Robust Asset Allocation

24 Feb 2015To install Systematic Investor Toolbox (SIT) please visit About page.

The Scott’s Investments posted a spread sheet with Robust Asset Allocation (RAA) strategy based on the Alpha Architect’s - Our Robust Asset Allocation (RAA) Solution

Below I will try to adapt a code from the posts:

#*****************************************************************

# Load historical data

#*****************************************************************

library(SIT)

load.packages('quantmod')

# load saved Proxies Raw Data, data.proxy.raw

# please see http://systematicinvestor.github.io/Data-Proxy/ for more details

load('data/data.proxy.raw.Rdata')

tickers = '

SP500 = SPY

EAFE = EFA + VDMIX + VGTSX

REIT = VNQ + VGSIX # Vanguard REIT

COM = DBC + CRB # PowerShares DB Commodity Index Tracking Fund

US.BOND = IEF + VFITX

#US.BOND = BND + VBMFX # Vanguard Total Bond Market

US.VAL = PRF # PowerShares FTSE RAFI US 1000

US.MOM = PDP # PowerShares DWA Momentum Portfolio

INT.VAL = GVAL # Cambria Global Value

INT.MOM = PIZ # PowerShares DWA Developed Markets Momentum Portfolio

CASH = BIL + TB3M # Money Market or SHY/BIL

'

data <- new.env()

getSymbols.extra(tickers, src = 'yahoo', from = '1970-01-01', env = data, raw.data = data.proxy.raw, set.symbolnames = T, auto.assign = T)

# convert to monthly, 1-month-year format, to match Fama/French factors

for(i in data$symbolnames) {

temp = to.monthly(data[[i]], indexAt='endof')

index(temp) = as.Date(format(index(temp), '%Y-%m-1'),'%Y-%m-%d')

data[[i]] = temp

}

#*****************************************************************

# Get Fama/French factors

#******************************************************************

download = T

factors = get.fama.french.data('10_Portfolios_Prior_12_2', 'months',download = download, clean = F)

temp = factors[["Average Value Weighted Returns -- Monthly"]]$High

temp = cumprod(1+temp/100)

data$US.MOM = extend.data(data$US.MOM, make.stock.xts(temp), scale=T)

factors = get.fama.french.data('Portfolios_Formed_on_BE-ME', 'months',download = download, clean = F)

temp = factors[["Value Weighted Returns -- Monthly"]][,'Hi 10']

temp = cumprod(1+temp/100)

data$US.VAL = extend.data(data$US.VAL, make.stock.xts(temp), scale=T)

factors = get.fama.french.data('Global_ex_US_25_Portfolios_ME_Prior_12_2', 'months',download = download, clean = F)

temp = factors[["Average Value Weighted Returns -- Monthly"]]$Big.High

temp[] = rowMeans(factors[["Average Value Weighted Returns -- Monthly"]][,spl('Big.3,Big.4,Big.High')])

temp = cumprod(1+temp/100)

data$INT.MOM = extend.data(data$INT.MOM, make.stock.xts(temp), scale=T)

factors = get.fama.french.data('Global_ex_US_25_Portfolios_ME_BE-ME', 'months',download = download, clean = F)

temp = factors[["Average Value Weighted Returns -- Monthly"]]$Big.High

temp[] = rowMeans(factors[["Average Value Weighted Returns -- Monthly"]][,spl('Big.3,Big.4,Big.High')])

temp = cumprod(1+temp/100)

data$INT.VAL = extend.data(data$INT.VAL, make.stock.xts(temp), scale=T)

data$REIT = extend.data(data$REIT, data.proxy.raw$NAREIT, scale=T)

for(i in data$symbolnames) data[[i]] = adjustOHLC(data[[i]], use.Adjusted=T)

#print(bt.start.dates(data))

bt.prep(data, align='remove.na')

# Check data

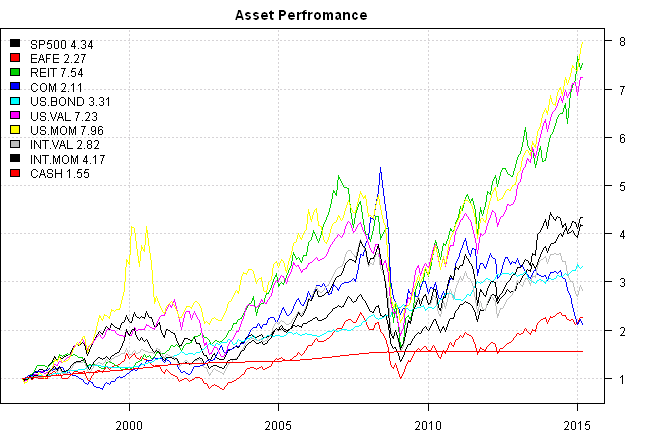

plota.matplot(scale.one(data$prices),main='Asset Perfromance')

