Sortino vs Omega ratios

02 Apr 2015To install Systematic Investor Toolbox (SIT) please visit About page.

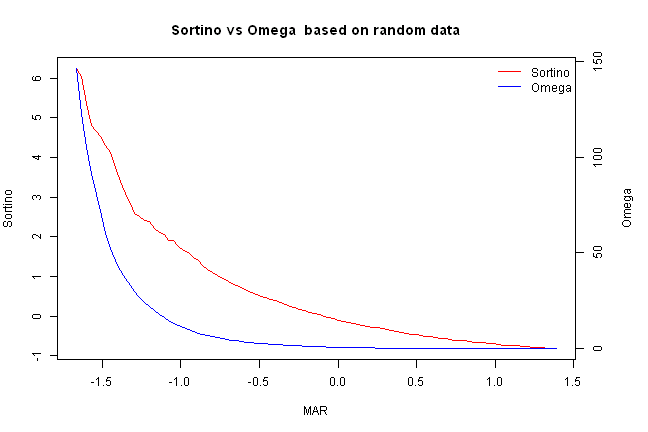

Following is quick visual comparison of Omega ratio vs Sortino ratio

library(SIT)

load.packages('quantmod')

#*****************************************************************

# Helper functions

#*****************************************************************

sortino.ratio = function(R,MAR) {

r = R[R < MAR]

(mean(R) - MAR) / sqrt(sum((MAR - r)^2) / length(r) )

}

omega.ratio = function(R,MAR) {

#sum(pmax(R - MAR, 0)) / sum(pmax(MAR - R, 0))

r = R - MAR

- sum(r[r > 0]) / sum(r[r < 0])

}

#*****************************************************************

# check: Omega has a value of 1 at the mean of the distribution

#*****************************************************************

R = rnorm(100)

MAR = mean(R)

print(list(Sortino = sortino.ratio(R, MAR), Omega = omega.ratio(R,MAR)))$Sortino [1] 0 $Omega [1] 1

#*****************************************************************

# Plot Sortino vs Omega

# based on [R graph with two y-axes](http://robjhyndman.com/hyndsight/r-graph-with-two-y-axes/)

#*****************************************************************

plot.sortino.omega = function(R, main='') {

x = quantile(R, c(0.05, 0.95))

x = seq(x[1],x[2], length.out=100)

par(mar=c(5,4,4,5))

plot(x, sapply(x, function(y) sortino.ratio(R,y)), xlab='MAR', ylab='Sortino',

main=paste('Sortino vs Omega', main), type='l', col='red')

par(new=TRUE)

plot(x, sapply(x, function(y) omega.ratio(R,y)), xaxt="n",yaxt="n",xlab="", ylab='', type='l', col='blue')

axis(4)

mtext('Omega',side=4,line=3)

legend("topright",col=c('red','blue'),lty=1,legend=c('Sortino','Omega'), bty='n')

}

plot.sortino.omega(R, ' based on random data')

#*****************************************************************

# Load historical data

#*****************************************************************

data = env()

getSymbols('SPY', src = 'yahoo', from = '1970-01-01', env = data, auto.assign = T)

price = Ad(data$SPY)

ret = diff(log(price))

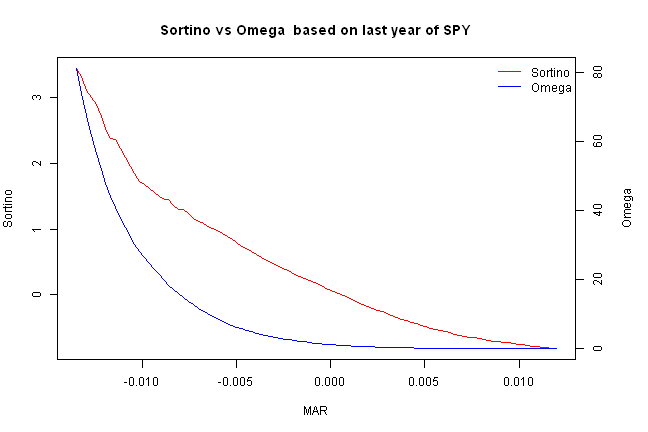

plot.sortino.omega(last(ret, 252), ' based on last year of SPY')

