Filtering Stocks

26 Mar 2015To install Systematic Investor Toolbox (SIT) please visit About page.

I found following discussions interesting and easy to test:

-

NASDAQ 100 Couples by Ripples The similarity measure is based on distance function from TSdist package

Below I will try to adapt a code from the posts:

#*****************************************************************

# Load historical end of day data

#*****************************************************************

library(SIT)

load.packages('quantmod')

tickers = nasdaq.100.components()

tickers = c('SPY', tickers)

data <- new.env()

getSymbols.extra(tickers, src = 'yahoo', from = '1970-01-01', env = data, set.symbolnames = T, auto.assign = T)

for(i in data$symbolnames) data[[i]] = adjustOHLC(data[[i]], use.Adjusted=T)

#print(bt.start.dates(data))

bt.prep(data, align='keep.all', dates='2000::', fill.gaps=T)

# remove ones with little history

bt.prep.remove.symbols.min.history(data, 5*252)

# show the ones removed

print(setdiff(tickers,names(data$prices)))FB GOOG KRFT LVNTA LMCA LMCK NXPI TSLA TRIP

#*****************************************************************

# Compute Distance

#*****************************************************************

tickers = names(data$prices)

prices = data$prices

n = ncol(prices)

prices = last(prices, 5*252)

prices = coredata(prices)

load.packages('TSdist')

# all possible combinations

choices = expand.grid(t1=1:n,t2=1:n,KEEP.OUT.ATTRS=F)

choices = choices[choices$t1 < choices$t2,]

n.choices = nrow(choices)

choices = as.matrix(choices)

#*****************************************************************

# Compute over all combinations

#*****************************************************************

# Following is SLOW, let's use all cores

#result = rep(NA, n.choices)

#for(i in 1:n.choices) {

# result[i] = tsDistances(prices[,choices[i,1]], prices[,choices[i,2]], distance="crosscorrelation")

# if( i %% 100 == 0) cat(i, '\n')

#}

# Run Cluster

load.packages('parallel')

cl = setup.cluster({library(TSdist)}, 'prices,choices',envir=environment())

out = clusterApplyLB(cl, 1:n.choices, function(i) { tsDistances(prices[,choices[i,1]], prices[,choices[i,2]], distance="crosscorrelation") } )

stopCluster(cl)

result = do.call(c, out)