#*****************************************************************

# Setup

#*****************************************************************

data$universe = data$prices > 0

# do not allocate to CASH

data$universe$CASH = NA

prices = data$prices * data$universe

n = ncol(prices)

nperiods = nrow(prices)

period.ends = endpoints(prices, 'months')

period.ends = period.ends[period.ends > 0]

models = list()

#*****************************************************************

# Benchmarks

#*****************************************************************

data$weight[] = NA

data$weight$SP500 = 1

models$SP500 = bt.run.share(data, clean.signal=T, trade.summary=T, silent=T)

data$weight[] = NA

data$weight$SP500[period.ends,] = 0.5

data$weight$US.BOND[period.ends,] = 0.5

models$S50.50 = bt.run.share(data, clean.signal=T, trade.summary=T, silent=T)

data$weight[] = NA

data$weight$SP500[period.ends,] = 0.6

data$weight$US.BOND[period.ends,] = 0.4

models$S60.40 = bt.run.share(data, clean.signal=T, trade.summary=T, silent=T)

#*****************************************************************

# IVY

# The [Quantitative Approach To Tactical Asset Allocation Strategy(QATAA) by Mebane T. Faber](http://mebfaber.com/timing-model/)

# [SSRN paper](http://papers.ssrn.com/sol3/papers.cfm?abstract_id=962461)

#*****************************************************************

sma = bt.apply.matrix(prices, SMA, 10)

# IVY5

prices1 = prices * NA

for(i in spl('SP500,EAFE,REIT,COM,US.BOND'))

prices1[,i] = prices[,i]

nasset = sum(count(last(prices1)))

data$weight[] = NA

data$weight[period.ends,] = ntop(prices1[period.ends,], nasset)

models$IVY5 = bt.run.share(data, clean.signal=F, trade.summary=T, silent=T)

# IVY5_MA

weight = NA * data$weight

weight = iif(prices1 > sma, 1/nasset, 0)

weight$CASH = 1 - rowSums(weight)

data$weight[] = NA

data$weight[period.ends,] = weight[period.ends,]

models$IVY5_MA = bt.run.share(data, clean.signal=F, trade.summary=T, silent=T)

# IVY

nasset = sum(count(last(prices)))

data$weight[] = NA

data$weight[period.ends,] = ntop(prices[period.ends,], n)

models$IVY = bt.run.share(data, clean.signal=F, trade.summary=T, silent=T)

# IVY_MA

weight = NA * data$weight

weight = iif(prices > sma, 1/nasset, 0)

weight$CASH = 1 - rowSums(weight)

data$weight[] = NA

data$weight[period.ends,] = weight[period.ends,]

models$IVY_MA = bt.run.share(data, clean.signal=F, trade.summary=T, silent=T)

#*****************************************************************

# Strategy

# RAA_BAL = 40% Equity; 40% Real; 20% Bonds. Equity split between value and momentum. Risk-Managed.

# RAA_MOD = 60% Equity; 20% Real; 20% Bonds. Equity split between value and momentum. Risk-Managed.

# RAA_AGG = 80% Equity; 10% Real; 10% Bonds. Equity split between value and momentum. Risk-Managed.

#*****************************************************************

# RAA_MOD

target = list(

US.VAL = 60/4,

US.MOM = 60/4,

INT.VAL = 60/4,

INT.MOM = 60/4,

REIT = 20/2,

COM = 20/2,

US.BOND = 20

)

target.allocation = match(names(prices), toupper(names(target)))

target.allocation = unlist(target)[target.allocation] / 100

sma = bt.apply.matrix(prices, SMA, 10)

sma.signal = prices > sma

sma.signal = ifna(sma.signal, F)

mom = prices / mlag(prices, 10) - 1

mom.signal = mom > 0

mom.signal = ifna(mom.signal, F)