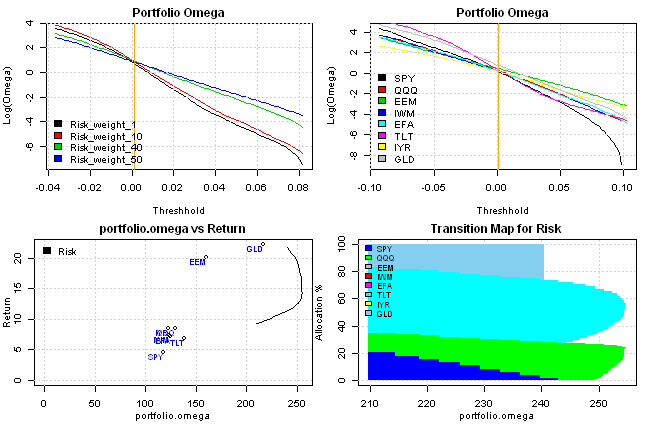

Re-run Maximizing Omega Ratio

Please set threshold used in Omega calculations (i.e. MAR) to a small number. Otherwise, optimizer will be forced to find corner solutions and result in not stable weights.

#--------------------------------------------------------------------------

# Create Efficient Frontier

#--------------------------------------------------------------------------

ia = aa.test.create.ia()

n = ia$n

# 0 <= x.i <= 0.8

constraints = new.constraints(n, lb = 0, ub = 0.8)

# SUM x.i = 1

constraints = add.constraints(rep(1, n), 1, type = '=', constraints)

# Omega - http://en.wikipedia.org/wiki/Omega_ratio

# do not set threshold too high

ia$parameters.omega = 1/100

# convert annual to monthly

ia$parameters.omega = ia$parameters.omega / 12

max.omega.portfolio(ia, constraints) [1] 0.000000e+00 7.255498e-02 1.688399e-01 1.097557e-16 0.000000e+00 [6] 2.661959e-01 0.000000e+00 4.924093e-01

# create efficient frontier(s)

ef.risk = portopt(ia, constraints, 50, 'Risk')

#plot.ef(ia, list(ef.risk), portfolio.risk, T, T)

# Plot Omega Efficient Frontiers and Transition Maps

layout( matrix(1:4, nrow = 2, byrow=T) )

# weights

rownames(ef.risk$weight) = paste('Risk','weight',1:50,sep='_')

plot.omega(ef.risk$weight[c(1,10,40,50), ], ia)

# assets

temp = diag(n)

rownames(temp) = ia$symbols

plot.omega(temp, ia)

# portfolio

plot.ef(ia, list(ef.risk), portfolio.omega, T, T)

