Review of Momentum and Markowitz A Golden Combination paper

04 Jun 2015To install Systematic Investor Toolbox (SIT) please visit About page.

The Momentum and Markowitz: A Golden Combination (2015) by Keller, Butler, Kipnis paper is a review of practitioner’s tools to make mean variance optimization portfolio a viable solution. In particular, authors suggest and test:

- adding maximum weight limits and

- adding target volatility constraint

to control solution of mean variance optimization.

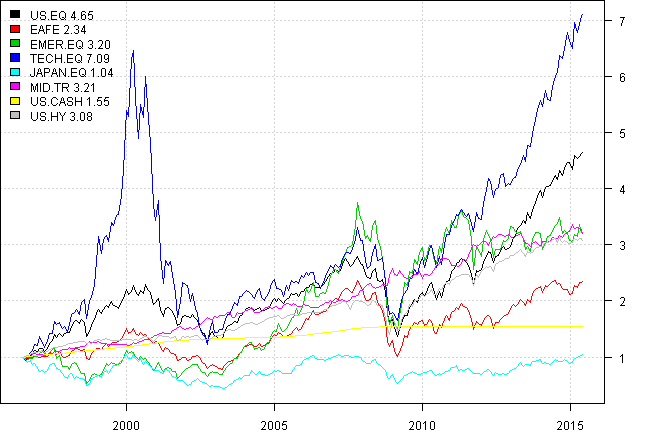

Below I will have a look at the results for the 8 asset universe:

- S&P 500

- EAFE

- Emerging Markets

- US Technology Sector

- Japanese Equities

- 10-Year Treasuries

- T-Bills

- High Yield Bonds

First, let’s load historical data for all assets

#*****************************************************************

# Load historical data

#*****************************************************************

library(SIT)

load.packages('quantmod')

# load saved Proxies Raw Data, data.proxy.raw

# please see http://systematicinvestor.github.io/Data-Proxy/ for more details

load('data/data.proxy.raw.Rdata')

N8.tickers = '

US.EQ = VTI + VTSMX + VFINX

EAFE = EFA + VDMIX + VGTSX

EMER.EQ = EEM + VEIEX

TECH.EQ = QQQ + ^NDX

JAPAN.EQ = EWJ + FJPNX

MID.TR = IEF + VFITX

US.CASH = BIL + TB3M,

US.HY = HYG + VWEHX

'

data = env()

getSymbols.extra(N8.tickers, src = 'yahoo', from = '1970-01-01', env = data, raw.data = data.proxy.raw, set.symbolnames = T, auto.assign = T)

for(i in data$symbolnames) data[[i]] = adjustOHLC(data[[i]], use.Adjusted=T)

bt.prep(data, align='remove.na', fill.gaps = T)Next, let’s test the functionality of kellerCLAfun from Appendix A

#*****************************************************************

# Run tests, monthly data - works

#*****************************************************************

data = bt.change.periodicity(data, periodicity = 'months')

plota.matplot(scale.one(data$prices))

prices = data$prices

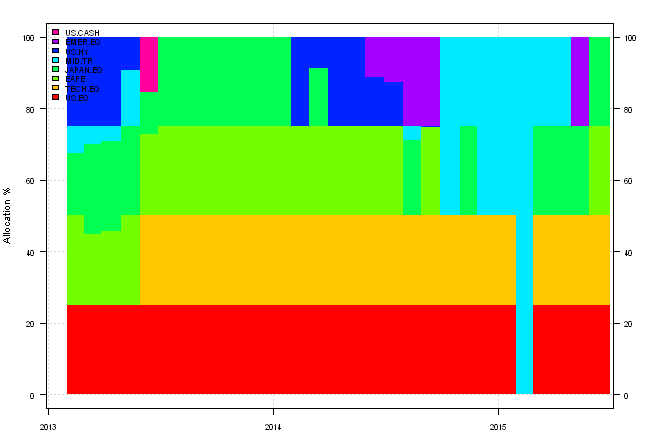

res = kellerCLAfun(prices, returnWeights = T, 0.25, 0.1, c('US.CASH', 'MID.TR'))

plotbt.transition.map(res[[1]]['2013::'])

