Financial Turbulence Example

01 Dec 2012To install Systematic Investor Toolbox (SIT) please visit About page.

Today, I want to highlight the Financial Turbulence Index idea introduced by Mark Kritzman and Yuanzhen Li in the Skulls, Financial Turbulence, and Risk Management paper. Timely Portfolio did a great series of posts about Financial Turbulence:

As example, I will compute Financial Turbulence for the equal weight index of G10 Currencies.

I created a helper function get.G10() function in data.r at github to download historical data for G10 Currencies from FRED.

Let’s compute Financial Turbulence Index for G10 Currencies.

#*****************************************************************

# Load historical data

#*****************************************************************

library(SIT)

load.packages('quantmod')

fx = get.G10()

nperiods = nrow(fx)

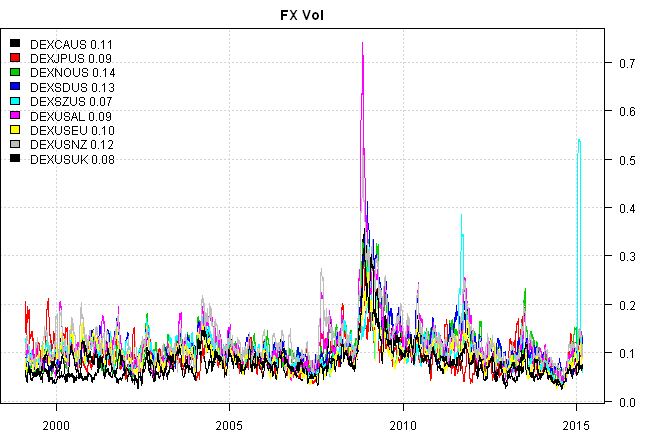

# Check data, plot FX vols

ret = diff(log(fx))

hist.vol = sqrt(252) * bt.apply.matrix(ret, runSD, n = 20)

plota.matplot(hist.vol,main='FX Vol')

Swiss currency, DEXSZUS - Switzerland/U.S., dropeed 13% in a single day due to removal of trading restrictions.

#*****************************************************************

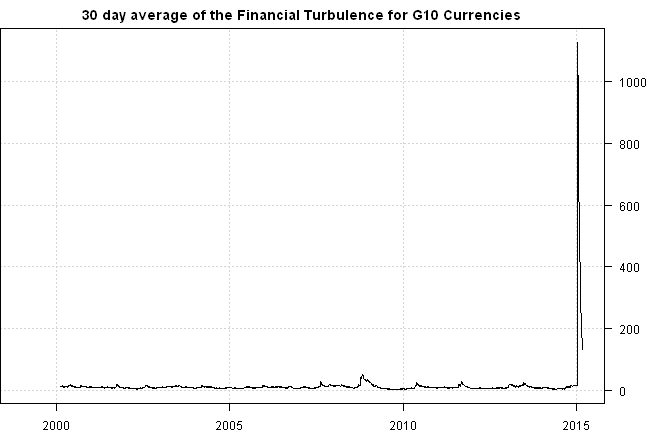

# Rolling estimate of the Financial Turbulence for G10 Currencies

#******************************************************************

turbulence = fx[,1] * NA

colnames(turbulence) = 'turbulence'

ret = coredata(fx / mlag(fx) - 1)

look.back = 252

for( i in (look.back+1) : nperiods ) {

temp = ret[(i - look.back + 1):(i-1), ]

# measures turbulence for the current observation

turbulence[i] = mahalanobis(ret[i,], colMeans(temp), cov(temp))

}

# DEXSZUS - Switzerland/U.S.

print(to.nice(cbind(fx,turbulence)['2015-01-14::2015-01-16',]))| DEXCAUS | DEXJPUS | DEXNOUS | DEXSDUS | DEXSZUS | DEXUSAL | DEXUSEU | DEXUSNZ | DEXUSUK | turbulence | |

|---|---|---|---|---|---|---|---|---|---|---|

| 2015-01-14 | 1.20 | 116.78 | 7.64 | 8.05 | 1.02 | 1.23 | 0.85 | 1.29 | 0.66 | 23.03 |

| 2015-01-15 | 1.19 | 116.95 | 7.65 | 8.14 | 0.89 | 1.22 | 0.86 | 1.28 | 0.66 | 17,225.61 |

| 2015-01-16 | 1.20 | 117.45 | 7.60 | 8.14 | 0.85 | 1.22 | 0.87 | 1.29 | 0.66 | 47.83 |

#*****************************************************************

# Plot 30 day average of the Financial Turbulence for G10 Currencies

#******************************************************************

plota(EMA( turbulence, 30), type='l',

main='30 day average of the Financial Turbulence for G10 Currencies')

#*****************************************************************

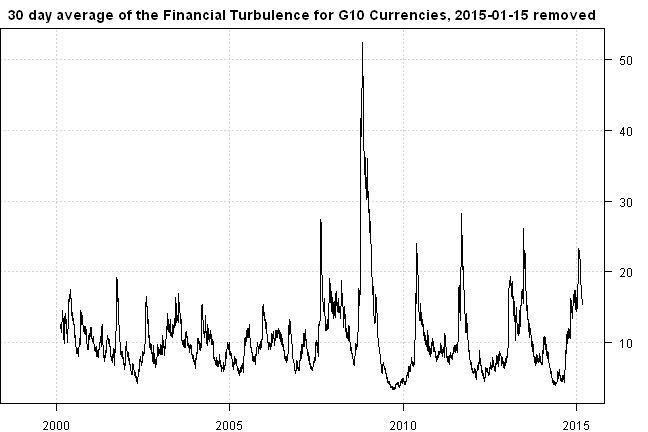

# Same plot with 2015-01-15 removed

#******************************************************************

turbulence['2015-01-15']=NA

plota(EMA( ifna.prev(turbulence), 30), type='l',

main='30 day average of the Financial Turbulence for G10 Currencies, 2015-01-15 removed')

There is a big spike in the index during 2008-2009 period. If you had monitored the Financial Turbulence Index and reduced or hedged your positions during these times, you would be able to reduce your draw-downs and sleep better at night.

To view the complete source code for this example, please have a look at the bt.financial.turbulence.test() function in bt.test.r at github.

(this report was produced on: 2015-03-14)