Quarterly Tactical Strategy

16 Feb 2015To install Systematic Investor Toolbox (SIT) please visit About page.

Another interesting post by QuantStrat TradeR: The Quarterly Tactical Strategy (aka QTS)

The Quarterly Tactical Strategy was published by Cliff Smith.

Below I will try to adapt a code from the post:

#*****************************************************************

# Load historical data

#*****************************************************************

library(SIT)

load.packages('quantmod')

tickers = '

US.SC = VB + NAESX # U.S. Small Cap

EM.BOND = VWOB + PREMX # Emerging Market Government Bond

EM.EQ = VWO + VEIEX # Emerging Markets

US.CORP.BOND = VCIT + VFICX # Intermediate Corporate Bond

US.MBS = VMBS + VFIIX # Mortgage-Backed Bonds

US.LC = SPY + VFINX # S&P 500

US.REIT = VNQ + VGSIX # MSCI U.S. REIT

INTL.EQ = VEU + VGTSX # FTSE All-World ex-U.S.

CASH = TLT + VUSTX # Long-Tern Treasury

'

data <- new.env()

getSymbols.extra(tickers, src = 'yahoo', from = '1970-01-01', env = data, set.symbolnames = T, auto.assign = T)

for(i in data$symbolnames) data[[i]] = adjustOHLC(data[[i]], use.Adjusted=T)

#print(bt.start.dates(data))

bt.prep(data, align='remove.na', fill.gaps = T)

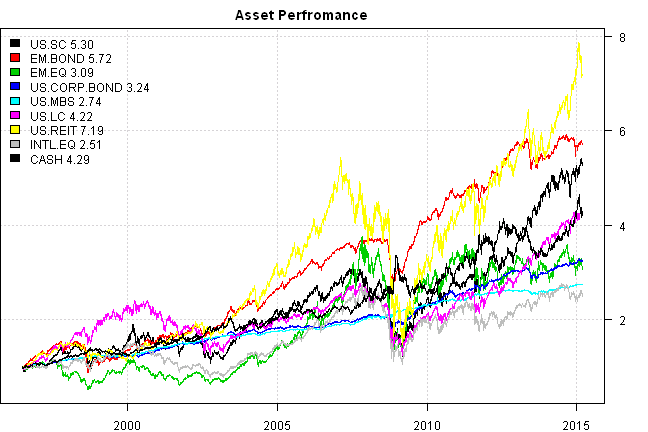

# Check data

plota.matplot(scale.one(data$prices),main='Asset Perfromance')

#*****************************************************************

# Setup

#*****************************************************************

data$universe = data$prices > 0

# do not allocate to CASH, or BENCH

data$universe$CASH = NA

prices = data$prices * data$universe

n = ncol(prices)

nperiods = nrow(prices)

frequency = 'quarters'

# find period ends, can be 'weeks', 'months', 'quarters', 'years'

period.ends = endpoints(prices, frequency)

period.ends = period.ends[period.ends > 0]

models = list()

commission = list(cps = 0.01, fixed = 10.0, percentage = 0.0)

# lag prices by 1 day

#prices = mlag(prices)

#*****************************************************************

# Equal Weight each re-balancing period

#******************************************************************

data$weight[] = NA

data$weight[period.ends,] = ntop(prices[period.ends,], n)

models$ew = bt.run.share(data, clean.signal=F, commission = commission, trade.summary=T, silent=T)

#*****************************************************************

# Strategy:

#

# Select the top-ranked asset each quarter based on

# 5-month and 20-day total returns weighted 50% each.

#

# A cash filter must be passed for the top-ranked mutual fund to be selected

# in any given period. The cash filter is the 3-month moving average.

#******************************************************************

mom.5m = prices / mlag(prices, 5*21) -1

mom.20d = prices / mlag(prices, 20) -1

# compute 3 month moving average

sma = bt.apply.matrix(prices, SMA, 3*21)

# go to cash if prices falls below 3 month moving average

go2cash = prices <= sma

go2cash.d = ifna(go2cash, T)

# compute moving average in months

sma = bt.apply.matrix(prices, SMA, 3, periodicity='months')

go2cash = prices <= sma

go2cash.m = ifna(go2cash, T)

# all logic below is done at period.ends

mom.5m = mom.5m[period.ends,]

mom.20d = mom.20d[period.ends,]

go2cash.d = go2cash.d[period.ends,]

go2cash.m = go2cash.m[period.ends,]

#*****************************************************************

# Rank total score

#*****************************************************************

# target allocation

target.allocation = ntop(0.5 * mom.5m + 0.5 * mom.20d ,1)

