Simulating correlated random walks with Copulas

16 Jan 2015To install Systematic Investor Toolbox (SIT) please visit About page.

Another great article from mktstk: Simulating correlated random walks with Copulas

We can replicate this example using R

#*****************************************************************

# Load historical data

#******************************************************************

library(SIT)

load.packages('quantmod')

filename = 'intraday.Rdata'

if(!file.exists(filename)) {

data <- new.env()

data$YHOO = getSymbol.intraday.google('YHOO', 'NASDAQ', 60, '15d')

data$FB = getSymbol.intraday.google('FB', 'NASDAQ', 60, '15d')

bt.prep(data, align='remove.na')

save(data, file=filename)

}

load(file=filename)

#*****************************************************************

# Generate simulations

#******************************************************************

prices = data$prices

n = ncol(prices)

rets = diff(log(prices))

rets = coredata(na.omit(rets))

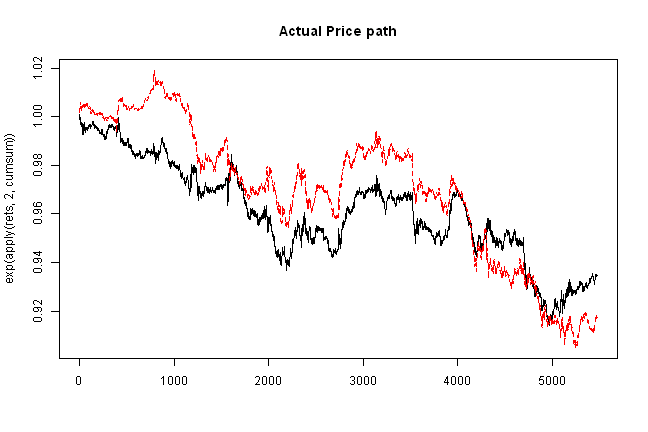

# Plot prices

matplot(exp(apply(rets,2,cumsum)), type='l', main='Actual Price path')

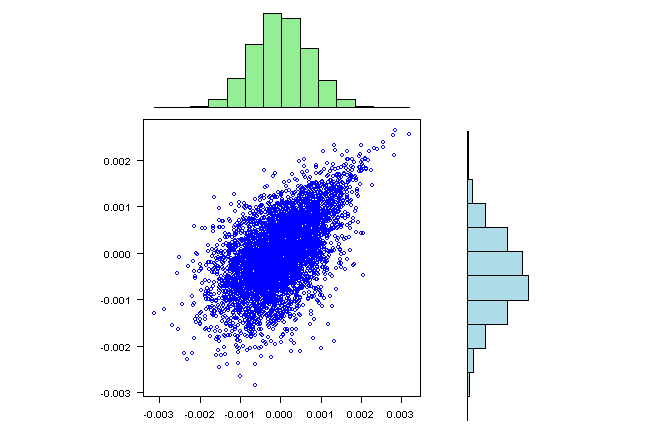

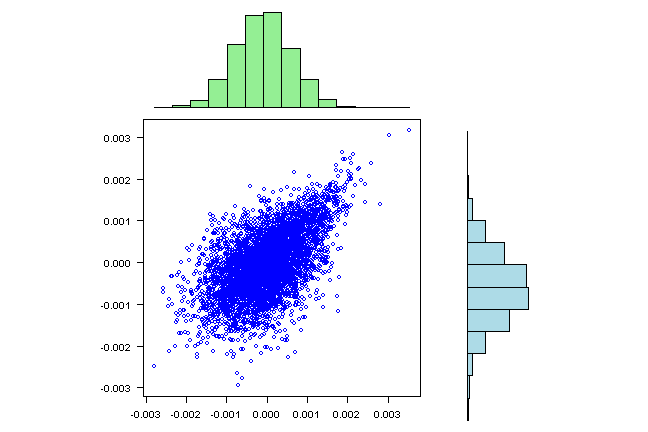

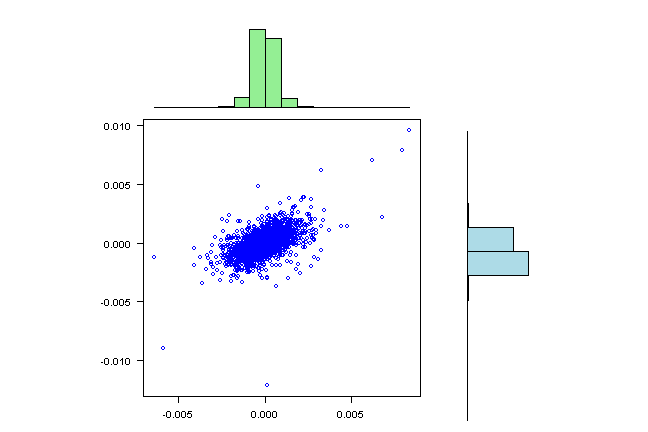

# helper function to visualize distribution

visualize.rets = function(fit.sim) {

labs = colnames(rets)