#*****************************************************************

# Plot

#*****************************************************************

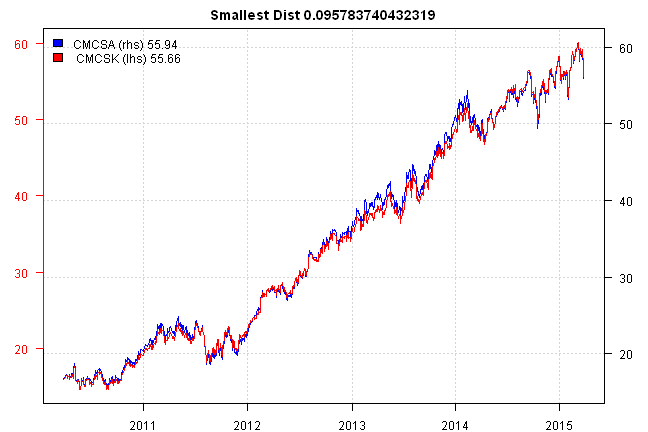

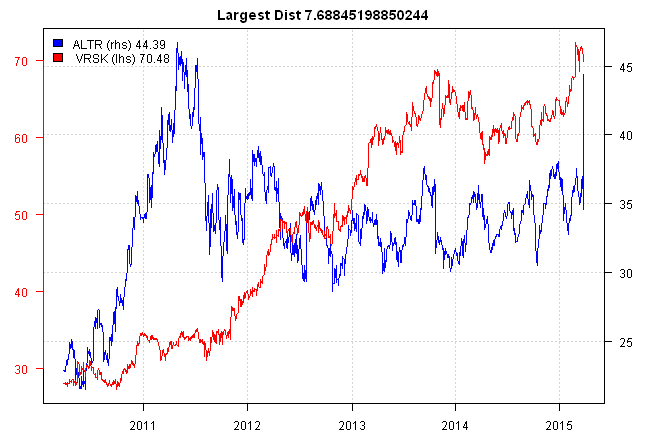

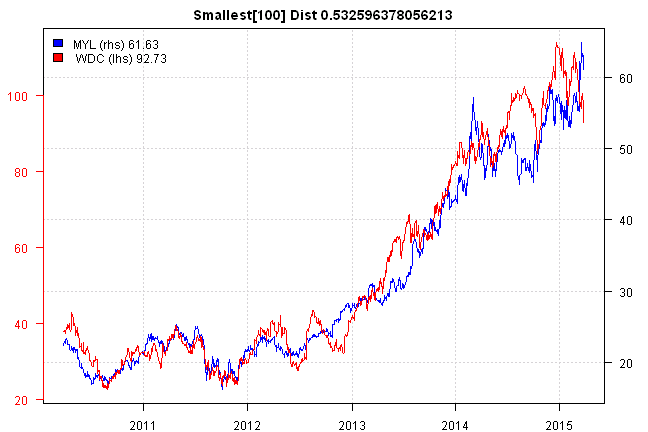

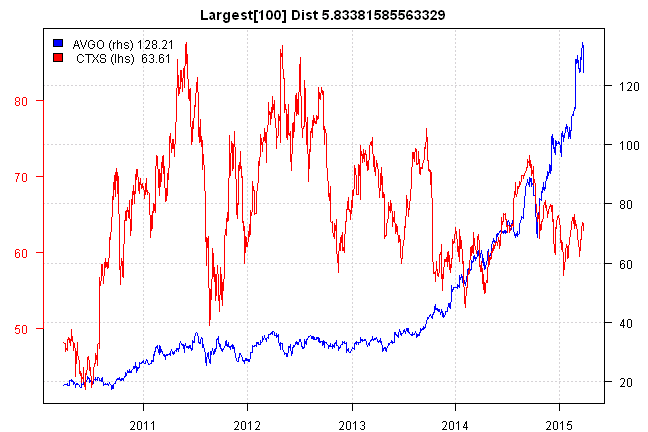

side.by.side.plot = function(index, main=NULL) {

i = choices[index,1]

j = choices[index,2]

plota(prices[,i], type = 'l', LeftMargin=3, col='blue', main=main)

plota2Y(prices[,j], type='l', las=1, col='red', col.axis = 'red')

plota.legend(paste(tickers[i], '(rhs),', tickers[j], '(lhs)'), 'blue,red', list(prices[,i],prices[,j]))

}

prices = last(data$prices, 5*252)

index = sort.list(result)

i = index[1]

side.by.side.plot(i, paste('Smallest Dist', result[i]))

i = last(index)

side.by.side.plot(i, paste('Largest Dist', result[i]))

i = index[100]

side.by.side.plot(i, paste('Smallest[100] Dist', result[i]))

i = last(index,100)[1]

side.by.side.plot(i, paste('Largest[100] Dist', result[i]))

Next let’s look at the second idea: Stocks with upside potential by Eran Raviv

#*****************************************************************

# Compute Qunatile Regressions

#*****************************************************************

prices = data$prices

n = ncol(prices)

rets = prices / mlag(prices) - 1

rets = last(rets, 1 * 252)

rets = coredata(rets)

load.packages('quantreg')

# Ask the slopes for 20% and 80%

tau = c(.2,.8)

result = matrix(1, nr=n, nc=2)

for(i in 2:n) {

result[i,1] = rq(rets[,i] ~ rets[,1], tau = tau[1])$coef[2]

result[i,2] = rq(rets[,i] ~ rets[,1], tau = tau[2])$coef[2]

if( i %% 100 == 0) cat(i, '\n')

}

ratio = result[,2] / result[,1]

