Adjusted Data

30 Mar 2015To install Systematic Investor Toolbox (SIT) please visit About page.

Date at DTR Trading wrote an excellent series on cons / pros of using Adjusted data for momentum strategies.

Below I will try to adapt a code from the posts:

#*****************************************************************

# Load historical end of day data

#*****************************************************************

library(SIT)

load.packages('quantmod')

tickers = '

AGG # iShares Barclays Aggregate Bond Fund

DBC # PowerShares DB Com Indx Trckng Fund

EEM # iShares MSCI Emerging Markets Indx

EFA # iShares MSCI EAFE Index Fund

GLD # SPDR Gold Trust

IYR # iShares Dow Jones US Real Estate

JNK # SPDR Barclays Capital High Yield Bond

PPH # Market Vectors Pharmaceutical

SPY # SPDR S&P 500 Trust

TIP # iShares Barclays TIPS Bond Fund

'

tickers = '

EEM # iShares MSCI Emerging Markets Index ETF

EFA # iShares MSCI EAFE Index ETF

FXI # iShares China Large#Cap ETF

IEF # iShares 7#10 Year Treasury Bond ETF

IYR # iShares Dow Jones US Real Estate ETF

SHY # iShares 1#3 Year Treasury Bond ETF

SPY # SPDR S&P 500 Trust ETF

TIP # iShares Barclays TIPS Bond ETF

XLV # Health Care Select Sector SPDR ETF

UUP # PowerShares DB US Dollar Bullish ETF

'

data = new.env()

getSymbols.extra(tickers, src = 'yahoo', from = '1970-01-01', env = data, set.symbolnames = T, auto.assign = T)

#print(bt.start.dates(data))

#*****************************************************************

# Contruct another back-test environment with split-adjusted prices, do not include dividends

# http://www.fintools.com/wp-content/uploads/2012/02/DividendAdjustedStockPrices.pdf

# http://www.pstat.ucsb.edu/research/papers/momentum.pdf

#

# For example of split and dividend schedule

# http://finance.yahoo.com/q/hp?s=EFA&g=v

#*****************************************************************

data.price = new.env()

data.price$symbolnames = data$symbolnames

for(i in data$symbolnames) data.price[[i]] = adjustOHLC(data[[i]], symbol.name=i, adjust='split', use.Adjusted=F)

bt.prep(data.price, align='keep.all', dates='2002::', fill.gaps=T)

#*****************************************************************

# Adjust prices

#*****************************************************************

for(i in data$symbolnames) data[[i]] = adjustOHLC(data[[i]], use.Adjusted=T)

bt.prep(data, align='keep.all', dates='2002::', fill.gaps=T)We constructed two environments:

- data environment contains split and dividend adjusted prices

- data.price environment contains only split adjusted prices

#*****************************************************************

# Setup

#*****************************************************************

prices = data$prices

n = ncol(prices)

nperiods = nrow(prices)

frequency = 'months'

period.ends = endpoints(prices, frequency)

period.ends1 = period.ends - 1 # lag by one day

period.ends1 = period.ends1[period.ends1 > 0]

period.ends0 = period.ends1 + 1

models = list()

commission = list(cps = 0.01, fixed = 10.0, percentage = 0.0)

#*****************************************************************

# 60 day rate of change for ranking

#******************************************************************

return = prices / mlag(prices,60) - 1

position.score = iif(return < 0, NA, return)

data$weight[] = NA

data$weight[period.ends0,] = ntop(position.score[period.ends1,], 1)

models$mom60 = bt.run.share(data, clean.signal=F, commission = commission, trade.summary=T, silent=T)

# alternatively use do.lag

#data$weight[] = NA

# data$weight[period.ends1,] = ntop(position.score[period.ends1,], 1)

#models$mom60A = bt.run.share(data, clean.signal=F, do.lag=2, commission = commission, trade.summary=T, silent=T)

#print(last.trades(models$mom60, make.plot=F, return.table=T))

#print(last.trades(models$mom60A, make.plot=F, return.table=T))

#*****************************************************************

# 60/120 day rate of change for ranking

#******************************************************************

return = prices / mlag(prices,60) - 1 + prices / mlag(prices,120) - 1

position.score = iif(return < 0, NA, return)

data$weight[] = NA

data$weight[period.ends0,] = ntop(position.score[period.ends1,], 1)

models$mom120 = bt.run.share(data, clean.signal=F, commission = commission, trade.summary=T, silent=T)

#*****************************************************************

# Create Report

#*****************************************************************

#strategy.performance.snapshoot(models, T)

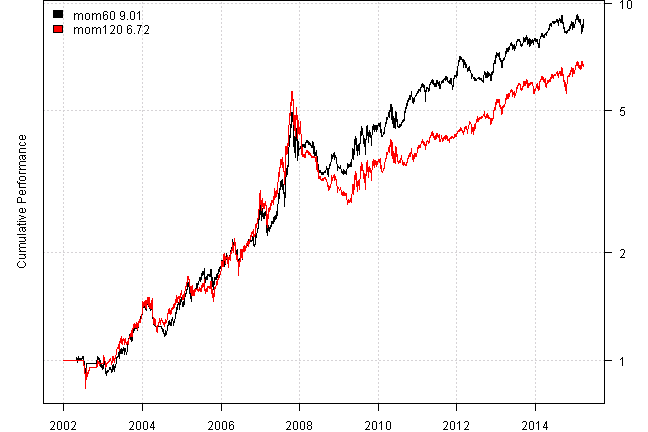

plotbt(models, plotX = T, log = 'y', LeftMargin = 3, main = NULL)