xhist = hist(fit.sim[,1], plot=FALSE)

yhist = hist(fit.sim[,2], plot=FALSE)

top =max(c(xhist$counts, yhist$counts))

layout(matrix(c(2,0,1,3),2,2,byrow=TRUE), c(3,1), c(1,3), TRUE)

par(mar=c(3,3,1,1))

plot(fit.sim[,1], fit.sim[,2], xlab=labs[1], ylab=labs[2], col='blue', las=1)

par(mar=c(0,3,1,1))

barplot(xhist$counts, axes=FALSE, ylim=c(0, top), space=0,col="light green")

barplot(yhist$counts, axes=FALSE, xlim=c(0, top), space=0, horiz=TRUE,col="light blue")

}

# Helper function to check Copula fit

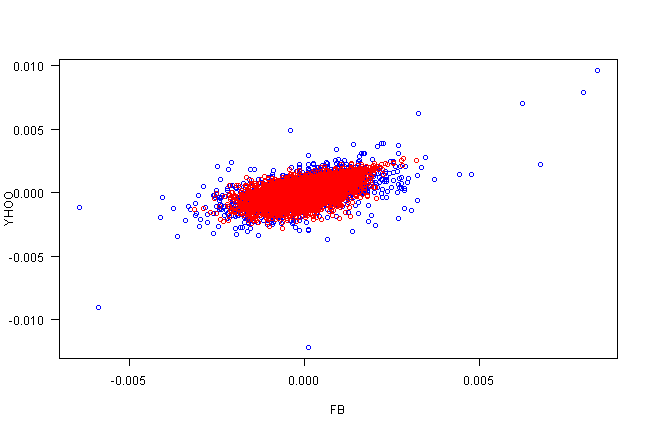

copula.check = function(fit.sim) {

# plot simulated vs actual

labs = colnames(rets)

layout(1)

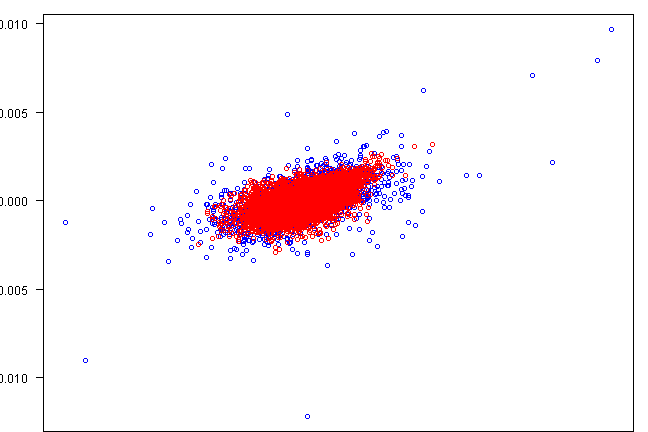

plot(rets[,1], rets[,2], xlab=labs[1], ylab=labs[2], col='blue', las=1)

points(fit.sim[,1], fit.sim[,2], col='red')

# compare stats for simulated vs actual

temp = matrix(0,nr=5,nc=2)

colnames(temp) = spl('Actual,Simulated')

rownames(temp) = c('Correlation', paste('Mean', labs), paste('StDev', labs))

temp[1,] = c(cor(rets)[1,2], cor(fit.sim)[1,2])

temp[2:3,] = 252 * cbind(apply(rets, 2, mean), apply(fit.sim, 2, mean))

temp[4:5,] = sqrt(252) * cbind(apply(rets, 2, sd), apply(fit.sim, 2, sd))

print(round(100*temp,2))

# check if returns come from same distributions

for (i in 1:2) {

print(labs[i])

print(ks.test(rets[,i], fit.sim[i]))