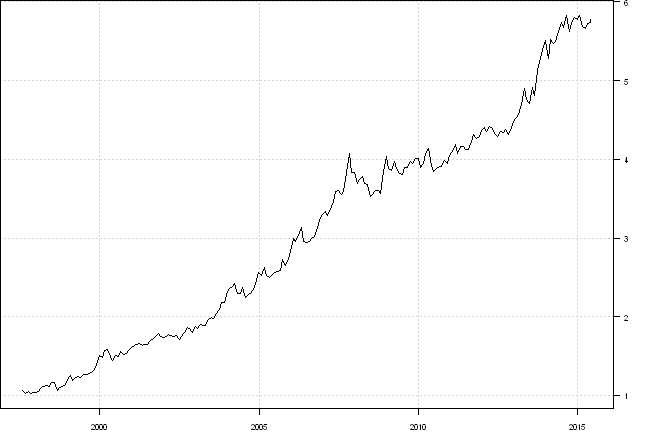

plota(cumprod(1 + res[[2]]), type='l')

Next, let’s create a benchmark and set up commision structure to be used for all tests.

#*****************************************************************

# Create a benchmark

#*****************************************************************

models = list()

commission = list(cps = 0.01, fixed = 10.0, percentage = 0.0)

data$weight[] = NA

data$weight$US.EQ = 1

data$weight[1:12,] = NA

models$US.EQ = bt.run.share(data, clean.signal=T, commission=commission, trade.summary=T, silent=T)Next, let’s take weights from the kellerCLAfun and use them to create a back-test

#*****************************************************************

# transform kellerCLAfun into model results

#*****************************************************************

#models$CLA = list(weight = res[[1]], ret = res[[2]], equity = cumprod(1 + res[[2]]), type = "weight")

obj = list(weights = list(CLA = res[[1]]), period.ends = index(res[[1]]))

models = c(models, create.strategies(obj, data, commission=commission, trade.summary=T, silent=T)$models)We can easily replicate same results with base SIT functionality

#*****************************************************************

# Replicate using base SIT functionality

#*****************************************************************

weight.limit = data.frame(last(prices))

weight.limit[] = 0.25

weight.limit$US.CASH = weight.limit$MID.TR = 1

obj = portfolio.allocation.helper(data$prices,

periodicity = 'months', lookback.len = 12, silent=T,

const.ub = weight.limit,

create.ia.fn = function(hist.returns, index, nperiod) {

ia = create.ia(hist.returns, index, nperiod)

ia$expected.return = (last(hist.returns,1) + colSums(last(hist.returns,3)) +

colSums(last(hist.returns,6)) + colSums(last(hist.returns,12))) / 22

ia

},

min.risk.fns = list(

TRISK = target.risk.portfolio(target.risk = 0.1, annual.factor=12)

)

)

models = c(models, create.strategies(obj, data, commission=commission, trade.summary=T, silent=T)$models)Another idea is to use Pierre Chretien’s Averaged Input Assumptions

#*****************************************************************

# Let's use Pierre's Averaged Input Assumptions

#*****************************************************************

obj = portfolio.allocation.helper(data$prices,

periodicity = 'months', lookback.len = 12, silent=T,

const.ub = weight.limit,

create.ia.fn = create.ia.averaged(c(1,3,6,12), 0),

min.risk.fns = list(

TRISK.AVG = target.risk.portfolio(target.risk = 0.1, annual.factor=12)

)

)

models = c(models, create.strategies(obj, data, commission=commission, trade.summary=T, silent=T)$models)Finally we are ready to look at the results

#*****************************************************************

# Plot back-test

#*****************************************************************

models = bt.trim(models)

#strategy.performance.snapshoot(models, T)

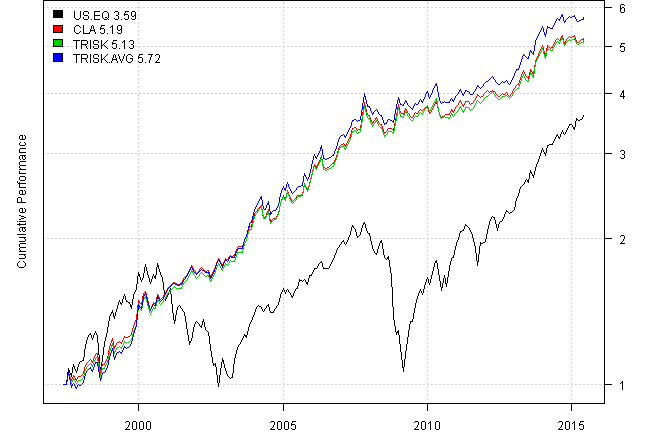

plotbt(models, plotX = T, log = 'y', LeftMargin = 3, main = NULL)

