Leadership Details

16 Apr 2015To install Systematic Investor Toolbox (SIT) please visit About page.

Let’s continue with Run Leadership Rcpp post and look at results in more details

First, let’s load historical prices for S&P 500:

#*****************************************************************

# Load historical end of day data

#*****************************************************************

library(SIT)

load.packages('quantmod')

filename = 'big.test.Rdata'

if(!file.exists(filename)) {

tickers = nasdaq.100.components()

tickers = sp500.components()$tickers

data = env()

getSymbols.extra(tickers, src = 'yahoo', from = '1970-01-01', env = data, auto.assign = T)

rm.index = which(sapply(ls(data), function(i) is.null(data[[i]])))

if(any(rm.index)) env.del(names(rm.index), data)

for(i in ls(data)) data[[i]] = adjustOHLC(data[[i]], use.Adjusted=T)

#print(bt.start.dates(data))

bt.prep(data, align='keep.all', dates='2000::', fill.gaps=T)

# remove ones with little history

prices = data$prices

bt.prep.remove.symbols(data, which(

count(prices, side = 2) < 3*252 | is.na(last(prices))

))

# show the ones removed

print(setdiff(tickers,names(data$prices)))

prices = data$prices

save(prices, file=filename)

}

load(file=filename)

#*****************************************************************

# Helper functions

#*****************************************************************

# lead - lag sample function

rtest = function(ret, nwindow) {

nlag = floor(nwindow/2)

n = ncol(ret)

nperiod = nrow(ret)

out = array(0, c(n,n,nperiod))

index = !lower.tri(out[,,1])

for(i in nwindow:nperiod) {

temp = coredata(ret[(i-nwindow+1):i,])

temp.out = matrix(0, n,n)

for (c1 in 2:n) {

data1 = temp[,c1]

c2.index = 1:(c1-1)

data2 = temp[,c2.index,drop=F]

# if c1.cor : c2 -> c1 i.e. cor(data1[(lag+1):nwindow], data2[1:(nwindow-lag),])

c1.cor = rep(0,ncol(data2))

for (lag in 0:nlag) {

cor.temp = cor(data1[(lag+1):nwindow], data2[1:(nwindow-lag),])

c1.cor = c1.cor + pmax(cor.temp, 0)

}

c1.cor = c1.cor / (nlag + 1)

# if c2.cor : c1 -> c2 i.e. cor(data1[1:(nwindow-lag)], data2[(lag+1):nwindow,])

c2.cor = rep(0,ncol(data2))

for (lag in 1:nlag) {

cor.temp = cor(data1[1:(nwindow-lag)], data2[(lag+1):nwindow,])

c2.cor = c2.cor + pmax(cor.temp, 0)

}

c2.cor = c2.cor / nlag

# if c1.cor >= c2.cor hence c2 -> c1 i.e. cor(data1[(lag+1):nwindow], data2[1:(nwindow-lag),])

index = c1.cor >= c2.cor

if(any(index))

temp.out[c2.index[index], c1] = c1.cor[index]

# if c2.cor >= c1.cor hence c1 -> c2 i.e. cor(data1[1:(nwindow-lag)], data2[(lag+1):nwindow,])

index = !index

if(any(index))

temp.out[c1, c2.index[index]] = c2.cor[index]

}

out[,,i] = temp.out

}

out

}

# lead - lag sample function

rtest.one = function(ret, nwindow, c1.name, c2.name) {

c1 = which(colnames(ret) == c1.name)

c2 = which(colnames(ret) == c2.name)

if(c1 < c2) { # switch

temp = c2; c2 = c1; c1 = temp

temp = c2.name; c2.name = c1.name; c1.name = temp

}

nlag = floor(nwindow/2)

n = ncol(ret)

nperiod = nrow(ret)

out = array(NA, c(n,n,nperiod))

index = !lower.tri(out[,,1])

i = nperiod

temp = coredata(ret[(i-nwindow+1):i,])

temp.out = matrix(NA, n,n)

data1 = temp[,c1]

data2 = temp[,c2,drop=F]

c1.cor = c()

for (lag in 0:nlag) {

cor.temp = cor(data1[(lag+1):nwindow], data2[1:(nwindow-lag),])

c1.cor = c(c1.cor, cor.temp)

