Data Proxy - extending time series with proxies

14 Nov 2014To install Systematic Investor Toolbox (SIT) please visit About page.

This page will hold collection of Proxies I collected to extend historical time series.

Note: there are more examples at Composing Synthetic Prices For Extended Historical ETF Data

Commodities:

#*****************************************************************

# Load external data

#******************************************************************

library(SIT)

load.packages('quantmod')

raw.data <- new.env()

# TRJ_CRB file was downloaded from the

# http://www.corecommodityllc.com/CoreIndexes.aspx

# select TR/CC-CRB Index-Total Return and click "See Chart"

# on Chart page click "Download to Spreadsheet" link

# copy TR_CC-CRB, downloaded file, to data folder

temp = extract.table.from.webpage( join(readLines("data/TR_CC-CRB")), 'EODValue' )

temp = join( apply(temp, 1, join, ','), '\n' )

raw.data$CRB = make.stock.xts( read.xts(temp, format='%m/%d/%y' ) )

# prfmdata.csv file was downloaded from the http://www.crbequityindexes.com/indexdata-form.php

# for "TR/J CRB Global Commodity Equity Index", "Total Return", "All Dates"

raw.data$CRB_2 = make.stock.xts( read.xts('data/prfmdata.csv', format='%m/%d/%Y' ) )

#*****************************************************************

# Load historical data

#******************************************************************

load.packages('quantmod')

tickers = spl('GSG,DBC')

data = new.env()

data$CRB = raw.data$CRB

data$CRB_2 = raw.data$CRB_2

getSymbols(tickers, src = 'yahoo', from = '1970-01-01', env = data, auto.assign = T)

for(i in ls(data)) data[[i]] = adjustOHLC(data[[i]], use.Adjusted=T)Look at historical start date for each series:

print(bt.start.dates(data))| Start | |

|---|---|

| CRB | 1994-01-03 |

| CRB_2 | 1999-12-31 |

| DBC | 2006-02-06 |

| GSG | 2006-07-21 |

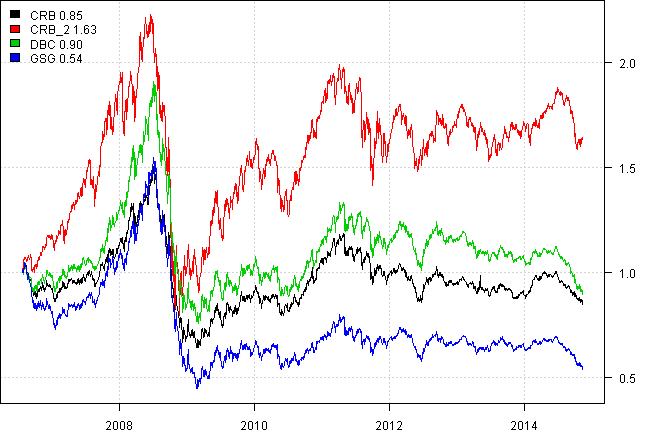

There are 2 sources of historical commodity index data. Let’s compare them with commodity ETFs.

proxy.test(data)

| CRB | CRB_2 | DBC | GSG | |

|---|---|---|---|---|

| CRB | 66% | 89% | 88% | |

| CRB_2 | 66% | 63% | ||

| DBC | 90% | |||

| Mean | -0.1% | 9.5% | 0.9% | -4.4% |

| StDev | 19.1% | 26.6% | 21.0% | 25.0% |

The historical commodity index data from crbequityindexes , that I denoted CRB_2, looks very different over the common interval for all proxies

proxy.overlay.plot(data)

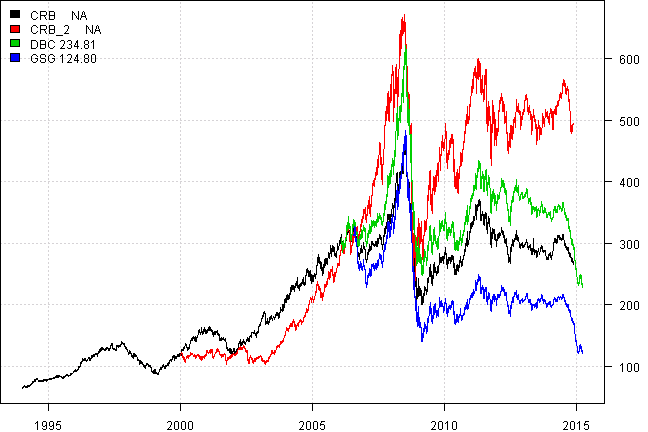

On the all history chart CRB_2 is also different.

