Stock Bond Model from Don't Fear the Bear

13 Dec 2014To install Systematic Investor Toolbox (SIT) please visit About page.

Another interesing post from Don’t Fear the Bear : A stock bond model based on the average investor allocation to equities that is based on the The Single Greatest Predictor of Future Stock Market Returns

The main indicator:

Investor Allocation to Stocks (Average) = Market Value of All Stocks / (Market Value of All Stocks + Total Liabilities of All Real Economic Borrowers)

is constructed using FRED data in the here

It is based on the following data:

- (a) Nonfinancial corporate business; corporate equities; liability, Level, Millions of Dollars, Not Seasonally Adjusted (NCBEILQ027S)

- (b) Nonfinancial Corporate Business; Credit Market Instruments; Liability, Billions of Dollars, Seasonally Adjusted (BCNSDODNS)

- (c) Households and Nonprofit Organizations; Credit Market Instruments; Liability, Level, Billions of Dollars, Seasonally Adjusted (CMDEBT)

- (d) Federal Government; Credit Market Instruments; Liability, Level, Billions of Dollars, Seasonally Adjusted (FGSDODNS)

- (e) State and Local Governments, Excluding Employee Retirement Funds; Credit Market Instruments; Liability, Level, Billions of Dollars, Seasonally Adjusted (SLGSDODNS)

- (f) Financial business; corporate equities; liability, Level, Millions of Dollars, Not Seasonally Adjusted (FBCELLQ027S)

- (g) Rest of the World; Credit Market Instruments; Liability, Level, Billions of Dollars, Seasonally Adjusted (DODFFSWCMI)

Please not the that (a) and (f) are Millions, rest in Billions; hence there is division by 1000 in the formula below:

Investor Allocation to Stocks (Average) = ((a+f)/1000)/(((a+f)/1000)+b+c+d+e+g)

Load historical data from FRED:

#*****************************************************************

# Load historical data

#*****************************************************************

library(SIT)

load.packages('quantmod')

tickers = spl('A=NCBEILQ027S,B=BCNSDODNS,C=CMDEBT,D=FGSDODNS,E=SLGSDODNS,F=FBCELLQ027S,G=DODFFSWCMI')

metric.data <- new.env()

getSymbols.extra(tickers, src = 'FRED', from = '1900-01-01', env = metric.data, auto.assign = T, getSymbols.fn=quantmod:::getSymbols)Next let’s compute the Stock Allocation:

metric.data$StockAllocation = with(metric.data, ((A+F)/1000)/(((A+F)/1000)+B+C+D+E+G))

metric.data$AverageRatio = SMA(ifna.prev(metric.data$StockAllocation),4)

metric.data$RelativeAverageRatio = 1 - (metric.data$AverageRatio - 0.25) / 0.20

metric.data$RelativeAverageRatio = iif(metric.data$RelativeAverageRatio > 1, 1, metric.data$RelativeAverageRatio)

metric.data$RelativeAverageRatio = iif(metric.data$RelativeAverageRatio < 0, 0, metric.data$RelativeAverageRatio)

colnames(metric.data$RelativeAverageRatio) = 'RelativeAverageRatio'

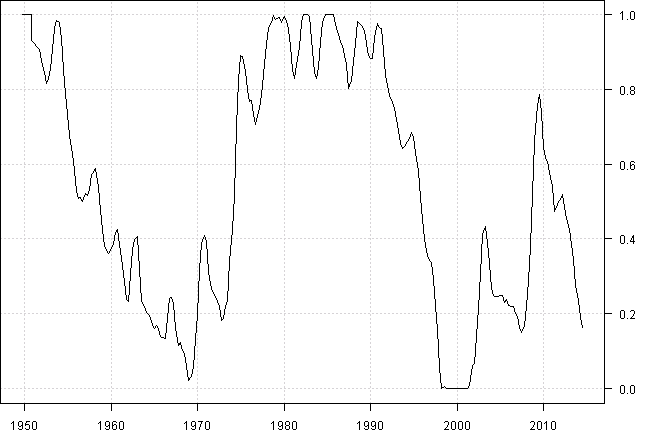

plota(metric.data$RelativeAverageRatio, type='l')