#--------------------------------------------------------------------------

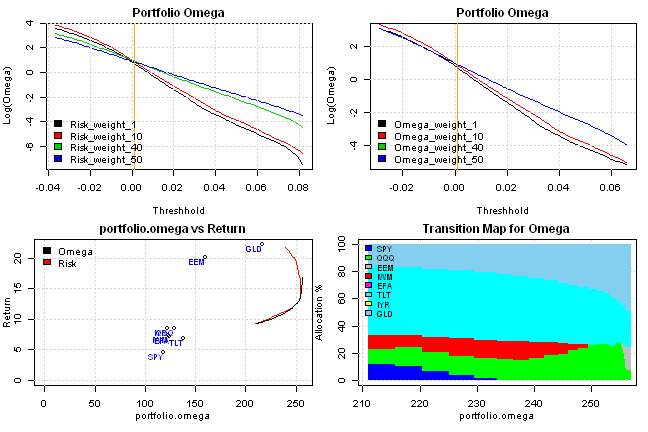

# Create Efficient Frontier in Omega Ratio framework

#--------------------------------------------------------------------------

# Create maximum Omega Efficient Frontier

ef.omega = portopt.omega(ia, constraints, 50)i = 1 i = 2 i = 3 i = 4 i = 5 i = 6 i = 7 i = 8 i = 9 i = 10 i = 11 i = 12 i = 13 i = 14 i = 15 i = 16 i = 17 i = 18 i = 19 i = 20 i = 21 i = 22 i = 23 i = 24 i = 25 i = 26 i = 27 i = 28 i = 29 i = 30 i = 31 i = 32 i = 33 i = 34 i = 35 i = 36 i = 37 i = 38 i = 39 i = 40 i = 41 i = 42 i = 43 i = 44 i = 45 i = 46 i = 47 i = 48 i = 49 i = 50

# Plot Omega Efficient Frontiers and Transition Maps

layout( matrix(1:4, nrow = 2, byrow=T) )

# weights

plot.omega(ef.risk$weight[c(1,10,40,50), ], ia)

#plot.omega(ef.omega$weight[c(1,10,40,50), ], ia)

# weights

rownames(ef.omega$weight) = paste('Omega','weight',1:50,sep='_')

plot.omega(ef.omega$weight[c(1,10,40,50), ], ia)

# portfolio

plot.ef(ia, list(ef.omega, ef.risk), portfolio.omega, T, T)

#--------------------------------------------------------------------------

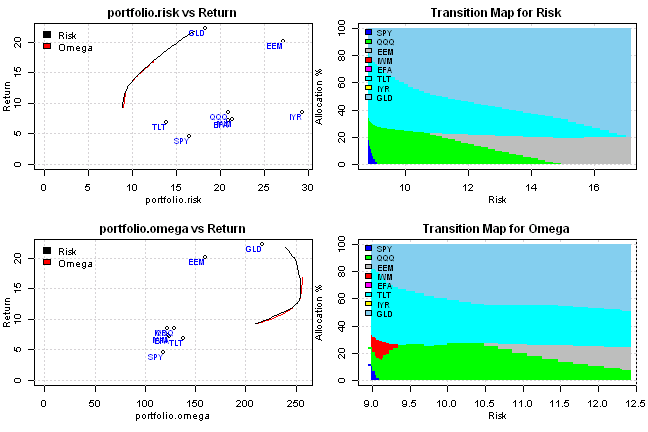

# Compare Risk and Omega frontiers

#--------------------------------------------------------------------------

# Plot multiple Efficient Frontiers and Transition Maps

layout( matrix(1:4, nrow = 2) )

plot.ef(ia, list(ef.risk,ef.omega), portfolio.risk, F)

plot.ef(ia, list(ef.risk,ef.omega), portfolio.omega, F)

plot.transition.map(ef.risk)

plot.transition.map(ef.omega)

I will use methods presented in Optimizing Omega by H. Mausser, D. Saunders, L. Seco (2006) paper to construct optimal portfolios that maximize Omega Ratio.

#' @export

target.omega.portfolio <- function

(

target.omega,

type = 'mixed'

)

{

target.omega = target.omega

function

(

ia, # input assumptions

constraints # constraints

)

{

ia$parameters.omega = target.omega

max.omega.portfolio(ia, constraints, type)

}

}

#*****************************************************************

# Load historical data

#*****************************************************************

library(SIT)

load.packages('quantmod')

# load saved Proxies Raw Data, data.proxy.raw, to extend DBC and SHY

# please see http://systematicinvestor.github.io/Data-Proxy/ for more details

load('data/data.proxy.raw.Rdata')

tickers = '

LQD + VWESX

DBC + CRB

VTI +VTSMX # (or SPY)

ICF + VGSIX # (or IYR)

CASH = SHY + TB3Y

'

data <- new.env()

getSymbols.extra(tickers, src = 'yahoo', from = '1970-01-01', env = data, raw.data = data.proxy.raw, set.symbolnames = T, auto.assign = T)

for(i in data$symbolnames) data[[i]] = adjustOHLC(data[[i]], use.Adjusted=T)