}

c2.cor = c()

for (lag in 1:nlag) {

cor.temp = cor(data1[1:(nwindow-lag)], data2[(lag+1):nwindow,])

c2.cor = c(c2.cor, cor.temp)

}

c1.cor.mean = sum(pmax(c1.cor,0)) / (nlag + 1)

c2.cor.mean = sum(pmax(c2.cor,0)) / nlag

# if c1.cor >= c2.cor hence c2 -> c1 i.e. cor(data1[(lag+1):nwindow], data2[1:(nwindow-lag),])

# if c2.cor >= c1.cor hence c1 -> c2 i.e. cor(data1[1:(nwindow-lag)], data2[(lag+1):nwindow,])

relationship = iif(c1.cor.mean >= c2.cor.mean, 'c2 -> c1', 'c1 -> c2')

list(

c1 = c1, c2 = c2, c1.name = c1.name, c2.name = c2.name,

x = -nlag:nlag,

y = c(c2.cor, c1.cor),

c1.cor = to.nice(c1.cor.mean),

c2.cor = to.nice(c2.cor.mean),

relationship = relationship,

c1.ret = ret[(i-nwindow+1):i,c1],

c2.ret = ret[(i-nwindow+1):i,c2]

)

}

# make plot

rtest.visualize = function(out) {

par(mar=c(5,4,4,5))

plot(out$x, out$y, type = "n", xlab='Lag', ylab='Correlation', las=1,

main = paste('c2 =', out$c2.name, out$c2.cor, 'vs c1 =', out$c1.name, out$c1.cor,

'\n', out$relationship)

)

col1 = col.add.alpha('blue',100)

polygon(c(first(out$x), out$x, last(out$x)), c(0, pmax(out$y,0), 0), col=col1, border=col1)

col1 = col.add.alpha('gray',200)

polygon(c(first(out$x), out$x, last(out$x)), c(0, pmin(out$y,0), 0), col=col1, border=col1)

abline(h=0, v=0)

lines(out$x, out$y, col='red')

lines(out$x, out$y, type='b', pch='+', col='red')

}

rtest.visualize.relationship = function(out) {

ylim = range(c(cumprod(1 + out$c1.ret), cumprod(1 + out$c2.ret)))

plota(cumprod(1 + out$c1.ret), type='l', ylim = ylim, col='black')

plota.lines(cumprod(1 + out$c2.ret), col='blue')

plota.legend(paste('c1', out$c1.name, ',c2', out$c2.name, ',', out$relationship), 'black,blue, red')

}

#*****************************************************************

# Run Lead Lag Correlation

#*****************************************************************

prices = prices[,]

n = ncol(prices)

nperiod = nrow(prices)

ret = prices / mlag(prices) - 1

index = (nperiod-20):nperiod

ret = ret[index,]

nperiod = nrow(ret)

nwindow = 15

#*****************************************************************

# Run Lead Lag Correlation

#*****************************************************************

# make sure to install [Rtools on windows](http://cran.r-project.org/bin/windows/Rtools/)

load.packages('Rcpp')

load.packages('RcppParallel')

# load Rcpp functions

sourceCpp('lead.lag.correlation.cpp')

c.cor = cp_run_leadership_smart(ret, nwindow, T)