#*****************************************************************

# Plot

#*****************************************************************

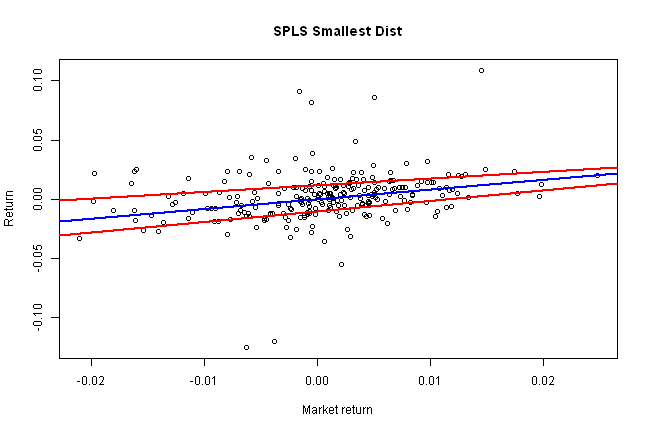

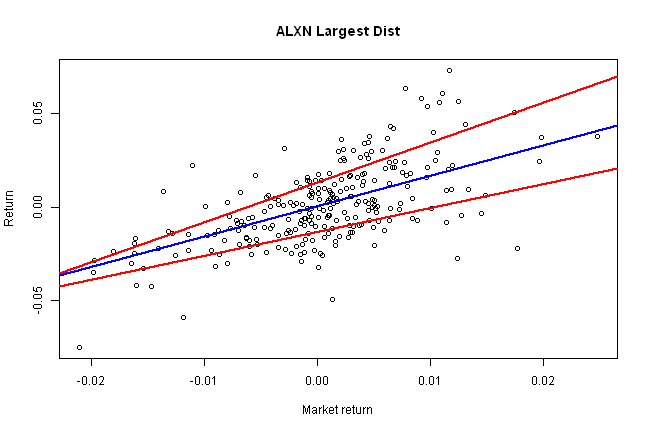

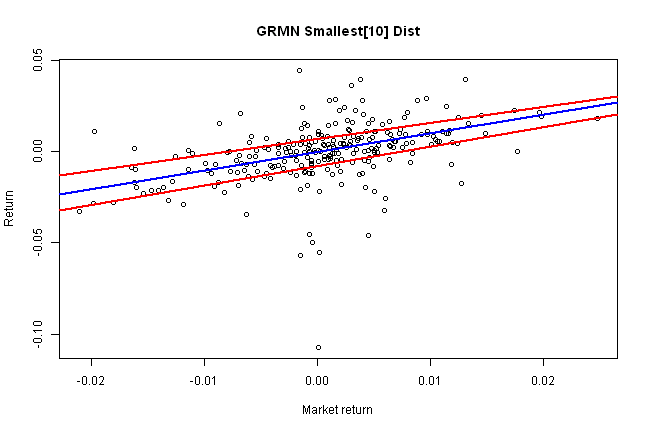

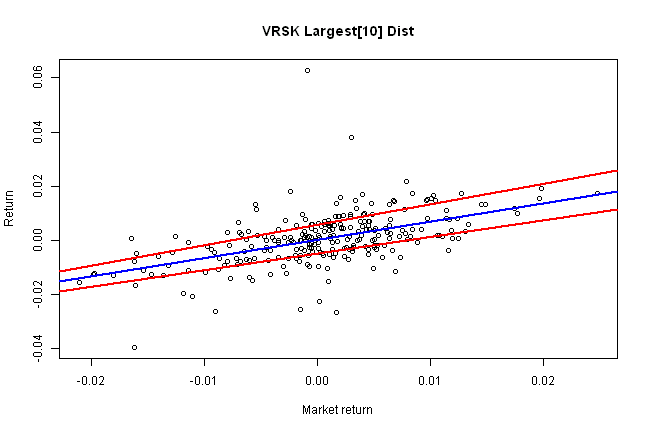

rq.plot = function(i, main='') {

plot(rets[,1], rets[,i], xlab='Market return', ylab='Return', main=paste(tickers[i],main))

abline(reg = rq(rets[,i] ~ rets[,1], tau = tau[1]), col='red', lwd=2)

abline(reg = rq(rets[,i] ~ rets[,1], tau = tau[2]), col='red', lwd=2)

abline(reg = rq(rets[,i] ~ rets[,1], tau = 0.5), col='blue', lwd=2)

}

index = sort.list(ratio)

i = index[1]

rq.plot(i, 'Smallest Dist')

i = last(index)

rq.plot(i,'Largest Dist')

i = index[10]

rq.plot(i,'Smallest[10] Dist')

i = last(index,10)[1]

rq.plot(i,'Largest[10] Dist')

Both concepts work, and show lot’s of promise.

To be continued…

(this report was produced on: 2015-03-29)