proxy.prices(data)

| CRB Price | CRB Total | CRB_2 Price | CRB_2 Total | DBC Price | DBC Total | GSG Price | GSG Total | |

|---|---|---|---|---|---|---|---|---|

| Mean | 8.2% | 8.2% | 11.5% | 11.5% | -0.8% | -0.8% | -7.5% | -7.5% |

| StDev | 16.3% | 16.3% | 21.5% | 21.5% | 20.9% | 20.9% | 25.0% | 25.0% |

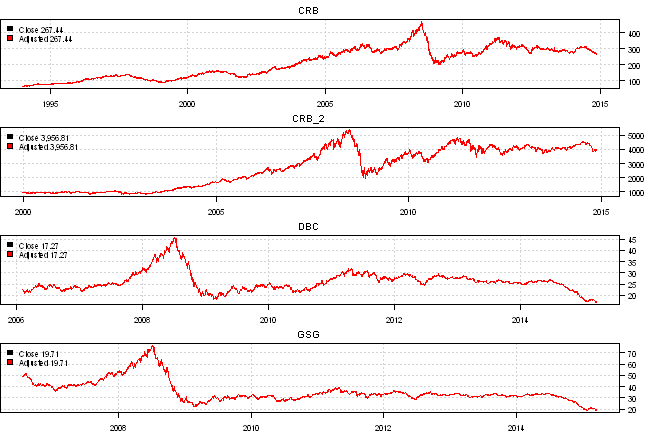

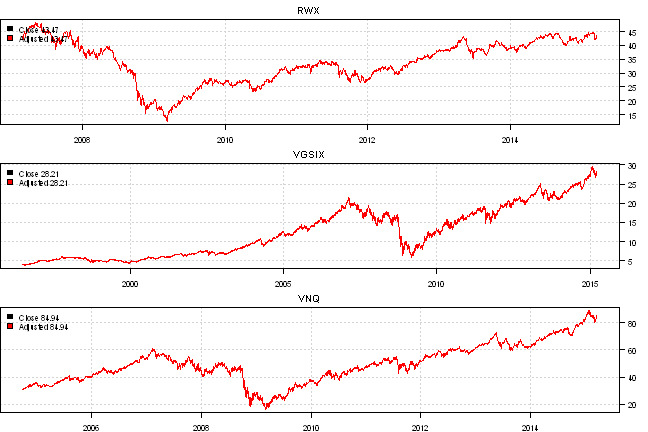

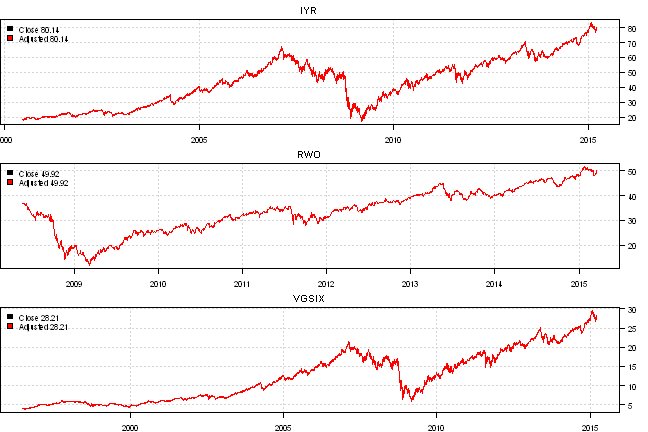

Quick glance at historical time series does not show anything abnormal between Price and Adjusted Price series.

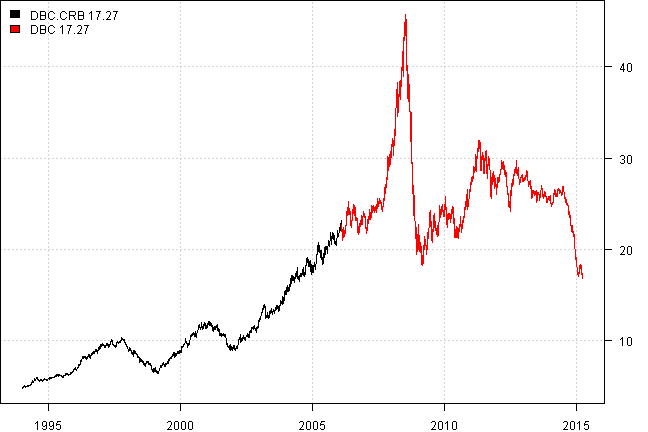

tickers = spl('DBC, DBC.CRB=DBC+CRB')

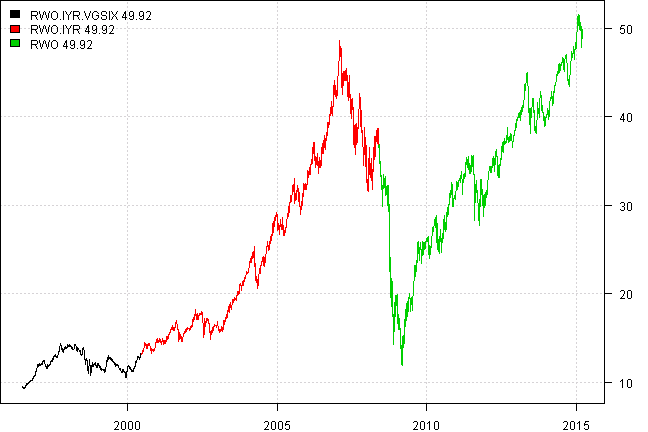

proxy.map(data, tickers)

Please use CRB to extend Commodities.