# remove zero entries

clean.adj = function(adj.mat, threshold = 0.5) {

adj.mat[ abs(adj.mat) < threshold] = 0

keep.index = (rowSums(adj.mat != 0) >= 1) | (colSums(adj.mat != 0) >= 1)

adj.mat = adj.mat[keep.index, keep.index]

adj.mat

}

adj.mat = c.cor[,,nperiod-1]

rownames(adj.mat) = colnames(adj.mat) = colnames(prices)

adj.mat = clean.adj(adj.mat, 0.38)

temp = adj.mat

temp[temp == 0] = NA

print(to.percent(temp))| AIG | APA | ED | NEM | PPL | PVH | RL | STT | XL | |

|---|---|---|---|---|---|---|---|---|---|

| AIG | |||||||||

| APA | |||||||||

| ED | 38.18% | ||||||||

| NEM | |||||||||

| PPL | |||||||||

| PVH | 41.76% | ||||||||

| RL | 42.19% | 38.71% | |||||||

| STT | 38.28% | ||||||||

| XL | 38.30% |

# examine some pairs

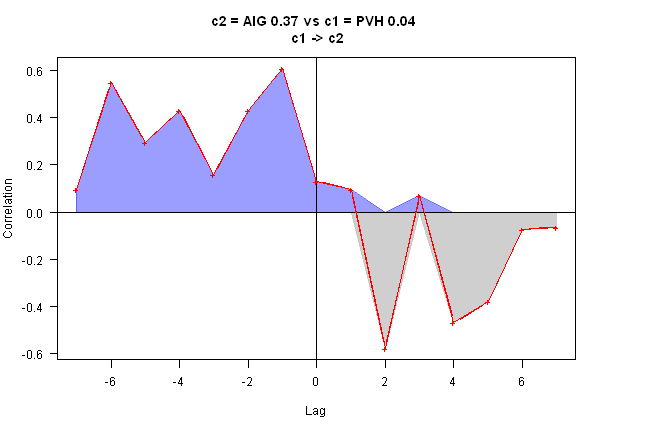

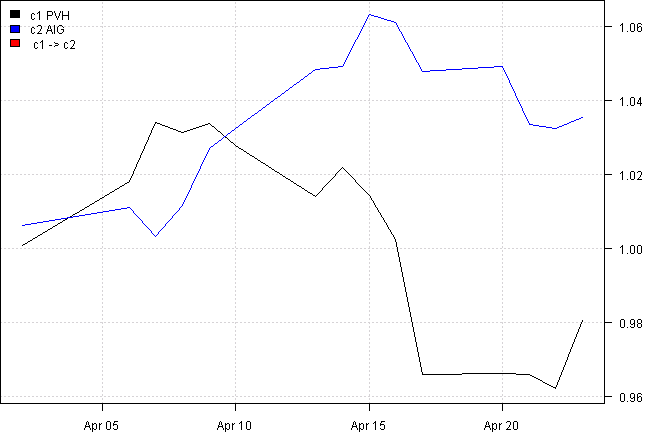

out = rtest.one(ret, nwindow, 'AIG', 'PVH')

rtest(ret[,c(out$c2,out$c1)], nwindow)[,,nperiod] [,1] [,2] [1,] 0.0000000 0 [2,] 0.3668593 0

rtest.visualize(out)

rtest.visualize.relationship(out)

