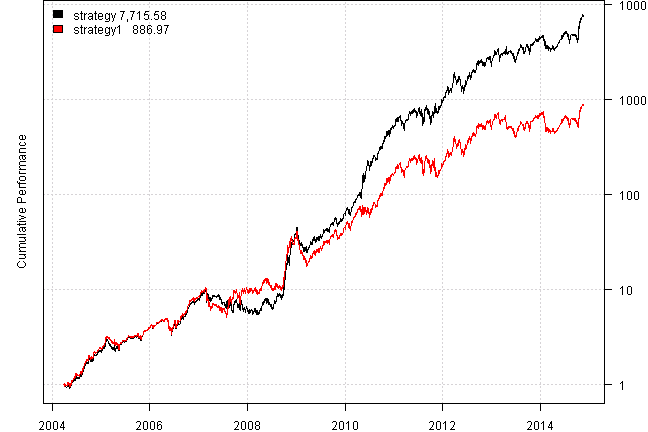

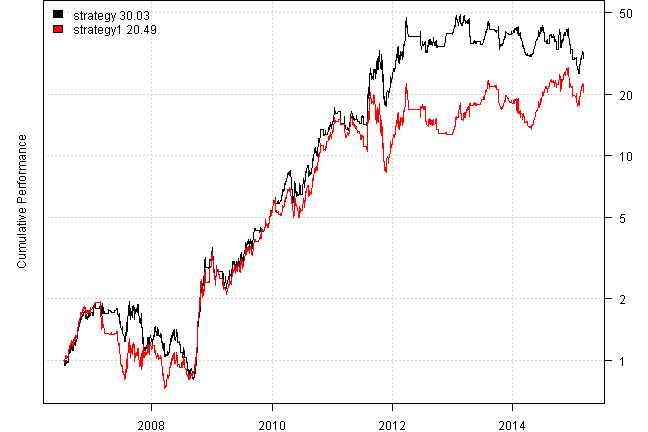

plotbt(models, plotX = T, log = 'y', LeftMargin = 3, main = NULL)

mtext('Cumulative Performance', side = 2, line = 1)

print(plotbt.strategy.sidebyside(models, make.plot=F, return.table=T))| strategy | strategy1 | |

