Timing Luck

02 Jan 2015To install Systematic Investor Toolbox (SIT) please visit About page.

There are numerous articles talking about timing luck:

- Luck: The Difference Between Hired or Fired

- The Luck of the Rebalance Timing

- Timing Misfortune Strikes Again: 2013 Ivy10 Portfolio Performance

- Setting Expectations for Monthly Trading Systems

Let’s test concept of trading on different dates by simulating a momentum strategy with various lookbacks that trades on Quarter ends, and compare it to trading with 1/2 months offsets. I.e. let’s simulate trading on the second or third month of the quarter instead of the first month.

Load historical data.

#*****************************************************************

# Load historical data

#*****************************************************************

library(SIT)

load.packages('quantmod')

tickers = spl('DBC,EEM,EWJ,GLD,ICF,IEF,IEV,RWX,TLT,VTI')

data <- new.env()

getSymbols(tickers, src = 'yahoo', from = '1970-01-01', env = data, auto.assign = T)

extend.data.proxy(data)

for(i in ls(data)) data[[i]] = adjustOHLC(data[[i]], use.Adjusted=T)

bt.prep(data, align='remove.na')Let’s define our test strategy:

test.strategy <- function(data, period.ends,

top.n = 3, # number of momentum positions

lookback = 250, # length of momentum look back

lag = 1

){

prices = coredata(data$prices)

momentum = (mlag(prices, lag) / mlag(prices, (lookback + lag)) - 1)

data$weight[] = NA

data$weight[period.ends,] = ntop(momentum[period.ends,],top.n)

data$weight

}Now we ready to back-test our strategy:

#*****************************************************************

# Code Strategies

#*****************************************************************

prices = data$prices

models = list()

period.ends.high = endpoints(prices, 'months')

n.period.ends = len(period.ends.high)

n.high.in.low = 12 # i.e. there are 12 months in 1 year

period.ends.low = endpoints(prices, 'years')

period.ends.low = endpoints(prices, 'quarters')

n.high.in.low = 3 # i.e. there are 3 months in 1 quater

pe = list()

pe[[1]] = which(!is.na( match(period.ends.high, period.ends.low) ))

for (i in 2:n.high.in.low) {

pe[[i]] = pe[[(i-1)]] + 1

pe[[i]] = iif(pe[[i]] > n.period.ends, n.period.ends, pe[[i]])

}

#*****************************************************************

# Code Strategies

#******************************************************************

lookbacks = c(30,120,250)

for (lookback in lookbacks) {

weights = ifna(0 * data$weight, 0)

for (i in 1:n.high.in.low) {

period.offset = i - 1

weight = test.strategy(data, period.ends = period.ends.high[ pe[[i]] ], lookback = lookback)

data$weight[] = weight

models[[paste0('Lookback_', lookback, '_Offset_', period.offset)]] = bt.run.share(data, clean.signal=F, silent=T)

weights = weights + bt.apply.matrix(weight, ifna.prev)/n.high.in.low

}

data$weight[] = weights

models[[paste0('Lookback_',lookback,'_AVG')]] = bt.run.share(data, clean.signal=T, silent=T)