print(last(metric.data$RelativeAverageRatio, 20))| RelativeAverageRatio | |

|---|---|

| 2009-10-01 | 0.7386075 |

| 2010-01-01 | 0.6448204 |

| 2010-04-01 | 0.6192706 |

| 2010-07-01 | 0.6073752 |

| 2010-10-01 | 0.5777071 |

| 2011-01-01 | 0.5408631 |

| 2011-04-01 | 0.4747850 |

| 2011-07-01 | 0.4852374 |

| 2011-10-01 | 0.4993816 |

| 2012-01-01 | 0.5045022 |

| 2012-04-01 | 0.5189942 |

| 2012-07-01 | 0.4680151 |

| 2012-10-01 | 0.4474356 |

| 2013-01-01 | 0.4258632 |

| 2013-04-01 | 0.3850559 |

| 2013-07-01 | 0.3436522 |

| 2013-10-01 | 0.2763624 |

| 2014-01-01 | 0.2348901 |

| 2014-04-01 | 0.1889742 |

| 2014-07-01 | 0.1637294 |

Now let’s test the strategy with Vanguard funds:

#*****************************************************************

# Test Strategy

#*****************************************************************

tickers='STOCK=VFINX,BOND=VUSTX'

data <- new.env()

getSymbols.extra(tickers, src = 'yahoo', from = '1970-01-01', env = data, auto.assign = T)

for(i in ls(data)) data[[i]] = adjustOHLC(data[[i]], use.Adjusted=T)

print(bt.start.dates(data))| Start | |

|---|---|

| STOCK | 1987-03-27 |

| BOND | 1989-12-14 |

data$StockAllocation = make.stock.xts(metric.data$RelativeAverageRatio)

bt.prep(data, align='keep.all')

prices = data$prices

prices$StockAllocation = ifna.prev(prices$StockAllocation)

models = list()

#*****************************************************************

# Code Strategies

#*****************************************************************

data$weight[] = NA

data$weight$BOND = 1

models$BOND = bt.run.share(data, clean.signal=F, silent=T)

data$weight[] = NA

data$weight$STOCK = 1

models$STOCK = bt.run.share(data, clean.signal=F, silent=T)

data$weight[] = NA

data$weight$STOCK = prices$StockAllocation

data$weight$BOND = 1 - prices$StockAllocation

models$strategy = bt.run.share(data, clean.signal=F, silent=T)

models = bt.trim(models, dates = '1990::')

#*****************************************************************

# Create Report

#*****************************************************************

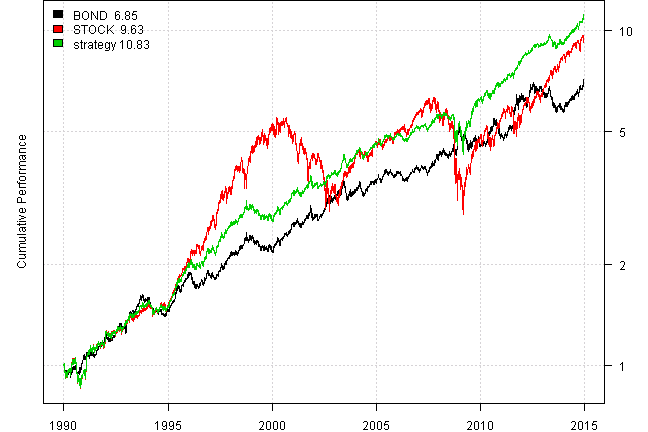

plotbt(models, plotX = T, log = 'y', LeftMargin = 3, main = NULL)

mtext('Cumulative Performance', side = 2, line = 1)

print(plotbt.strategy.sidebyside(models, make.plot=F, return.table=T))| BOND | STOCK | strategy | |

|---|---|---|---|

| Period | Jan1990 - Dec2014 | Jan1990 - Dec2014 | Jan1990 - Dec2014 |

| Cagr | 8 | 9.49 | 10 |

| Sharpe | 0.78 | 0.59 | 1.02 |

| DVR | 0.74 | 0.48 | 0.94 |

| Volatility | 10.45 | 18.06 | 9.71 |

| MaxDD | -18.78 | -55.25 | -25.07 |

| AvgDD | -2.16 | -2.22 | -1.38 |

| VaR | -1.05 | -1.73 | -0.9 |

| CVaR | -1.45 | -2.67 | -1.41 |

| Exposure | 100 | 100 | 100 |

There is more to investigate. The fun part is that i was able to replicate this strategy in about 2 hours.

(this report was produced on: 2014-12-25)