|---|---|---|

| Period | Mar2004 - Nov2014 | Mar2004 - Nov2014 |

| Cagr | 131.66 | 89.09 |

| Sharpe | 1.8 | 1.43 |

| DVR | 1.15 | 1.06 |

| Volatility | 55.29 | 55.41 |

| MaxDD | -45.64 | -56.77 |

| AvgDD | -6.6 | -6.91 |

| VaR | -5.71 | -5.76 |

| CVaR | -8.11 | -8.38 |

| Exposure | 99.96 | 99.93 |

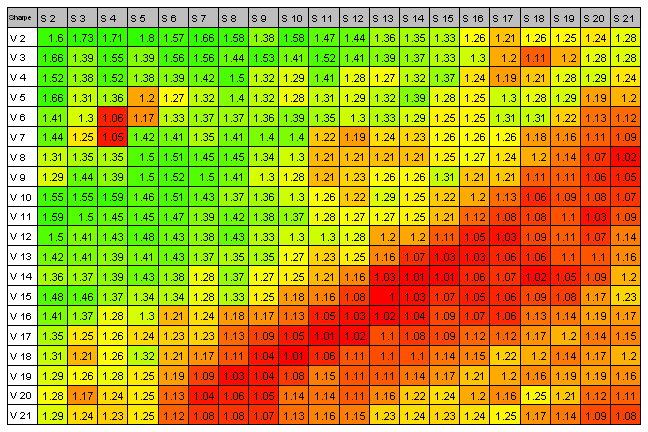

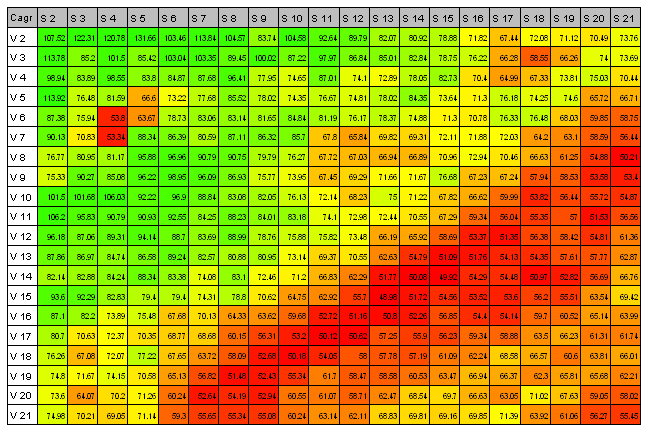

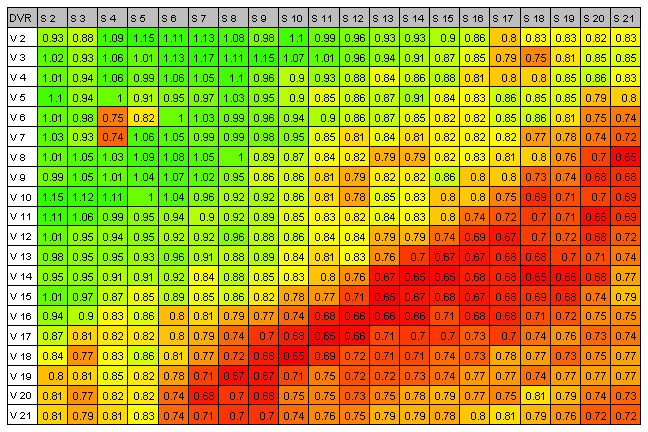

Next, sensetivity analysis:

models = list()

sma.lens = 2:21

vol.lens = 2:21

if(F) {

tic(10)

#*****************************************************************

# Sensitivity Analysis

#******************************************************************

for(n.vol in vol.lens) {

spyVol = runSD(spyRets, n=n.vol)

SPY.VOL = spyVol*100*sqrt(252)

for(n.sma in sma.lens) {

SMA.VOL = SMA(prices$VXMT - SPY.VOL, n=n.sma)

signal = SMA.VOL > 0

data$weight[] = NA

data$weight$XIV = iif(signal, 1, 0)

data$weight$VXX = iif(signal, 0, 1)

models[[ paste(n.sma, n.vol) ]] = bt.run.share(data, clean.signal=F, silent=T)

}

}

toc(10)

}

tic(11)

#*****************************************************************

# Sensitivity Analysis Cluster

#******************************************************************

run.backtest <- function(n.vol) {

models = list()

spyVol = runSD(spyRets, n=n.vol)

SPY.VOL = spyVol*100*sqrt(252)

for(n.sma in sma.lens) {

SMA.VOL = SMA(data$prices$VXMT - SPY.VOL, n=n.sma)

signal = SMA.VOL > 0

data$weight[] = NA

data$weight$XIV = iif(signal, 1, 0)

data$weight$VXX = iif(signal, 0, 1)

models[[ paste(n.sma, n.vol) ]] = bt.run.share(data, clean.signal=F, silent=T)

}

# serialize and compress first

models

}

#*****************************************************************

# Run Cluster

#*****************************************************************

load.packages('parallel')

cl = setup.cluster(varlist='spyRets,sma.lens,data,run.backtest',envir=environment())

out = clusterApplyLB(cl, vol.lens, function(j) { run.backtest(j) } )

stopCluster(cl)

models = do.call(c, out)