REIT ex-U.S.:

(Dow Jones Global ex-U.S. Real Estate Securities Index)

create.proxy = function(tickers, proxy.map.tickers, raw.data = new.env()) {

#*****************************************************************

# Load historical data

#******************************************************************

load.packages('quantmod')

tickers = spl(tickers)

data = new.env()

getSymbols.extra(tickers, src = 'yahoo', from = '1970-01-01', env = data, raw.data = raw.data, auto.assign = T)

for(i in ls(data)) data[[i]] = adjustOHLC(data[[i]], use.Adjusted=T)

#*****************************************************************

# Compare

#******************************************************************

print(bt.start.dates(data))

proxy.test(data)

proxy.overlay.plot(data)

proxy.prices(data)

tickers = spl(proxy.map.tickers)

proxy.map(data, tickers)

}

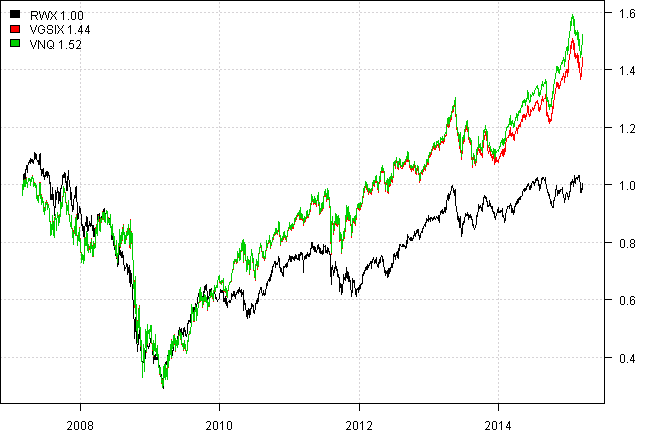

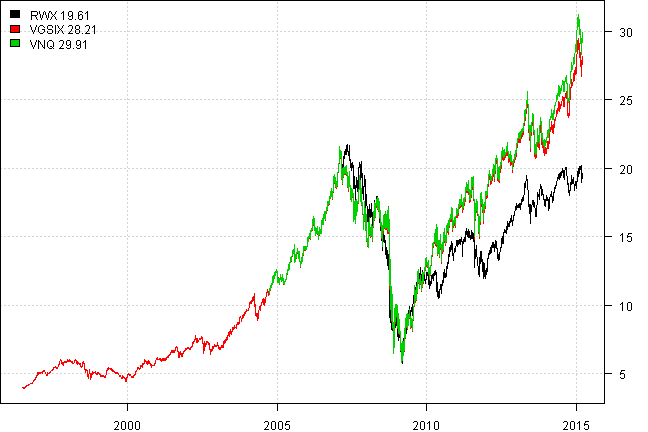

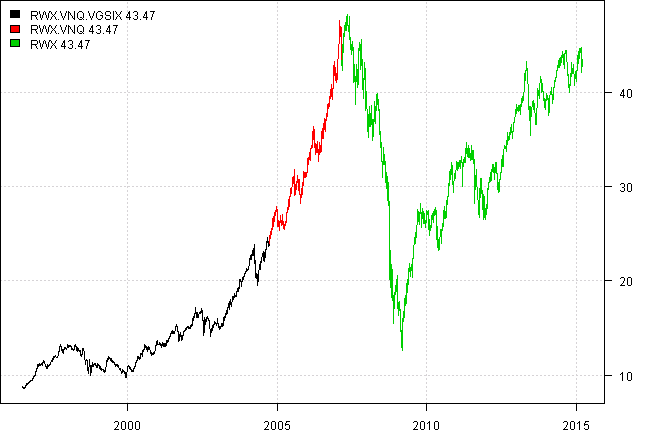

create.proxy('RWX,VNQ,VGSIX', 'RWX, RWX.VNQ=RWX+VNQ, RWX.VNQ.VGSIX=RWX+VNQ+VGSIX')| Start | |

|---|---|

| VGSIX | 1996-06-28 |

| VNQ | 2004-09-29 |

| RWX | 2007-03-02 |

| RWX | VGSIX | VNQ | |

|---|---|---|---|

| RWX | 66% | 67% | |

| VGSIX | 99% | ||

| Mean | 3.3% | 12.6% | 12.9% |

| StDev | 25.4% | 40.2% | 39.1% |

| RWX Price | RWX Total | VGSIX Price | VGSIX Total | VNQ Price | VNQ Total | |

|---|---|---|---|---|---|---|

| Mean | 3.3% | 3.3% | 14.4% | 14.4% | 15.9% | 15.9% |

| StDev | 25.4% | 25.4% | 28.1% | 28.1% | 35.1% | 35.1% |

Please use VNQ and VGSIX to extend REIT ex-U.S.