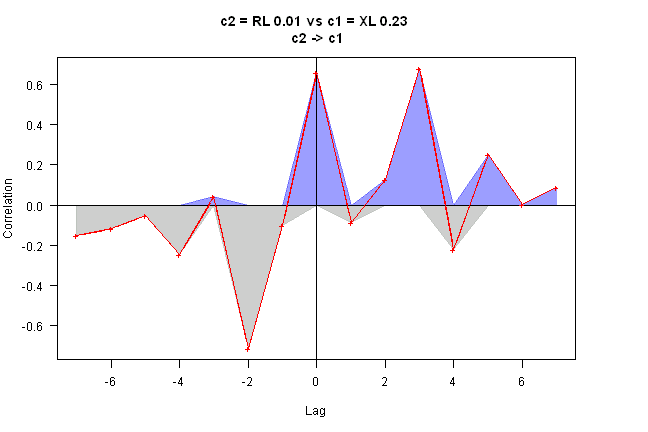

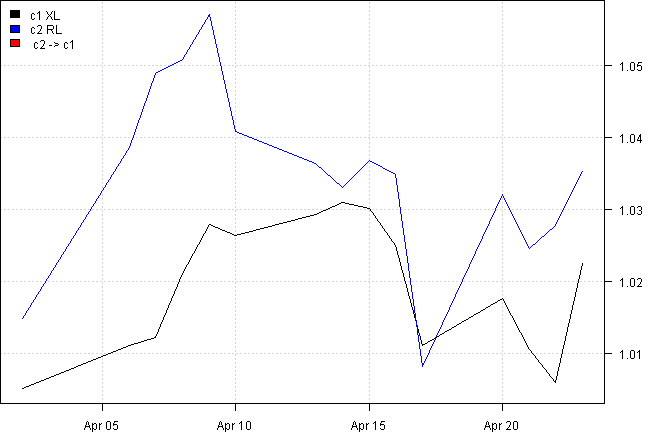

out = rtest.one(ret, nwindow, 'XL', 'RL')

rtest(ret[,c(out$c2,out$c1)], nwindow)[,,nperiod] [,1] [,2] [1,] 0 0.2261738 [2,] 0 0.0000000

rtest.visualize(out)

rtest.visualize.relationship(out)

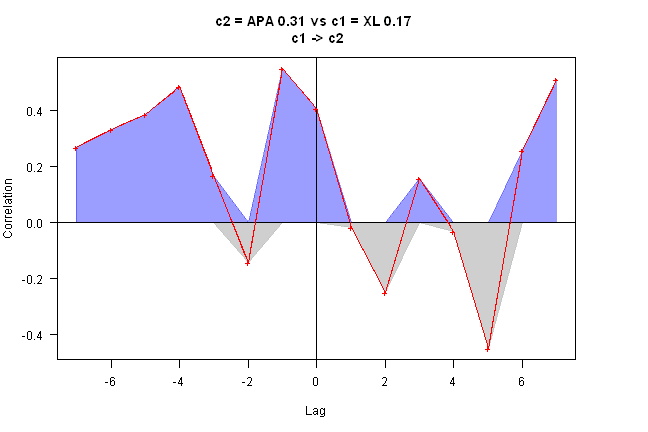

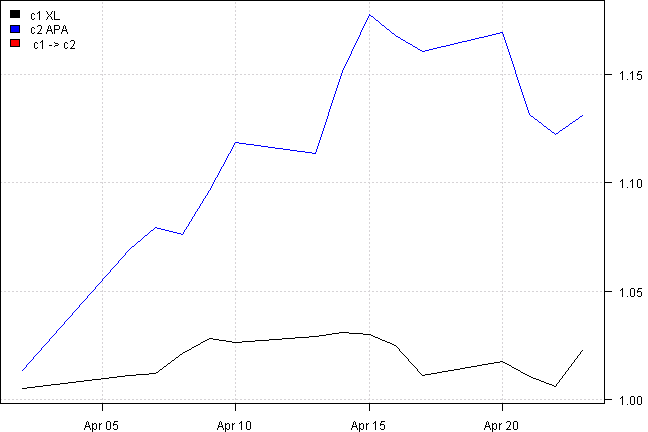

out = rtest.one(ret, nwindow, 'APA', 'XL')

rtest(ret[,c(out$c2,out$c1)], nwindow)[,,nperiod] [,1] [,2] [1,] 0.0000000 0 [2,] 0.3136286 0

rtest.visualize(out)

rtest.visualize.relationship(out)

# adj.mat(row,col) is mapped to

#

# |from |to |value |

# |:----|:---|:----------------|

# |row |col |adj.mat(row,col) |

load.packages('igraph')

g = graph.adjacency(adj.mat,weighted=TRUE)

get.data.frame(g)from to weight 1 ED PPL 0.3817913 2 PVH AIG 0.4175742 3 RL AIG 0.4219342 4 RL XL 0.3870656 5 STT NEM 0.3828356 6 XL APA 0.3830476

print(g)IGRAPH DNW- 9 6 -- + attr: name (v/c), weight (e/n)

(this report was produced on: 2015-04-24)