toc(11) Elapsed time is 18.29 seconds

#*****************************************************************

# Create Report

#******************************************************************

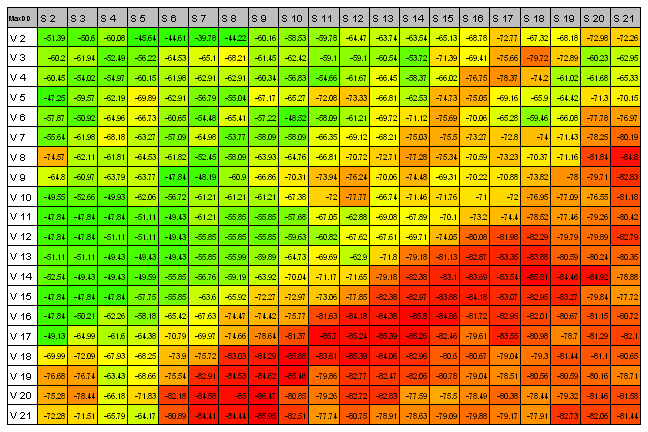

out = plotbt.strategy.sidebyside(models, return.table=T, make.plot = F)

# allocate matrix to store backtest results

dummy = matrix('', len(vol.lens), len(sma.lens))

colnames(dummy) = paste('S', sma.lens)

rownames(dummy) = paste('V', vol.lens)

names = spl('Sharpe,Cagr,DVR,MaxDD')

for(i in names) {

dummy[] = ''

for(n.vol in vol.lens)

for(n.sma in sma.lens)

dummy[ paste('V', n.vol), paste('S', n.sma)] =

out[i, paste(n.sma, n.vol) ]

print(i, ':')

plot.table(dummy, smain = i, highlight = T, colorbar = F)

}Sharpe :

Cagr :

DVR :

MaxDD :

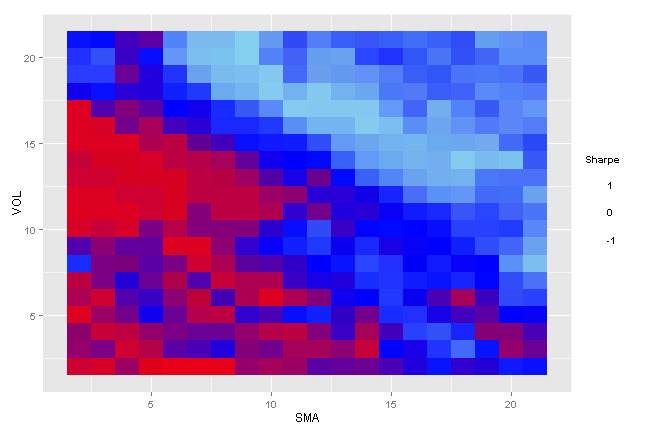

load.packages('ggplot2,reshape2')

plot.data = melt(dummy)

colnames(plot.data) = c("vol", "sma", "Sharpe")

plot.data$SMA = as.numeric(gsub("S", "", plot.data$sma))

plot.data$VOL = as.numeric(gsub("V", "", plot.data$vol))

plot.data$Sharpe = scale(as.numeric(plot.data$Sharpe))

ggplot(plot.data, aes(x=SMA, y=VOL, fill=Sharpe))+

geom_tile()+

scale_fill_gradient2(high="skyblue", mid="blue", low="red")

Helmuth Vollmeier says my app The strategy employs a SINGLE variable (the SMA of a ratio of 2 points on the term structure). The strategy is robust over the whole range. Even if you want there is almost no way to get a mediocre performance ! No clever optimization will change this fact. To ‘harvest’ the premium I think the simplest strategies are the most efficient,

A side note concerning the entry : an entry on the NEXT close is even more profitable than entering on the close ( there is some short term mean-reversion)