Aside comparison of RWO vs. RWX: RWO vs. RWX: Head-To-Head ETF Comparison

Global REIT:

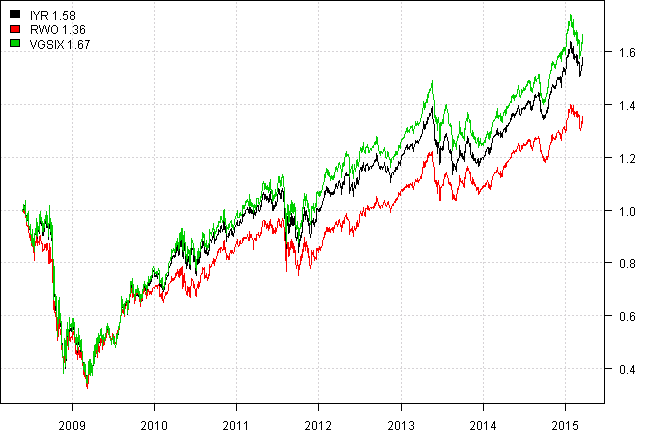

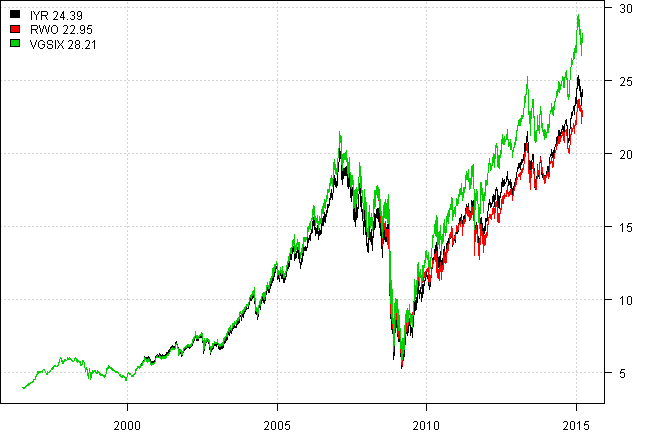

(Dow Jones Global Select Real Estate Securities Index)

Please use IYR and VGSIX to extend Global REIT.

CASH:

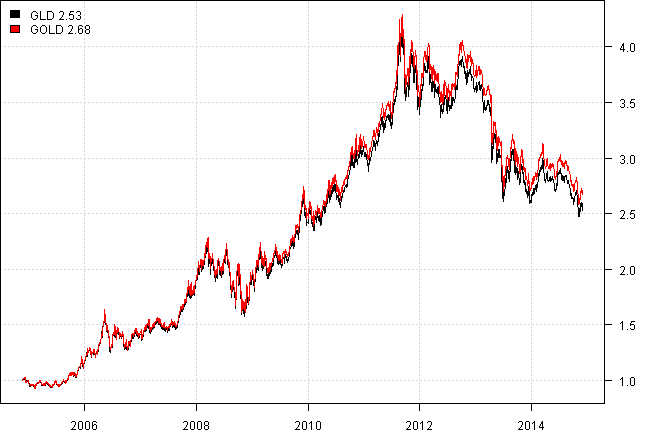

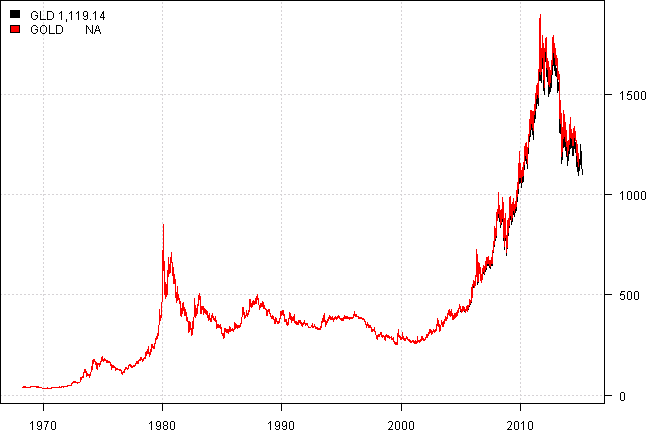

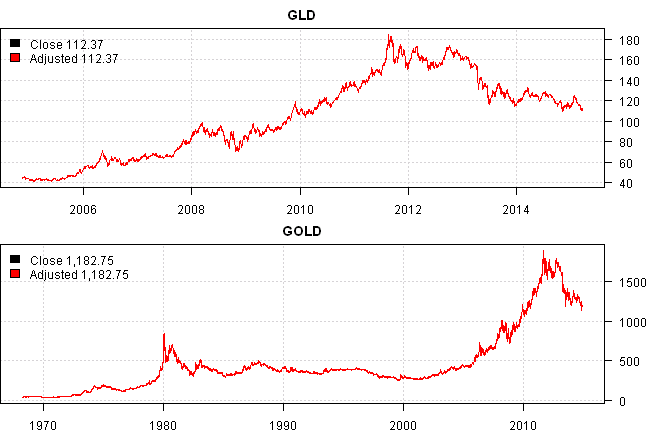

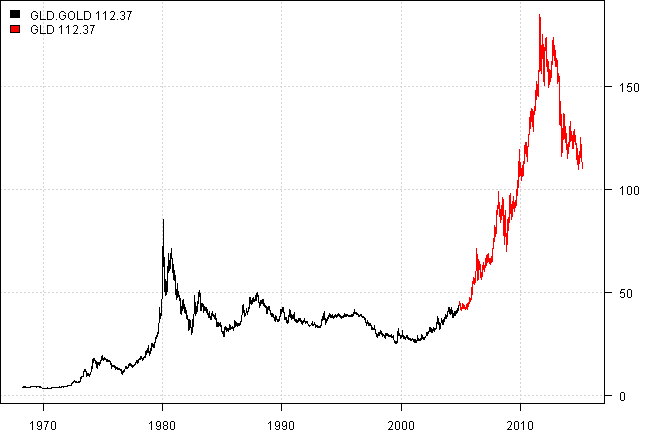

GOLD:

#--------------------------------

# FTSE NAREIT U.S. Real Estate Index monthly total return series

# http://returns.reit.com/returns/MonthlyHistoricalReturns.xls

# https://r-forge.r-project.org/scm/viewvc.php/pkg/FinancialInstrument/inst/parser/download.NAREIT.R?view=markup&root=blotter

filename = 'data/NAREIT.xls'

if(!file.exists(filename)) {

url = 'http://returns.reit.com/returns/MonthlyHistoricalReturns.xls'

download.file(url, filename, mode = 'wb')

}

load.packages('gdata')

temp = read.xls(filename, pattern='Date', sheet='Index Data', stringsAsFactors=FALSE)

index = as.numeric(gsub(',','',temp$Index))

# monthly data, with 1-month-year format

NAREIT = make.xts(index, as.Date(paste(1,temp$Date),'%d %b-%y'))

raw.data$NAREIT = make.stock.xts(NAREIT)

#--------------------------------Let’s save these proxies in data.proxy.Rdata for convience to use later on

Syntax to specify tickers in getSymbols.extra function:

- Basic : XLY

- Rename: BOND=TLT

- Extend: XLB+RYBIX

- Mix above: XLB=XLB+RYBIX+FSDPX+FSCHX+PRNEX+DREVX

- TLT;MTM + IEF => TLT = TLT + IEF and MTM = MTM + IEF

- BOND = TLT;MTM + IEF => BOND = TLT + IEF, TLT = TLT + IEF, and MTM = MTM + IEF

- BOND;US.BOND = TLT;MTM + IEF => BOND = TLT + IEF, US.BOND = TLT + IEF, TLT = TLT + IEF, and MTM = MTM + IEF

-

BOND = [TLT] + IEF => BOND = TLT + IEF, and TLT = TLT + IEF

- use comma or new line to separate entries

- lines starting with

#symbol or empty lines are skipped Make sure not to use commas in comments

,message=T, warning=T

tickers = '