}

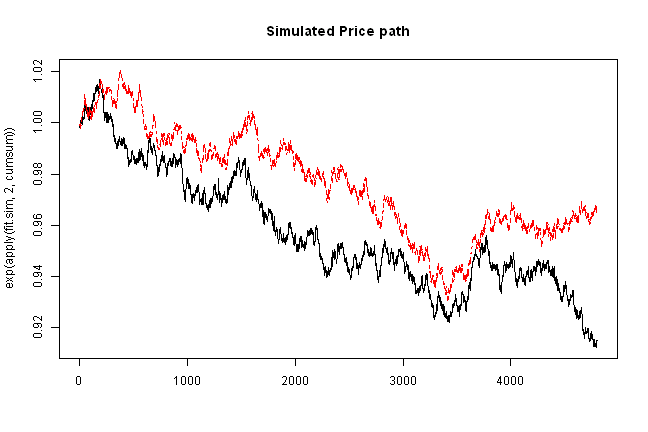

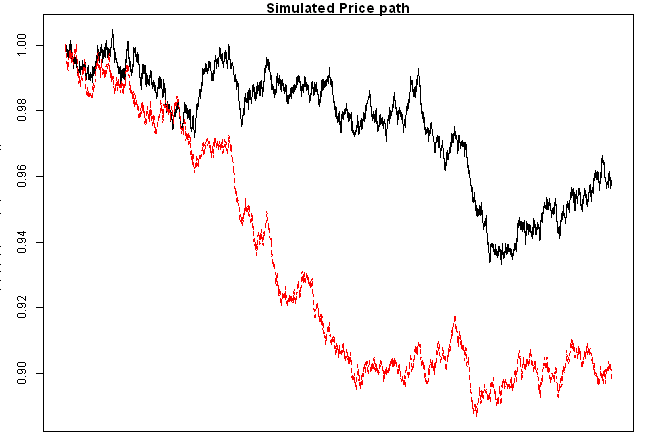

# plot simulated price path

matplot(exp(apply(fit.sim,2,cumsum)), type='l', main='Simulated Price path')

}

# fit Copula

load.packages('copula')package ‘gsl’ successfully unpacked and MD5 sums checked package ‘ADGofTest’ successfully unpacked and MD5 sums checked package ‘stabledist’ successfully unpacked and MD5 sums checked package ‘mvtnorm’ successfully unpacked and MD5 sums checked package ‘pspline’ successfully unpacked and MD5 sums checked package ‘copula’ successfully unpacked and MD5 sums checked

The downloaded binary packages are in C:\Temp\RtmpCw8dcM\downloaded_packages

gumbel.cop = gumbelCopula(dim=n)

uniform.data = pobs(rets)

gumbel = fitCopula(gumbel.cop, uniform.data, method="ml")

# create custom distribution by combining fitted margins with fitted copula

margins=c("norm","norm")

paramMargins=apply(rets,2,function(x) list(mean=mean(x), sd=sd(x)))

fit = mvdc(copula = gumbelCopula(gumbel@estimate, dim=n),

margins=margins,paramMargins=paramMargins)

# simulate from fitted distn

fit.sim = rMvdc(4800, fit)

copula.check(fit.sim)

| Actual | Simulated | |

|---|---|---|

| Correlation | 57.13 | 57.38 |

| Mean FB | -0.31 | -0.47 |

| Mean YHOO | -0.40 | -0.17 |

| StDev FB | 1.24 | 1.25 |

| StDev YHOO | 1.23 | 1.23 |

FB

Two-sample Kolmogorov-Smirnov test data: rets[, i] and fit.sim[i] D = 0.9404, p-value = 0.3395 alternative hypothesis: two-sided

YHOO

Two-sample Kolmogorov-Smirnov test data: rets[, i] and fit.sim[i] D = 0.8792, p-value = 0.4222 alternative hypothesis: two-sided

visualize.rets(fit.sim)

# alternatively we can do it by hand, please note to go from uniform data

# to original data, we can use quantile function

# i.e [simulation by inverse cdf](https://xianblog.wordpress.com/2015/01/14/simulation-by-inverse-cdf/)

# qnorm(runif(10^8)) and rnorm(10^8) are equivalent

uniform.sim = rCopula(4800, gumbelCopula(gumbel@estimate, dim=n))

fit.sim2 = cbind(

qnorm(uniform.sim[,1],mean(rets[,1]),sd(rets[,1])),

qnorm(uniform.sim[,2],mean(rets[,2]),sd(rets[,2]))

)

copula.check(fit.sim2)

| Actual | Simulated | |

|---|---|---|

| Correlation | 57.13 | 57.14 |

| Mean FB | -0.31 | -0.22 |

| Mean YHOO | -0.40 | -0.56 |

| StDev FB | 1.24 | 1.24 |

| StDev YHOO | 1.23 | 1.21 |

FB

Two-sample Kolmogorov-Smirnov test data: rets[, i] and fit.sim[i] D = 0.7791, p-value = 0.5787 alternative hypothesis: two-sided

YHOO

Two-sample Kolmogorov-Smirnov test data: rets[, i] and fit.sim[i] D = 0.795, p-value = 0.5525 alternative hypothesis: two-sided

visualize.rets(fit.sim2)

visualize.rets(rets)

Please note that Standard Deviation is huge relative to the Mean, which is close to zero; hence, we are very likely to get positive and negative outcomes in some cases.

For additional references on the topic, I found following references very useful:

- Generating values from copula using copula package in R

- Simulating returns using copula and SPD distribution

- Info from Eric Zivot’s site

- R Code

- Principal Component Analysis (PCA) vs Ordinary Least Squares (OLS): A Visual Explanation

- Stochastic Simulation With Copulas in R

- Even Simpler Multivariate Correlated Simulations

-

Third, and Hopefully Final, Post on Correlated Random Normal Generation (Cholesky Edition)

- Ambhas

- simulation by inverse cdf > system.time(qnorm(runif(10^8))) > system.time(rnorm(10^8))

(this report was produced on: 2015-01-17)