#print(bt.start.dates(data))

bt.prep(data, align='remove.na', fill.gaps = T)

#*****************************************************************

# Code Strategies

#******************************************************************

obj = portfolio.allocation.helper(data$prices,

periodicity = 'months', lookback.len = 60,

min.risk.fns = list(

EW=equal.weight.portfolio,

RP=risk.parity.portfolio(),

MD=max.div.portfolio,

MV=min.var.portfolio,

MVE=min.var.excel.portfolio,

MO=target.omega.portfolio(0/100, 'lp'),

MC=min.corr.portfolio,

MCE=min.corr.excel.portfolio,

MC2=min.corr2.portfolio,

MS=max.sharpe.portfolio()

),

silent=T

)

commission = list(cps = 0.01, fixed = 10.0, percentage = 0.0)

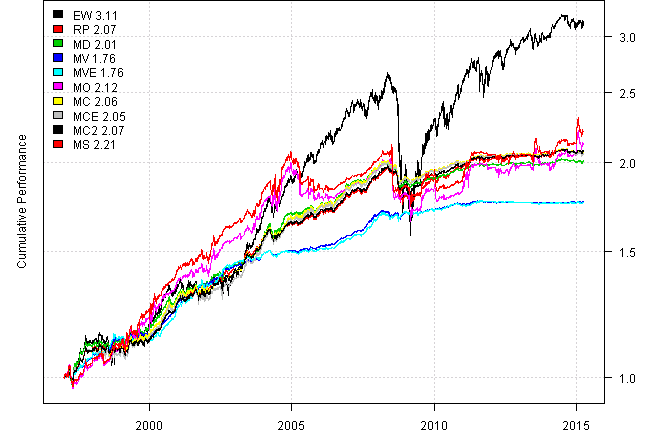

models = create.strategies(obj, data, dates='1997::', commission=commission, silent=T)$models

#*****************************************************************

# Create Report

#*****************************************************************

#strategy.performance.snapshoot(models, T)

plotbt(models, plotX = T, log = 'y', LeftMargin = 3, main = NULL)

mtext('Cumulative Performance', side = 2, line = 1)

print(plotbt.strategy.sidebyside(models, make.plot=F, return.table=T, perfromance.fn=engineering.returns.kpi))| EW | RP | MD | MV | MVE | MO | MC | MCE | MC2 | MS | |

|---|---|---|---|---|---|---|---|---|---|---|

| Period | Jan1997 - Apr2015 | Jan1997 - Apr2015 | Jan1997 - Apr2015 | Jan1997 - Apr2015 | Jan1997 - Apr2015 | Jan1997 - Apr2015 | Jan1997 - Apr2015 | Jan1997 - Apr2015 | Jan1997 - Apr2015 | Jan1997 - Apr2015 |

| Cagr | 6.41 | 4.06 | 3.88 | 3.15 | 3.13 | 4.2 | 4.04 | 4.02 | 4.06 | 4.43 |

| Sharpe | 0.65 | 1.26 | 1.19 | 1.73 | 1.47 | 0.72 | 1.25 | 1.22 | 1.32 | 0.76 |

| DVR | 0.6 | 1.21 | 1.1 | 1.61 | 1.36 | 0.61 | 1.18 | 1.16 | 1.26 | 0.63 |

| R2 | 0.93 | 0.96 | 0.92 | 0.93 | 0.93 | 0.84 | 0.94 | 0.95 | 0.96 | 0.84 |

| Volatility | 10.51 | 3.2 | 3.26 | 1.8 | 2.12 | 5.95 | 3.21 | 3.27 | 3.07 | 5.99 |

| MaxDD | -40.68 | -12.11 | -8.74 | -2.88 | -2.97 | -19.4 | -7.97 | -7.57 | -8.67 | -17.97 |

| Exposure | 99.98 | 99.98 | 99.98 | 99.98 | 99.98 | 99.98 | 99.98 | 99.98 | 99.98 | 99.98 |