COM = DBC;GSG + CRB

RExUS = [RWX] + VNQ + VGSIX

RE = [RWX] + VNQ + VGSIX

RE.US = [ICF] + VGSIX

EMER.EQ = [EEM] + VEIEX

EMER.FI = [EMB] + PREMX

GOLD = [GLD] + GOLD,

US.CASH = [BIL] + TB3M,

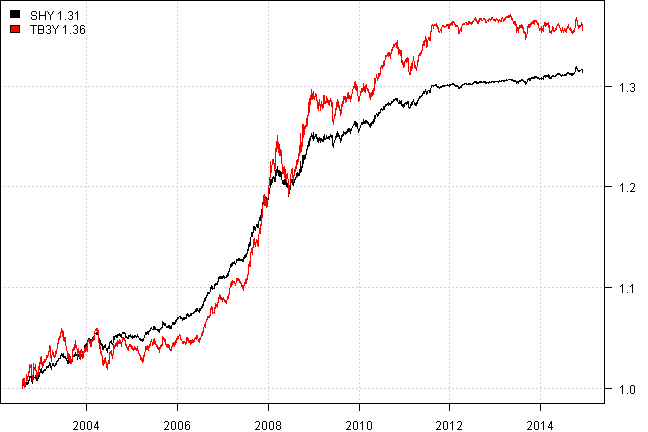

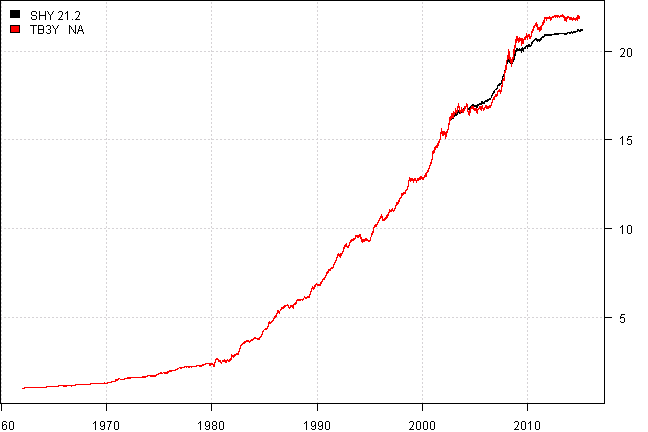

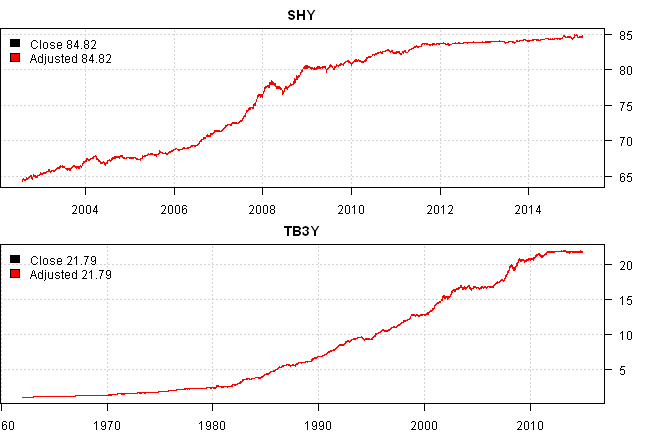

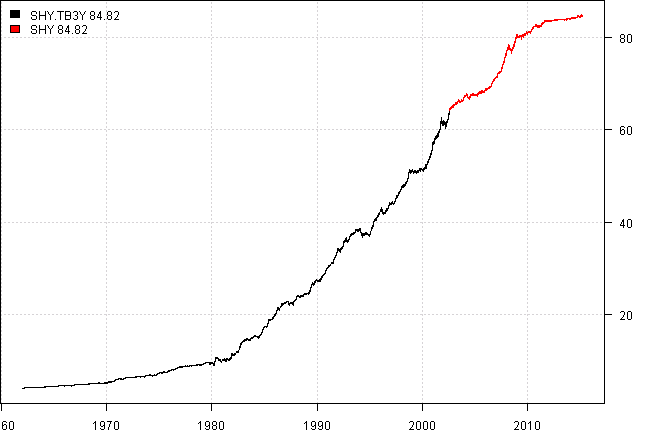

SHY + TB3Y,

US.HY = [HYG] + VWEHX

# Bonds

US.BOND = [AGG] + VBMFX

INTL.BOND = [BWX] + BEGBX

JAPAN.EQ = [EWJ] + FJPNX

EUROPE.EQ = [IEV] + FIEUX

US.SMCAP = IWM;VB + NAESX

TECH.EQ = [QQQ] + ^NDX

US.EQ = [VTI] + VTSMX + VFINX

US.MID = [VO] + VIMSX

EAFE = [EFA] + VDMIX + VGTSX

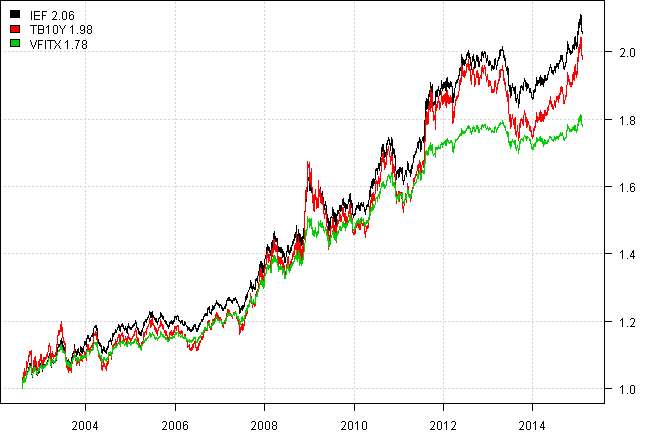

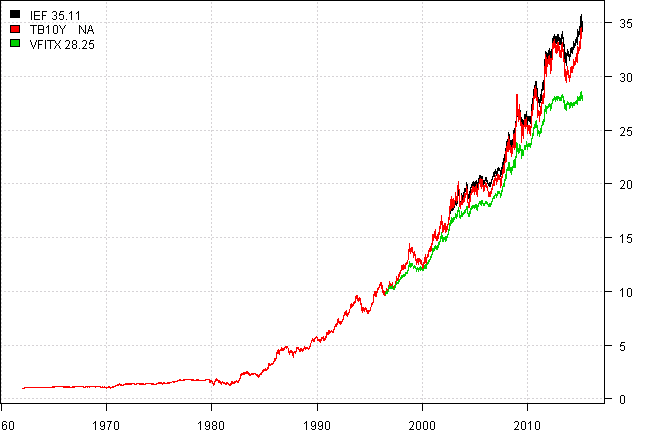