}

#*****************************************************************

# Report

#******************************************************************

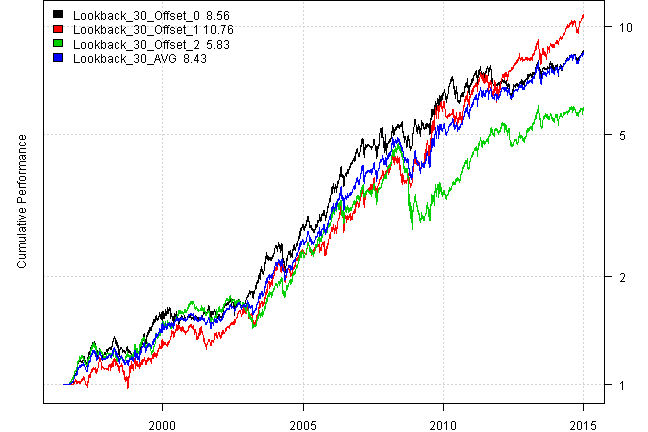

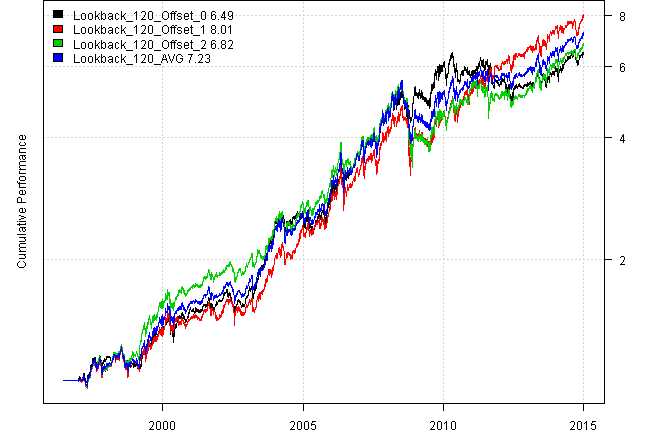

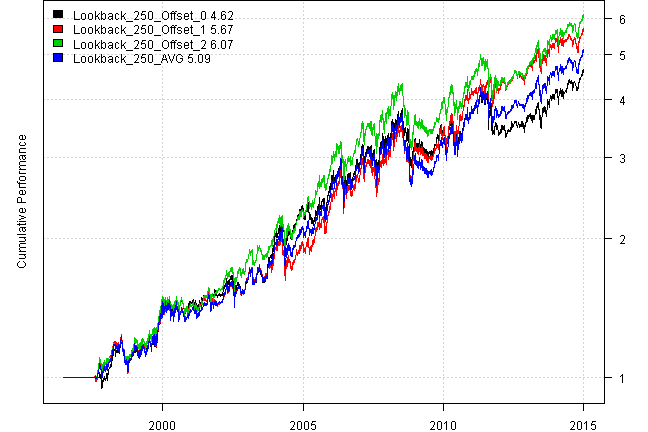

for (lookback in lookbacks) {

print('Lookback', lookback)

models1 = models[grep(paste0('_', lookback, '_'), names(models))]

plotbt(models1, plotX = T, log = 'y', LeftMargin = 3, main = NULL)

mtext('Cumulative Performance', side = 2, line = 1)

print(plotbt.strategy.sidebyside(models1, make.plot=F, return.table=T))

}Lookback 30

| Lookback_30_Offset_0 | Lookback_30_Offset_1 | Lookback_30_Offset_2 | Lookback_30_AVG | |

|---|---|---|---|---|

| Period | Jun1996 - Jan2015 | Jun1996 - Jan2015 | Jun1996 - Jan2015 | Jun1996 - Jan2015 |

| Cagr | 12.29 | 13.69 | 9.99 | 12.2 |

| Sharpe | 0.91 | 0.95 | 0.78 | 1.02 |

| DVR | 0.86 | 0.83 | 0.71 | 0.94 |

| Volatility | 13.92 | 14.9 | 13.67 | 12.17 |

| MaxDD | -19.47 | -20.08 | -42.42 | -23.47 |

| AvgDD | -2.49 | -2.33 | -2.33 | -1.9 |

| VaR | -1.41 | -1.45 | -1.31 | -1.22 |

| CVaR | -2.06 | -2.18 | -2.04 | -1.78 |

| Exposure | 98.61 | 98.11 | 99.04 | 99.04 |

Lookback 120

| Lookback_120_Offset_0 | Lookback_120_Offset_1 | Lookback_120_Offset_2 | Lookback_120_AVG | |

|---|---|---|---|---|

| Period | Jun1996 - Jan2015 | Jun1996 - Jan2015 | Jun1996 - Jan2015 | Jun1996 - Jan2015 |

| Cagr | 10.62 | 11.88 | 10.92 | 11.27 |

| Sharpe | 0.8 | 0.87 | 0.79 | 0.83 |

| DVR | 0.73 | 0.79 | 0.75 | 0.79 |

| Volatility | 14.13 | 14.36 | 14.76 | 14.3 |

| MaxDD | -25.41 | -33.05 | -37.72 | -30.33 |

| AvgDD | -2.79 | -2.6 | -2.55 | -2.6 |

| VaR | -1.46 | -1.45 | -1.49 | -1.49 |

| CVaR | -2.09 | -2.12 | -2.26 | -2.15 |

| Exposure | 97.28 | 96.81 | 96.39 | 97.28 |

Lookback 250

| Lookback_250_Offset_0 | Lookback_250_Offset_1 | Lookback_250_Offset_2 | Lookback_250_AVG | |

|---|---|---|---|---|

| Period | Jun1996 - Jan2015 | Jun1996 - Jan2015 | Jun1996 - Jan2015 | Jun1996 - Jan2015 |

| Cagr | 8.61 | 9.82 | 10.22 | 9.19 |

| Sharpe | 0.65 | 0.74 | 0.77 | 0.68 |

| DVR | 0.63 | 0.69 | 0.74 | 0.64 |

| Volatility | 14.38 | 14.23 | 14.1 | 14.8 |

| MaxDD | -25.49 | -24.85 | -27.84 | -30.29 |

| AvgDD | -2.83 | -2.93 | -2.77 | -2.96 |

| VaR | -1.5 | -1.48 | -1.47 | -1.59 |

| CVaR | -2.16 | -2.14 | -2.14 | -2.26 |

| Exposure | 93.24 | 94.13 | 93.7 | 94.13 |

Somehow, strategy with 2 month offset is most volatile and has largest draw-down.

(this report was produced on: 2015-01-03)