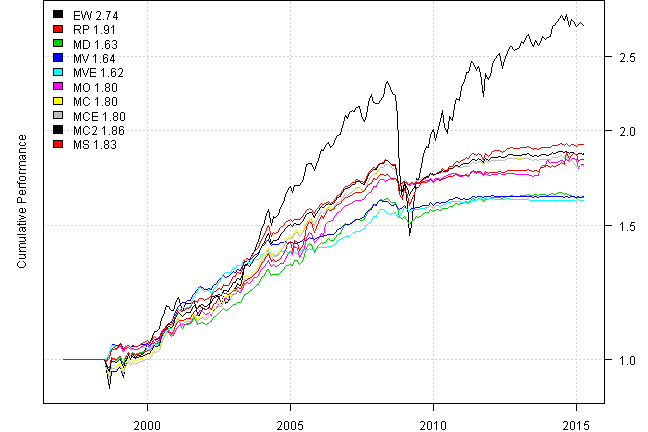

Now let’s do monthly

data = bt.change.periodicity(data, periodicity = 'months')

#*****************************************************************

# Code Strategies

#******************************************************************

obj = portfolio.allocation.helper(data$prices,

periodicity = 'months', lookback.len = 24,

min.risk.fns = list(

EW=equal.weight.portfolio,

RP=risk.parity.portfolio(),

MD=max.div.portfolio,

MV=min.var.portfolio,

MVE=min.var.excel.portfolio,

MO=target.omega.portfolio(0/100, 'lp'),

MC=min.corr.portfolio,

MCE=min.corr.excel.portfolio,

MC2=min.corr2.portfolio,

MS=max.sharpe.portfolio()

),

silent=T

)

models = create.strategies(obj, data, dates='1997::', commission=commission, silent=T)$models

#*****************************************************************

# Create Report

#*****************************************************************

#strategy.performance.snapshoot(models, T)

plotbt(models, plotX = T, log = 'y', LeftMargin = 3, main = NULL)

mtext('Cumulative Performance', side = 2, line = 1)

print(plotbt.strategy.sidebyside(models, make.plot=F, return.table=T, perfromance.fn=engineering.returns.kpi))| EW | RP | MD | MV | MVE | MO | MC | MCE | MC2 | MS | |

|---|---|---|---|---|---|---|---|---|---|---|

| Period | Jan1997 - Apr2015 | Jan1997 - Apr2015 | Jan1997 - Apr2015 | Jan1997 - Apr2015 | Jan1997 - Apr2015 | Jan1997 - Apr2015 | Jan1997 - Apr2015 | Jan1997 - Apr2015 | Jan1997 - Apr2015 | Jan1997 - Apr2015 |

| Cagr | 5.71 | 3.63 | 2.73 | 2.74 | 2.68 | 3.29 | 3.28 | 3.28 | 3.47 | 3.38 |

| Sharpe | 0.66 | 1.05 | 0.96 | 1.47 | 1.25 | 1.13 | 1.06 | 1.03 | 1.09 | 1.1 |

| DVR | 0.61 | 0.99 | 0.9 | 1.34 | 1.16 | 1.07 | 0.98 | 0.96 | 1.02 | 1.03 |

| R2 | 0.93 | 0.94 | 0.94 | 0.91 | 0.93 | 0.94 | 0.93 | 0.93 | 0.93 | 0.94 |

| Volatility | 8.97 | 3.44 | 2.83 | 1.84 | 2.12 | 2.88 | 3.08 | 3.15 | 3.16 | 3.06 |

| MaxDD | -37.17 | -12.8 | -7.54 | -3.17 | -2.59 | -3.22 | -6.56 | -6.54 | -9.92 | -3.38 |

| Exposure | 91.82 | 91.82 | 91.82 | 91.82 | 91.82 | 91.82 | 91.82 | 91.82 | 91.82 | 91.82 |

(this report was produced on: 2015-04-10)