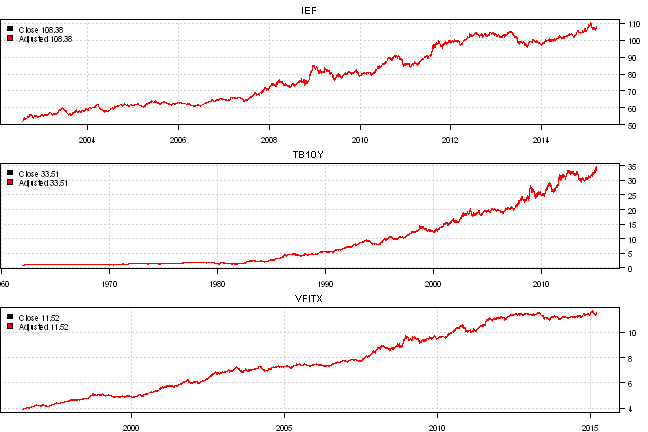

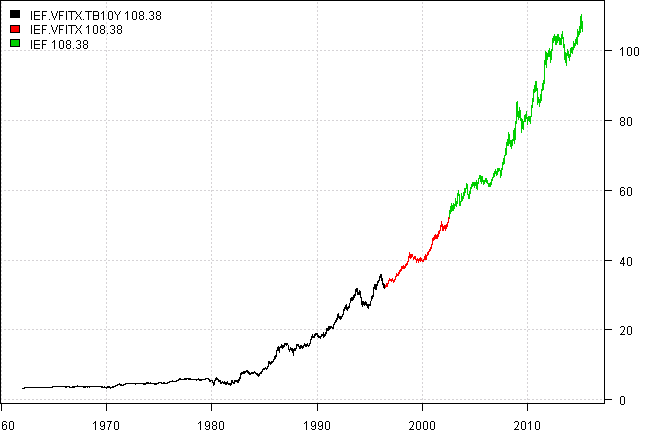

MID.TR = [IEF] + VFITX

CORP.FI = [LQD] + VWESX

TIPS = [TIP] + VIPSX + LSGSX

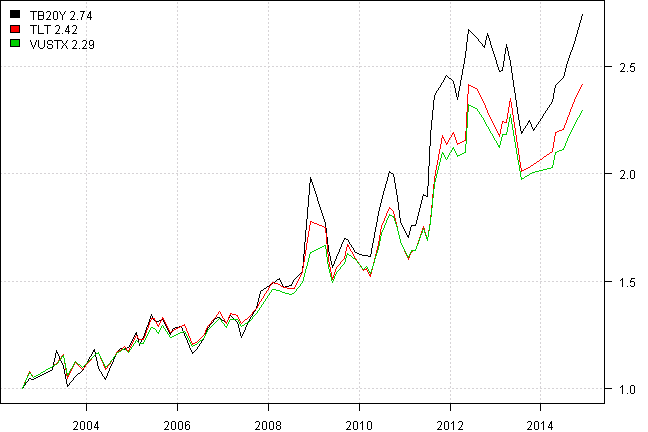

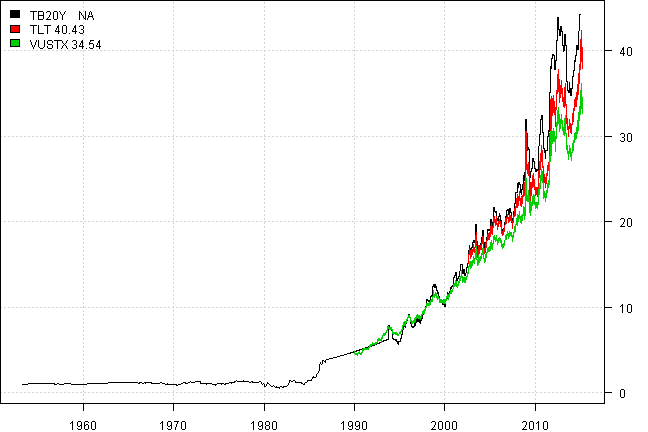

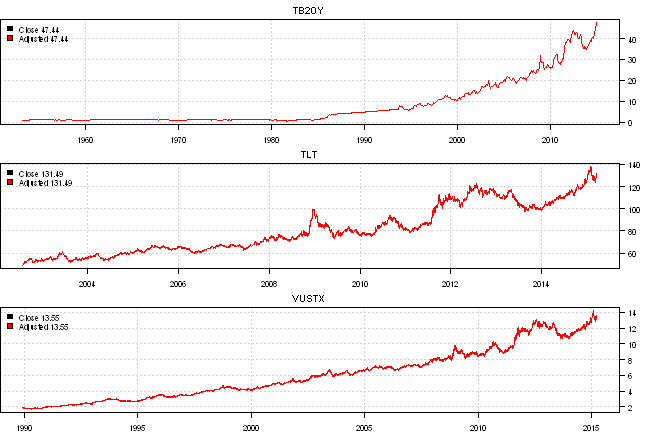

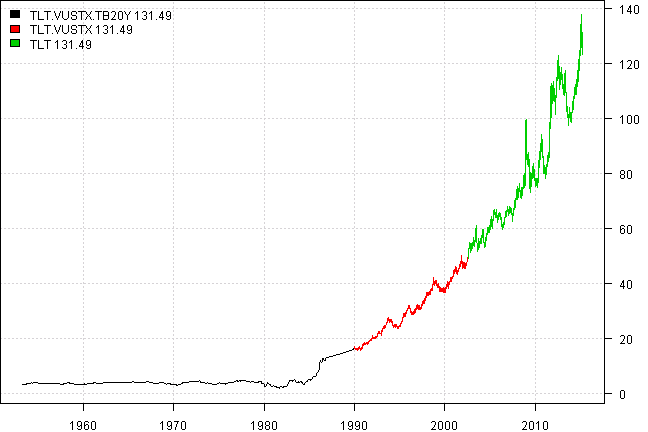

LONG.TR = [TLT] + VUSTX

'

data.proxy <- new.env()

getSymbols.extra(tickers, src = 'yahoo', from = '1970-01-01', env = data.proxy, raw.data = raw.data, auto.assign = T)

data.proxy.raw = raw.data

save(data.proxy.raw, file='data/data.proxy.raw.Rdata',compress='gzip')

save(data.proxy, file='data/data.proxy.Rdata',compress='gzip') To use saved proxy data to extend historical time series, use extend.data.proxy function:

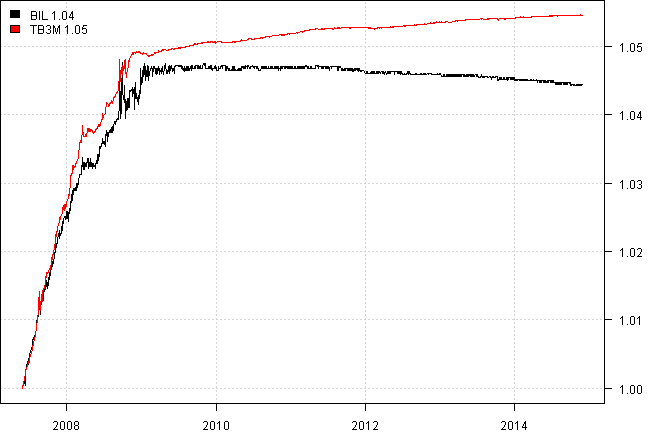

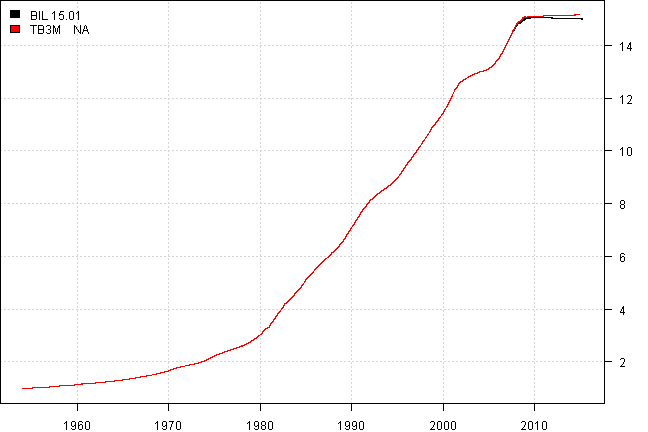

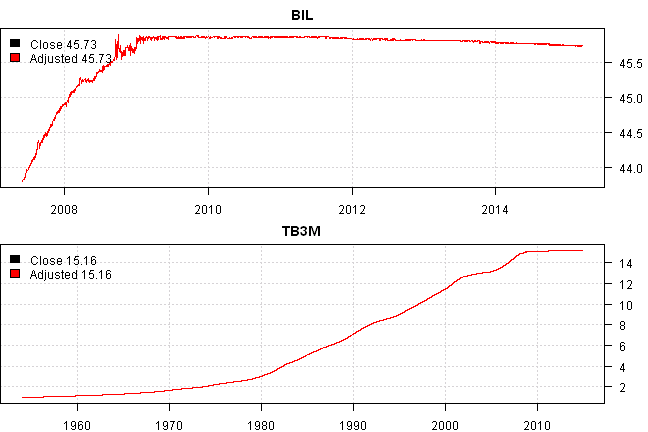

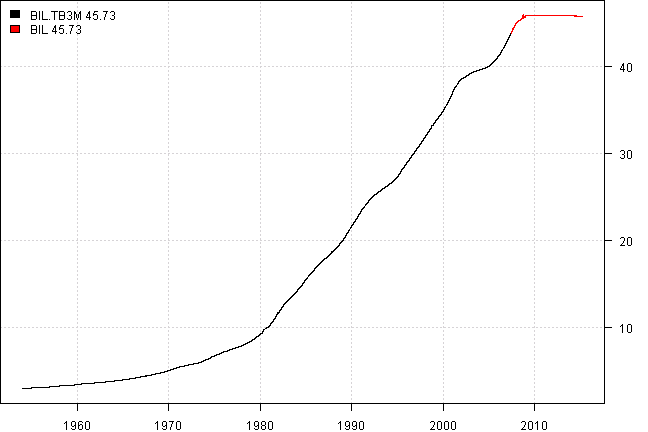

tickers = spl('BIL')

data <- new.env()

getSymbols(tickers, src = 'yahoo', from = '1970-01-01', env = data, auto.assign = T)

print(bt.start.dates(data))| Start | |

|---|---|

| BIL | 2007-05-30 |

extend.data.proxy(data, proxy.filename = 'data/data.proxy.Rdata')

print(bt.start.dates(data))| Start | |

|---|---|

| BIL | 1954-01-04 |

(this report was produced on: 2015-03-19)