mtext('Cumulative Performance', side = 2, line = 1)

print(plotbt.strategy.sidebyside(models, make.plot=F, return.table=T, perfromance.fn=engineering.returns.kpi)) | US.EQ | CLA | TRISK | TRISK.AVG | |

|---|---|---|---|---|

| Period | May1997 - Jun2015 | May1997 - Jun2015 | May1997 - Jun2015 | May1997 - Jun2015 |

| Cagr | 7.36 | 9.57 | 9.49 | 10.16 |

| Sharpe | 0.53 | 1.02 | 1.01 | 1.04 |

| DVR | 0.33 | 1 | 0.98 | 1.01 |

| R2 | 0.63 | 0.98 | 0.97 | 0.97 |

| Volatility | 15.84 | 9.32 | 9.42 | 9.72 |

| MaxDD | -50.84 | -13.65 | -13.65 | -13.65 |

| Exposure | 99.08 | 99.08 | 99.08 | 99.08 |

| Win.Percent | 100 | 64.57 | 59.85 | 59.28 |

| Avg.Trade | 259.48 | 0.26 | 0.18 | 0.19 |

| Profit.Factor | NaN | 1.93 | 1.87 | 1.93 |

| Num.Trades | 1 | 717 | 1066 | 1051 |

layout(1)

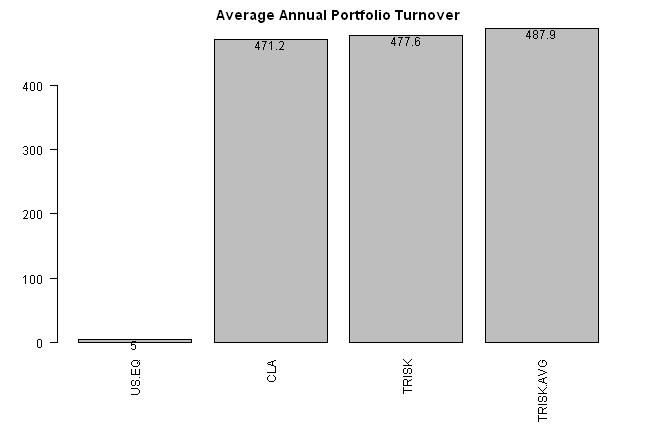

barplot.with.labels(sapply(models, compute.turnover, data), 'Average Annual Portfolio Turnover')

Our replication results are almost identical results to the results using kellerCLAfun.

Using Averaged Input Assumptions produces slightly better results.

I guess the main point that a reader should remember from reading Momentum and Markowitz: A Golden Combination (2015) by Keller, Butler, Kipnis paper is that it is a bad idea to blindly use the optimizer. Instead, you should apply common sense heuristics mentioned in the paper to make solution robust across time and various universes.

Supporting functions:

#*****************************************************************

# Appendix B. CLA code (in R) by Ilya Kipnis (QuantStratTradeR10) SSRN-id2606884.pdf

#*****************************************************************

require(quantmod)

require(PerformanceAnalytics)

require(TTR)

CCLA <- function(covMat, retForecast, maxIter = 1000,

verbose = FALSE, scale = 252,

weightLimit = .7, volThresh = .1)

{

if(length(retForecast) > length(unique(retForecast))) {

sequentialNoise <- seq(1:length(retForecast)) * 1e-12

retForecast <- retForecast + sequentialNoise

}

#initialize original out/in/up status

if(length(weightLimit) == 1) {

weightLimit <- rep(weightLimit, ncol(covMat))

}

# sort return forecasts

rankForecast <- length(retForecast) - rank(retForecast) + 1

remainingWeight <- 1 #have 100% of weight to allocate

upStatus <- inStatus <- rep(0, ncol(covMat))

i <- 1

# find max return portfolio

while(remainingWeight > 0) {

securityLimit <- weightLimit[rankForecast == i]

if(securityLimit < remainingWeight) {

upStatus[rankForecast == i] <- 1 #if we can't invest all remaining weight into the security

remainingWeight <- remainingWeight - securityLimit

} else {

inStatus[rankForecast == i] <- 1

remainingWeight <- 0

}

i <- i + 1

}

#initial matrices (W, H, K, identity, negative identity)

covMat <- as.matrix(covMat)

retForecast <- as.numeric(retForecast)

init_W <- cbind(2*covMat, rep(-1, ncol(covMat)))

init_W <- rbind(init_W, c(rep(1, ncol(covMat)), 0))