# If asset is above it's 3 month moving average it gets allocation

weight = iif(go2cash.d, 0, target.allocation)

# otherwise, it's weight is allocated to cash

weight$CASH = 1 - rowSums(weight)

data$weight[] = NA

data$weight[period.ends,] = weight

models$QTS.d = bt.run.share(data, clean.signal=F, commission = commission, trade.summary=T, silent=T)

# same but using monthly moving average to trigger go to cash

weight = iif(go2cash.m, 0, target.allocation)

weight$CASH = 1 - rowSums(weight)

data$weight[] = NA

data$weight[period.ends,] = weight

models$QTS.m = bt.run.share(data, clean.signal=F, commission = commission, trade.summary=T, silent=T)

#*****************************************************************

# Rank each component of total score first

#*****************************************************************

# target allocation

target.allocation[] = ntop(1.01 * bt.rank(mom.5m, F,T) + bt.rank(mom.20d, F,T) ,1)

# If asset is above it's 3 month moving average it gets allocation

weight = iif(go2cash.d, 0, target.allocation)

# otherwise, it's weight is allocated to cash

weight$CASH = 1 - rowSums(weight)

data$weight[] = NA

data$weight[period.ends,] = weight

models$QTS.RANK.d = bt.run.share(data, clean.signal=F, commission = commission, trade.summary=T, silent=T)

# same but using monthly moving average to trigger go to cash

weight = iif(go2cash.m, 0, target.allocation)

weight$CASH = 1 - rowSums(weight)

data$weight[] = NA

data$weight[period.ends,] = weight

models$QTS.RANK.m = bt.run.share(data, clean.signal=F, commission = commission, trade.summary=T, silent=T)

#*****************************************************************

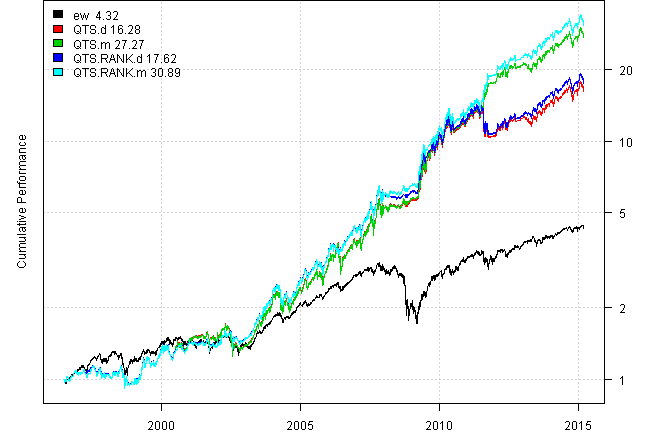

# Report

#*****************************************************************

#strategy.performance.snapshoot(models, T)

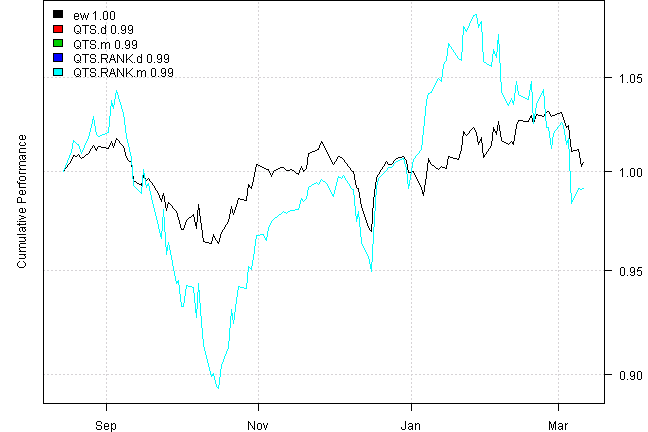

plotbt(models, plotX = T, log = 'y', LeftMargin = 3, main = NULL)

mtext('Cumulative Performance', side = 2, line = 1)

print(plotbt.strategy.sidebyside(models, make.plot=F, return.table=T))| ew | QTS.d | QTS.m | QTS.RANK.d | QTS.RANK.m | |

|---|---|---|---|---|---|

| Period | Jun1996 - Mar2015 | Jun1996 - Mar2015 | Jun1996 - Mar2015 | Jun1996 - Mar2015 | Jun1996 - Mar2015 |