# alternative

mom.cash = data$prices$CASH / mlag(data$prices$CASH, 12) - 1

mom.signal = mom > as.vector(mom.cash)

mom.signal = ifna(mom.signal, F)

weight = iif(sma.signal & mom.signal, 1, iif(sma.signal | mom.signal, 0.5, 0)) * rep.row(target.allocation, nperiods)

weight = ifna(weight, 0)

weight$CASH = 1 - rowSums(weight)

data$weight[] = NA

data$weight[period.ends,] = weight[period.ends,]

models$RAA = bt.run.share(data, clean.signal=F, trade.summary=T, silent=T)

print(last(weight[period.ends,], 24))| SP500 | EAFE | REIT | COM | US.BOND | US.VAL | US.MOM | INT.VAL | INT.MOM | CASH | |

|---|---|---|---|---|---|---|---|---|---|---|

| 2013-04-01 | 0 | 0 | 0.10 | 0.05 | 0.2 | 0.15 | 0.15 | 0.150 | 0.150 | 0.050 |

| 2013-05-01 | 0 | 0 | 0.10 | 0.00 | 0.0 | 0.15 | 0.15 | 0.150 | 0.150 | 0.300 |

| 2013-06-01 | 0 | 0 | 0.10 | 0.00 | 0.0 | 0.15 | 0.15 | 0.150 | 0.150 | 0.300 |

| 2013-07-01 | 0 | 0 | 0.10 | 0.00 | 0.0 | 0.15 | 0.15 | 0.150 | 0.150 | 0.300 |

| 2013-08-01 | 0 | 0 | 0.05 | 0.00 | 0.0 | 0.15 | 0.15 | 0.150 | 0.150 | 0.350 |

| 2013-09-01 | 0 | 0 | 0.05 | 0.00 | 0.0 | 0.15 | 0.15 | 0.150 | 0.150 | 0.350 |

| 2013-10-01 | 0 | 0 | 0.10 | 0.00 | 0.0 | 0.15 | 0.15 | 0.150 | 0.150 | 0.300 |

| 2013-11-01 | 0 | 0 | 0.00 | 0.00 | 0.0 | 0.15 | 0.15 | 0.150 | 0.150 | 0.400 |

| 2013-12-01 | 0 | 0 | 0.00 | 0.00 | 0.0 | 0.15 | 0.15 | 0.150 | 0.150 | 0.400 |

| 2014-01-01 | 0 | 0 | 0.05 | 0.00 | 0.1 | 0.15 | 0.15 | 0.150 | 0.150 | 0.250 |

| 2014-02-01 | 0 | 0 | 0.05 | 0.05 | 0.1 | 0.15 | 0.15 | 0.150 | 0.150 | 0.200 |

| 2014-03-01 | 0 | 0 | 0.10 | 0.10 | 0.1 | 0.15 | 0.15 | 0.150 | 0.150 | 0.100 |

| 2014-04-01 | 0 | 0 | 0.10 | 0.10 | 0.2 | 0.15 | 0.15 | 0.150 | 0.150 | 0.000 |

| 2014-05-01 | 0 | 0 | 0.10 | 0.10 | 0.2 | 0.15 | 0.15 | 0.150 | 0.150 | 0.000 |

| 2014-06-01 | 0 | 0 | 0.10 | 0.05 | 0.2 | 0.15 | 0.15 | 0.150 | 0.150 | 0.050 |

| 2014-07-01 | 0 | 0 | 0.10 | 0.00 | 0.2 | 0.15 | 0.15 | 0.075 | 0.075 | 0.250 |

| 2014-08-01 | 0 | 0 | 0.10 | 0.00 | 0.2 | 0.15 | 0.15 | 0.000 | 0.075 | 0.325 |

| 2014-09-01 | 0 | 0 | 0.10 | 0.00 | 0.2 | 0.15 | 0.15 | 0.000 | 0.000 | 0.400 |