H_vec <- c(rep(0, ncol(covMat)), 1)

K_vec <- c(retForecast, 0)

negIdentity <- -1*diag(ncol(init_W))

identity <- diag(ncol(init_W))

matrixDim <- nrow(init_W)

weightLimMat <- matrix(rep(weightLimit, matrixDim), ncol=ncol(covMat), byrow=TRUE)

#out status is simply what isn't in or up

outStatus <- 1 - inStatus - upStatus

#initialize expected volatility/count/turning points data structure

expVol <- Inf

lambda <- 100

count <- 0

turningPoints <- list()

while(lambda > 0 & count < maxIter) {

#old lambda and old expected volatility for use with numerical algorithms

oldLambda <- lambda

oldVol <- expVol

count <- count + 1

#compute W, A, B

inMat <- matrix(rep(c(inStatus, 1), matrixDim), nrow = matrixDim, byrow = TRUE)

upMat <- matrix(rep(c(upStatus, 0), matrixDim), nrow = matrixDim, byrow = TRUE)

outMat <- matrix(rep(c(outStatus, 0), matrixDim), nrow = matrixDim, byrow = TRUE)

W <- inMat * init_W + upMat * identity + outMat * negIdentity

inv_W <- solve(W)

modified_H <- H_vec - rowSums(weightLimMat* upMat[,-matrixDim] * init_W[,-matrixDim])

A_vec <- inv_W %*% modified_H

B_vec <- inv_W %*% K_vec

#remove the last elements from A and B vectors

truncA <- A_vec[-length(A_vec)]

truncB <- B_vec[-length(B_vec)]

#compute in Ratio (aka Ratio(1) in Kwan.xls)

inRatio <- rep(0, ncol(covMat))

inRatio[truncB > 0] <- -truncA[truncB > 0]/truncB[truncB > 0]

#compute up Ratio (aka Ratio(2) in Kwan.xls)

upRatio <- rep(0, ncol(covMat))

upRatioIndices <- which(inStatus==TRUE & truncB < 0)

if(length(upRatioIndices) > 0) {

upRatio[upRatioIndices] <- (weightLimit[upRatioIndices] - truncA[upRatioIndices]) / truncB[upRatioIndices]

}

#find lambda -- max of up and in ratios

maxInRatio <- max(inRatio)

maxUpRatio <- max(upRatio)

lambda <- max(maxInRatio, maxUpRatio)

#compute new weights

wts <- inStatus*(truncA + truncB * lambda) + upStatus * weightLimit + outStatus * 0

#compute expected return and new expected volatility

expRet <- t(retForecast) %*% wts

expVol <- sqrt(wts %*% covMat %*% wts) * sqrt(scale)

#create turning point data row and append it to turning points

turningPoint <- cbind(count, expRet, lambda, expVol, t(wts))

colnames(turningPoint) <- c("CP", "Exp. Ret.", "Lambda", "Exp. Vol.", colnames(covMat))

turningPoints[[count]] <- turningPoint

#binary search for volatility threshold -- if the first iteration is lower than the threshold,

#then immediately return, otherwise perform the binary search until convergence of lambda

if(oldVol == Inf & expVol < volThresh) {

turningPoints <- do.call(rbind, turningPoints)

threshWts <- tail(turningPoints, 1)

return(list(turningPoints, threshWts))

} else if(oldVol > volThresh & expVol < volThresh) {

upLambda <- oldLambda

dnLambda <- lambda

meanLambda <- (upLambda + dnLambda)/2

while(upLambda - dnLambda > .00001) {

#compute mean lambda and recompute weights, expected return, and expected vol

meanLambda <- (upLambda + dnLambda)/2

wts <- inStatus*(truncA + truncB * meanLambda) + upStatus * weightLimit + outStatus * 0

expRet <- t(retForecast) %*% wts

expVol <- sqrt(wts %*% covMat %*% wts) * sqrt(scale)

#if new expected vol is less than threshold, mean becomes lower bound

#otherwise, it becomes the upper bound, and loop repeats

if(expVol < volThresh) {

dnLambda <- meanLambda

} else {

upLambda <- meanLambda

}

}

#once the binary search completes, return those weights, and the corner points

#computed until the binary search. The corner points aren't used anywhere, but they're there.

