Exponentially Weighted Volatility using RCPP

10 Apr 2016To install Systematic Investor Toolbox (SIT) please visit About page.

The Exponentially Weighted Volatility is a measure of volatility that put more weight on the recent observations. We will use following formula to compute the Exponentially Weighted Volatility:

S[t]^2 = SUM (1-a) * a^i * (r[t-1-i] - rhat[t])^2, i=0 … inf

where rhat[t] is the corresponding the Exponentially Weighted mean

rhat[t] = SUM (1-a) * a^i * r[t-1-i], i=0 … inf

For reference on the computations of Exponentially Weighted Volatility please check:

The above formula depends on the full price history at each point in time and took a while to compute. Hence, I want to share how Rcpp and RcppParallel helped to reduce computation time.

I will use a historic dataset of the Foreign Exchange Rates as my testing data.

First we compute average rolling volatility

#*****************************************************************

# Compute Log Returns

#*****************************************************************

ret = diff(log(data$prices))

tic(5)

hist.vol = sqrt(252) * bt.apply.matrix(ret, runSD, n = 200)

toc(5)[1] “Elapsed time is 0.17 seconds\n”

Next, let’s code the Exponentially Weighted logic

# create RCPP functions to compute the Exponentially Weighted Volatility

load.packages('Rcpp')

sourceCpp(code='

#include <Rcpp.h>

using namespace Rcpp;

using namespace std;

// [[Rcpp::plugins(cpp11)]]

//ema[1] = 0

//ema[t] = (1-a)*r[t-1] + (1-a)*a*ema[t-1]

// [[Rcpp::export]]

NumericVector run_ema_cpp(NumericVector x, double ratio) {

auto sz = x.size();

NumericVector res(sz);

int t;

// find start index; first non NA item

for(t = 0; t < sz; t++) {

if(!NumericVector::is_na(x[t])) break;

res[t] = NA_REAL;

}

int start_t = t;

res[start_t] = 0;

for(t = start_t + 1; t < sz; t++) {

res[t] = (1-ratio) * ( x[t-1] + ratio * res[t-1]);

}

return res;

}

//sigma[1] = 0

//sigma[t] = SUM (1-a) * a^i * (r[t-1-i] - rhat[t])^2, i=0 ... inf

// [[Rcpp::export]]

NumericVector run_esd_cpp(NumericVector x, double ratio) {

auto sz = x.size();

NumericVector res(sz);

int t;

// find start index; first non NA item

for(t = 0; t < sz; t++) {

if(!NumericVector::is_na(x[t])) break;

res[t] = NA_REAL;

}

int start_t = t;

double ema = 0;

res[start_t] = 0;

for(t = start_t + 1; t < sz; t++) {

ema = (1-ratio) * ( x[t-1] + ratio * ema);

double sigma = 0;

for(int i = 0; i < (t - start_t); i++) {

sigma += pow(ratio,i) * pow(x[t-1-i] - ema, 2);

}

res[t] = (1-ratio) * sigma;

}

return res;

}

'

)

run.ema = function(x, n, ratio = n/(n+1)) run_ema_cpp(x, ratio)

run.esd = function(x, n, ratio = n/(n+1)) sqrt(run_esd_cpp(x, ratio))

tic(5)

hist.vol.exp = sqrt(252) * bt.apply.matrix(ret, run.esd, n = 60)

toc(5)[1] “Elapsed time is 106.16 seconds\n”

It took a while to execute this code. Fortunately, the code can easily run in parallel. Following is the RcppParallel version.

# create RCPP Parallel function to compute the Exponentially Weighted Volatility

load.packages('RcppParallel')

sourceCpp(code='

#include <Rcpp.h>

using namespace Rcpp;

using namespace std;

// [[Rcpp::plugins(cpp11)]]

// [[Rcpp::depends(RcppParallel)]]

#include <RcppParallel.h>

using namespace RcppParallel;

struct run_esd_helper : public Worker {

// input matrix to read from

const RMatrix<double> mat;

// internal variables

const double ratio;

const int nperiod;

// output matrix to write to

RMatrix<double> rmat;

// initialize from Rcpp input and output matrixes

run_esd_helper(const NumericMatrix& mat, double ratio, int nperiod, NumericMatrix rmat)

: mat(mat), ratio(ratio), nperiod(nperiod), rmat(rmat) { }

// main entry -function call operator that work for the specified range (begin/end)

void operator()(size_t begin, size_t end) {

for (size_t c1 = begin; c1 < end; c1++) {

int t;

// find start index; first non NA item

for(t = 0; t < nperiod; t++) {

if(!NumericVector::is_na(mat(t, c1))) break;

rmat(t,c1) = NA_REAL;

}

int start_t = t;

double ema = 0;

rmat(start_t, c1) = 0;

for(t = start_t + 1; t < nperiod; t++) {

ema = (1-ratio) * ( mat(t-1,c1) + ratio * ema);

double sigma = 0;

for(int i = 0; i < (t - start_t); i++) {

sigma += pow(ratio,i) * pow(mat(t-1-i,c1) - ema, 2);

}

rmat(t,c1) = (1-ratio) * sigma;

}

}

}

};

// [[Rcpp::export]]

NumericMatrix run_esd_parallel(NumericMatrix mat, double ratio) {

// allocate the matrix we will return

int nc = mat.ncol();

int nperiod = mat.nrow();

NumericMatrix rmat(nperiod, nc);

// parallel run

run_esd_helper p(mat, ratio, nperiod, rmat);

parallelFor(0, nc, p);

return rmat;

}

'

)

run.esd.parallel = function(x, n, ratio = n/(n+1)) { temp=x; x[]=sqrt(run_esd_parallel(x, ratio)); return(x) }

tic(5)

hist.vol.parallel = sqrt(252) * run.esd.parallel(ret, n = 60)

toc(5)[1] “Elapsed time is 14.65 seconds\n”

Great, the running time is more reasonable. Next let’s visualize the impact of using the Exponentially Weighted Volatility

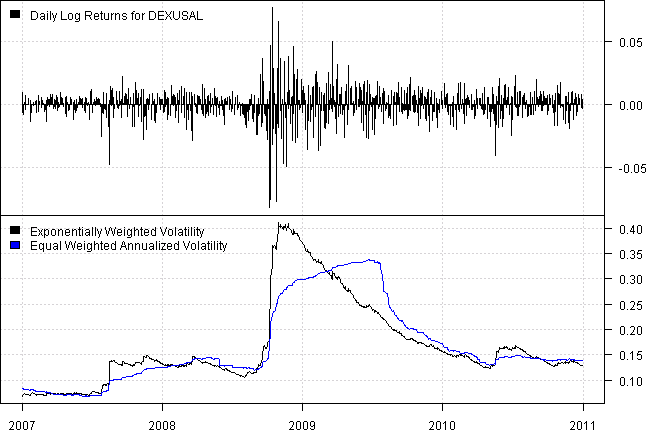

dates = '2007::2010'

layout(1:2)

plota(ret[dates,1],type='h', col='black', plotX=F)

plota.legend(paste('Daily Log Returns for',names(ret)[1]), 'black')

plota(hist.vol.parallel[dates,1],type='l',col='black')

plota.lines(hist.vol[dates,1], col='blue')

plota.legend('Exponentially Weighted Volatility,Equal Weighted Annualized Volatility','black,blue')

As expected, the Exponentially Weighted Volatility puts more weight on most recent observations and is a more reactive risk measure.

For your convenience, the 2016-04-10-Exponentially-Weighted-Volatility-RCPP post source code.