| 2014-10-01 | 0 | 0 | 0.10 | 0.00 | 0.2 | 0.15 | 0.15 | 0.000 | 0.000 | 0.400 |

| 2014-11-01 | 0 | 0 | 0.10 | 0.00 | 0.2 | 0.15 | 0.15 | 0.000 | 0.000 | 0.400 |

| 2014-12-01 | 0 | 0 | 0.10 | 0.00 | 0.2 | 0.15 | 0.15 | 0.000 | 0.000 | 0.400 |

| 2015-01-01 | 0 | 0 | 0.10 | 0.00 | 0.2 | 0.15 | 0.15 | 0.000 | 0.000 | 0.400 |

| 2015-02-01 | 0 | 0 | 0.10 | 0.00 | 0.2 | 0.15 | 0.15 | 0.000 | 0.075 | 0.325 |

| 2015-03-01 | 0 | 0 | 0.10 | 0.00 | 0.2 | 0.15 | 0.15 | 0.000 | 0.075 | 0.325 |

#*****************************************************************

# Report

#*****************************************************************

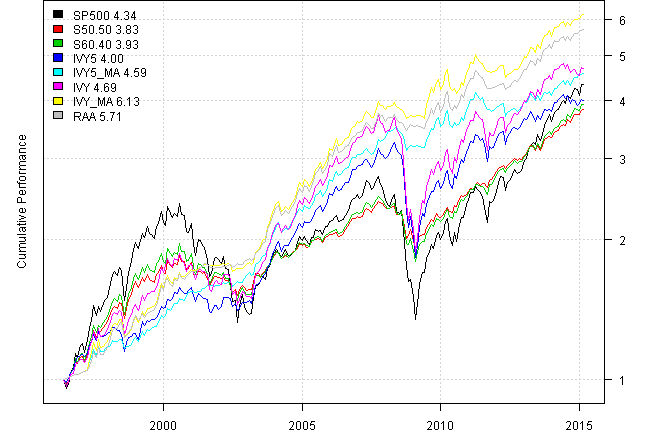

#strategy.performance.snapshoot(models, T)

plotbt(models, plotX = T, log = 'y', LeftMargin = 3, main = NULL)

mtext('Cumulative Performance', side = 2, line = 1)

print(plotbt.strategy.sidebyside(models, make.plot=F, return.table=T,perfromance.fn = engineering.returns.kpi))| SP500 | S50.50 | S60.40 | IVY5 | IVY5_MA | IVY | IVY_MA | RAA | |

|---|---|---|---|---|---|---|---|---|

| Period | Jun1996 - Mar2015 | Jun1996 - Mar2015 | Jun1996 - Mar2015 | Jun1996 - Mar2015 | Jun1996 - Mar2015 | Jun1996 - Mar2015 | Jun1996 - Mar2015 | Jun1996 - Mar2015 |

| Cagr | 8.14 | 7.42 | 7.57 | 7.67 | 8.46 | 8.59 | 10.15 | 9.74 |

| Sharpe | 0.58 | 0.95 | 0.84 | 0.72 | 1.25 | 0.68 | 1.21 | 1.28 |

| DVR | 0.35 | 0.84 | 0.7 | 0.66 | 1.22 | 0.6 | 1.17 | 1.24 |

| R2 | 0.6 | 0.88 | 0.83 | 0.91 | 0.97 | 0.88 | 0.97 | 0.97 |

| Volatility | 15.47 | 7.86 | 9.2 | 11.16 | 6.67 | 13.43 | 8.24 | 7.47 |

| MaxDD | -50.79 | -21.3 | -27.81 | -43.49 | -11.21 | -49.18 | -11.17 | -9.35 |

| Exposure | 99.56 | 99.56 | 99.56 | 99.56 | 99.56 | 99.56 | 99.56 | 99.56 |

| Win.Percent | 100 | 100 | 100 | 59.09 | 65.15 | 59.82 | 64.98 | 64.48 |

| Avg.Trade | 334.12 | 141.32 | 146.46 | 0.14 | 0.17 | 0.09 | 0.12 | 0.13 |

| Profit.Factor | NaN | NaN | NaN | 1.49 | 1.88 | 1.5 | 2.03 | 1.98 |

| Num.Trades | 1 | 2 | 2 | 1117 | 921 | 2016 | 1545 | 1354 |

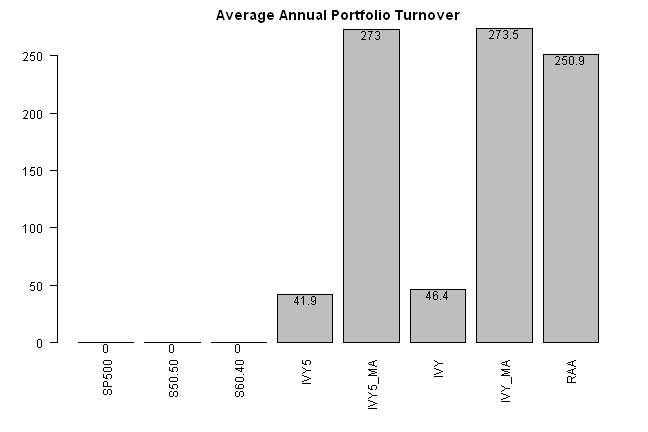

layout(1)

barplot.with.labels(sapply(models, compute.turnover, data), 'Average Annual Portfolio Turnover')

(this report was produced on: 2015-03-19)