threshWts <- cbind(count, expRet, meanLambda, expVol, t(wts))

colnames(turningPoint) <- colnames(threshWts) <- c("CP", "Exp. Ret.", "Lambda", "Exp. Vol.", colnames(covMat))

turningPoints[[count]] <- turningPoint

turningPoints <- do.call(rbind, turningPoints)

return(list(turningPoints, threshWts))

}

#this is only run for the corner points during which binary search doesn't take place

#change status of security that has new lambda

if(maxInRatio > maxUpRatio) {

inStatus[inRatio == maxInRatio] <- 1 - inStatus[inRatio == maxInRatio]

upStatus[inRatio == maxInRatio] <- 0

} else {

upStatus[upRatio == maxUpRatio] <- 1 - upStatus[upRatio == maxUpRatio]

inStatus[upRatio == maxUpRatio] <- 0

}

outStatus <- 1 - inStatus - upStatus

}

#we only get here if the volatility threshold isn't reached

#can actually happen if set sufficiently low

turningPoints <- do.call(rbind, turningPoints)

threshWts <- tail(turningPoints, 1)

return(list(turningPoints, threshWts))

}

sumIsNa <- function(column) {

return(sum(is.na(column)))

}

returnForecast <- function(prices) {

forecast <- (ROC(prices, n = 1, type="discrete") + ROC(prices, n = 3, type="discrete") +

ROC(prices, n = 6, type="discrete") + ROC(prices, n = 12, type="discrete"))/22

forecast <- as.numeric(tail(forecast, 1))

return(forecast)

}

kellerCLAfun <- function(prices, returnWeights = FALSE,

weightLimit, volThresh, uncappedAssets)

{

if(sum(colnames(prices) %in% uncappedAssets) == 0) {

stop("No assets are uncapped.")

}

#initialize data structure to contain our weights

weights <- list()

#compute returns

returns <- Return.calculate(prices)

returns[1,] <- 0 #impute first month with zeroes

ep <- endpoints(returns, on = "months")

for(i in 2:(length(ep) - 12)) {

priceSubset <- prices[ep[i]:ep[i+12]] #subset prices

retSubset <- returns[ep[i]:ep[i+12]] #subset returns

assetNAs <- apply(retSubset, 2, sumIsNa)

zeroNAs <- which(assetNAs == 0)

priceSubset <- priceSubset[, zeroNAs]

retSubset <- retSubset[, zeroNAs]

#remove perfectly correlated assets

retCors <- cor(retSubset)

diag(retCors) <- NA

corMax <- round(apply(retCors, 2, max, na.rm = TRUE), 7)

while(max(corMax) == 1) {

ones <- which(corMax == 1)

valid <- which(!names(corMax) %in% uncappedAssets)

toRemove <- intersect(ones, valid)

toRemove <- max(valid)

retSubset <- retSubset[, -toRemove]

priceSubset <- priceSubset[, -toRemove]

retCors <- cor(retSubset)

diag(retCors) <- NA

corMax <- round(apply(retCors, 2, max, na.rm = TRUE), 7)

}

covMat <- cov(retSubset) #compute covariance matrix

#Dr. Keller's return forecast

retForecast <- returnForecast(priceSubset)

uncappedIndex <- which(colnames(covMat) %in% uncappedAssets)

weightLims <- rep(weightLimit, ncol(covMat))

weightLims[uncappedIndex] <- 1

cla <- CCLA(covMat = covMat, retForecast = retForecast, scale = 12,

weightLimit = weightLims, volThresh = volThresh) #run CCLA algorithm

CPs <- cla[[1]] #corner points

wts <- cla[[2]] #binary search volatility targeting -- change this line and the next

#if using max sharpe ratio golden search

wts <- wts[, 5:ncol(wts)] #from 5th column to the end

if(length(wts) == 1) {

names(wts) <- colnames(covMat)

}

zeroes <- rep(0, ncol(prices) - length(wts))

names(zeroes) <- colnames(prices)[!colnames(prices) %in% names(wts)]

wts <- c(wts, zeroes)

wts <- wts[colnames(prices)]

#append to weights

wts <- xts(t(wts), order.by=tail(index(retSubset), 1))

weights[[i]] <- wts

}

weights <- do.call(rbind, weights)

#compute strategy returns

stratRets <- Return.portfolio(returns, weights = weights)

if(returnWeights) {

return(list(weights, stratRets))

}

return(stratRets)

}(this report was produced on: 2015-06-04)