90 days sma

vxx xiv ratio ma action ret2014-11-13 0.0103 -0.0128 0.8942 0.9162 -1 -0.0128 2014-11-14 0.0032 -0.0024 0.9002 0.9162 -1 -0.0024 2014-11-17 -0.0021 0.0024 0.8949 0.9162 -1 0.0024 2014-11-18 -0.0175 0.0167 0.89 0.9162 -1 0.0167 2014-11-19 0.0242 -0.0244 0.8917 0.9161 -1 -0.0244 2014-11-20 -0.0104 0.0101 0.8939 0.9163 -1 0.0101

delta (term structure slope) = VIX - VXV

load.packages('quantmod')

tickers = spl('VIX=^VIX,VXV=^VXV,VXX+VXX.LONG,XIV+XIV.LONG')

raw.data <- new.env()

raw.data$VXX.LONG = make.stock.xts(read.xts("data/VXXlong.TXT", format='%Y-%m-%d'))

raw.data$XIV.LONG = make.stock.xts(read.xts("data/XIVlong.TXT", format='%Y-%m-%d'))

data <- new.env()

getSymbols.extra(tickers, src = 'yahoo', from = '1970-01-01', env = data, raw.data = raw.data, auto.assign = T)

for(i in ls(data)) data[[i]] = adjustOHLC(data[[i]], use.Adjusted=T)

# data.CBOE = load.VXX.CBOE()

# futures = extract.VXX.CBOE(data.CBOE, 'Settle', 1:7)

# data$ratio = make.xts(futures[,2]/futures[,5],data.CBOE$dates)

# data$ratio[1:max(which(is.na(data$ratio)))] = NA

bt.prep(data, align='remove.na')

bt.start.dates(data)Start XIV "2006-07-17" VIX "2006-07-17" VXV "2006-07-17" VXX "2006-07-17"

prices = data$prices

ret = prices / mlag(prices) - 1

#last(round(cbind(ret$VXX, ret$XIV, data$ratio),4),6)

#last(round(cbind(ret$VXX, ret$XIV, prices$VIX / prices$VXV),4),7)

data$ratio = prices$VIX / prices$VXV

sma = SMA(data$ratio, 90)

signal = iif(data$ratio > sma, iif(data$ratio > 1, 1, 0), iif(data$ratio < 1, -1, 0))

# write.xts(cbind(prices$VXX / mlag(prices$VXX) - 1,

# prices$XIV / mlag(prices$XIV) - 1,

# data$ratio, sma, signal), '1.csv')

#*****************************************************************

# Code Strategies

#*****************************************************************

models = list()

data$weight[] = NA

data$weight$VXX = iif(signal == 1, 1, 0)

data$weight$XIV = iif(signal == -1, 1, 0)

models$strategy = bt.run.share(data, clean.signal=F, silent=T)

data$weight[] = NA

data$weight$VXX = iif(signal == 1, 1, 0)

data$weight$XIV = iif(signal == -1, 1, 0)

models$strategy1 = bt.run.share(data, do.lag=2, clean.signal=F, silent=T)

#*****************************************************************

# Create Report

#*****************************************************************

plotbt(models, plotX = T, log = 'y', LeftMargin = 3, main = NULL)

mtext('Cumulative Performance', side = 2, line = 1)

print(plotbt.strategy.sidebyside(models, make.plot=F, return.table=T))| strategy | strategy1 | |

|---|---|---|

| Period | Jul2006 - Mar2015 | Jul2006 - Mar2015 |

| Cagr | 48.16 | 41.76 |

| Sharpe | 1.05 | 0.96 |

| DVR | 0.87 | 0.85 |

| Volatility | 49.17 | 49.27 |

| MaxDD | -58.71 | -62.21 |

| AvgDD | -8.61 | -9.11 |

| VaR | -5.1 | -4.96 |

| CVaR | -7.75 | -7.63 |

| Exposure | 68.92 | 68.92 |

Investigate:

- http://www.godotfinance.com/pdf/DynamicVIXFuturesVersion2Rev1.pdf

- http://www.godotfinance.com/workingpapers/

Good way to use this high performance strategy in your portfolio is to balance it with other positions. For example, please see Barbell investing with XIV / SVXY at Don’t Fear the Bear blog

(this report was produced on: 2015-03-12)