| Cagr | 8.13 | 16.08 | 19.32 | 16.57 | 20.12 |

| Sharpe | 0.67 | 0.91 | 1.07 | 0.96 | 1.15 |

| DVR | 0.61 | 0.76 | 0.81 | 0.82 | 0.86 |

| Volatility | 12.89 | 18.28 | 17.99 | 17.54 | 17.32 |

| MaxDD | -44.61 | -26.78 | -26.78 | -25 | -19.39 |

| AvgDD | -1.55 | -3.09 | -3.01 | -2.87 | -2.77 |

| VaR | -1.16 | -1.79 | -1.75 | -1.71 | -1.69 |

| CVaR | -1.96 | -2.82 | -2.72 | -2.71 | -2.61 |

| Exposure | 99.98 | 99.98 | 99.98 | 99.98 | 99.98 |

Given that each quarter only one top fund is selected it is natural that strategy is sensitive to input parameters. However, the change in performance from go to cash rule based on 63 days vs 3 months is staggering.

Finally, let’s zoom in on various periods:

dates.range = c('2002-12-31::2014-08-15', '::2002-12-31', '2014-08-15::')

for(dates in dates.range) {

models1 = bt.trim(models, dates=dates)

plotbt(models1, plotX = T, log = 'y', LeftMargin = 3, main = NULL)

mtext('Cumulative Performance', side = 2, line = 1)

print(plotbt.strategy.sidebyside(models1, make.plot=F, return.table=T))

}

| ew | QTS.d | QTS.m | QTS.RANK.d | QTS.RANK.m | |

|---|---|---|---|---|---|

| Period | Dec2002 - Aug2014 | Dec2002 - Aug2014 | Dec2002 - Aug2014 | Dec2002 - Aug2014 | Dec2002 - Aug2014 |

| Cagr | 10.2 | 23.66 | 29.32 | 23.79 | 29.96 |

| Sharpe | 0.74 | 1.15 | 1.4 | 1.2 | 1.48 |

| DVR | 0.64 | 1.07 | 1.25 | 1.13 | 1.32 |

| Volatility | 14.5 | 20.3 | 19.86 | 19.34 | 19 |

| MaxDD | -44.61 | -25.99 | -25.99 | -25 | -19.13 |

| AvgDD | -1.43 | -2.89 | -2.79 | -2.61 | -2.49 |

| VaR | -1.36 | -2.06 | -1.98 | -1.86 | -1.81 |

| CVaR | -2.26 | -3.15 | -3.01 | -3.01 | -2.86 |

| Exposure | 100 | 100 | 100 | 100 | 100 |

| ew | QTS.d | QTS.m | QTS.RANK.d | QTS.RANK.m | |

|---|---|---|---|---|---|

| Period | Jun1996 - Dec2002 | Jul1996 - Dec2002 | Jul1996 - Dec2002 | Jul1996 - Dec2002 | Jul1996 - Dec2002 |

| Cagr | 5.18 | 5.19 | 5.11 | 6.27 | 6.2 |

| Sharpe | 0.56 | 0.43 | 0.42 | 0.51 | 0.5 |

| DVR | 0.4 | 0.32 | 0.32 | 0.41 | 0.41 |

| Volatility | 9.81 | 14.21 | 14.23 | 13.93 | 13.95 |

| MaxDD | -20.72 | -26.78 | -26.78 | -19.39 | -19.39 |

| AvgDD | -2.05 | -3.18 | -3.37 | -3.53 | -3.9 |

| VaR | -0.98 | -1.37 | -1.37 | -1.36 | -1.36 |

| CVaR | -1.43 | -2.15 | -2.15 | -2.11 | -2.11 |

| Exposure | 99.94 | 100 | 100 | 100 | 100 |

| ew | QTS.d | QTS.m | QTS.RANK.d | QTS.RANK.m | |

|---|---|---|---|---|---|

| Period | Aug2014 - Mar2015 | Aug2014 - Mar2015 | Aug2014 - Mar2015 | Aug2014 - Mar2015 | Aug2014 - Mar2015 |

| Cagr | 0.83 | -1.52 | -1.52 | -1.52 | -1.52 |

| Sharpe | 0.15 | -0.03 | -0.03 | -0.03 | -0.03 |

| DVR | 0.04 | -0.01 | -0.01 | -0.01 | -0.01 |

| Volatility | 8.15 | 15.71 | 15.71 | 15.71 | 15.71 |

| MaxDD | -5.29 | -14.33 | -14.33 | -14.33 | -14.33 |

| AvgDD | -1.03 | -3.38 | -3.38 | -3.38 | -3.38 |

| VaR | -0.89 | -1.94 | -1.94 | -1.94 | -1.94 |

| CVaR | -1.04 | -2.35 | -2.35 | -2.35 | -2.35 |

| Exposure | 100 | 100 | 100 | 100 | 100 |

(this report was produced on: 2015-03-12)