mtext('Cumulative Performance', side = 2, line = 1)

print(plotbt.strategy.sidebyside(models, make.plot=F, return.table=T, perfromance.fn=engineering.returns.kpi))| mom60 | mom120 | |

|---|---|---|

| Period | Jan2002 - Mar2015 | Jan2002 - Mar2015 |

| Cagr | 18.05 | 15.47 |

| Sharpe | 0.89 | 0.76 |

| DVR | 0.85 | 0.7 |

| R2 | 0.95 | 0.92 |

| Volatility | 21.26 | 22.21 |

| MaxDD | -33.49 | -51.75 |

| Exposure | 94.36 | 94.36 |

| Win.Percent | 63.76 | 62.42 |

| Avg.Trade | 1.69 | 1.49 |

| Profit.Factor | 2.24 | 2 |

| Num.Trades | 149 | 149 |

print(last.trades(models$mom60, make.plot=F, return.table=T))| models$mom60 | weight | entry.date | exit.date | nhold | entry.price | exit.price | return |

|---|---|---|---|---|---|---|---|

| SPY | 100 | 2013-06-28 | 2013-07-31 | 33 | 155.04 | 163.06 | 5.17 |

| XLV | 100 | 2013-07-31 | 2013-08-30 | 30 | 49.88 | 48.12 | -3.53 |

| XLV | 100 | 2013-08-30 | 2013-09-30 | 31 | 48.12 | 49.66 | 3.20 |

| FXI | 100 | 2013-09-30 | 2013-10-31 | 31 | 35.92 | 36.40 | 1.34 |

| EEM | 100 | 2013-10-31 | 2013-11-29 | 29 | 41.16 | 41.05 | -0.27 |

| XLV | 100 | 2013-11-29 | 2013-12-31 | 32 | 54.24 | 54.64 | 0.75 |

| SPY | 100 | 2013-12-31 | 2014-01-31 | 31 | 180.35 | 173.99 | -3.53 |

| XLV | 100 | 2014-01-31 | 2014-02-28 | 28 | 55.16 | 58.59 | 6.22 |

| IYR | 100 | 2014-02-28 | 2014-03-31 | 31 | 65.72 | 65.81 | 0.14 |

| IYR | 100 | 2014-03-31 | 2014-04-30 | 30 | 65.81 | 67.81 | 3.04 |

| EEM | 100 | 2014-04-30 | 2014-05-30 | 30 | 40.42 | 41.62 | 2.97 |

| EEM | 100 | 2014-05-30 | 2014-06-30 | 31 | 41.62 | 42.62 | 2.40 |

| IYR | 100 | 2014-06-30 | 2014-07-31 | 31 | 70.41 | 70.33 | -0.11 |

| FXI | 100 | 2014-07-31 | 2014-09-30 | 61 | 39.96 | 37.80 | -5.41 |

| UUP | 100 | 2014-09-30 | 2014-10-31 | 31 | 22.87 | 23.09 | 0.96 |

| XLV | 100 | 2014-10-31 | 2014-11-28 | 28 | 67.02 | 69.35 | 3.48 |

| XLV | 100 | 2014-11-28 | 2014-12-31 | 33 | 69.35 | 68.38 | -1.40 |

| IYR | 100 | 2014-12-31 | 2015-01-30 | 30 | 76.84 | 81.23 | 5.71 |

| IYR | 100 | 2015-01-30 | 2015-02-27 | 28 | 81.23 | 79.12 | -2.60 |

| FXI | 100 | 2015-02-27 | 2015-03-30 | 31 | 43.76 | 44.74 | 2.24 |

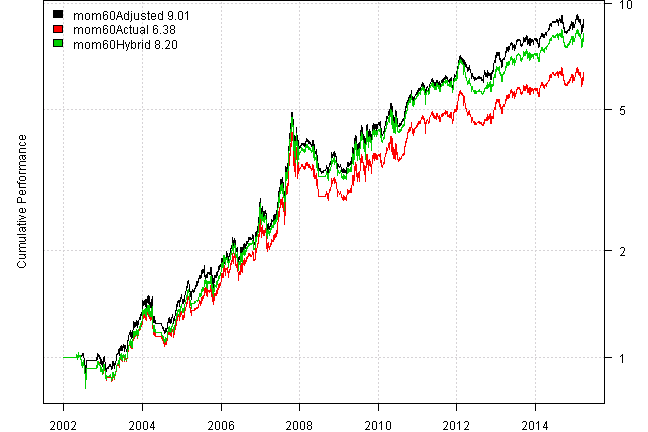

Next let’s consider following 3 setups:

- “Adjusted” - split and dividend adjusted price data. The signals and P&L are derived only from the adjusted data time series.

- “Actual” - using only split adjusted data, that has not been adjusted for dividends. The signals and P&L are derived only from the only split adjusted data time series.

- “Hybrid” - use “Actual” time series for signal generation and the “Adjusted” time series for the P&L calculation.

#*****************************************************************

# Helper function

#******************************************************************

run.strategy = function(prices , data, name) {

models = list()

return = prices / mlag(prices,60) - 1

position.score = iif(return < 0, NA, return)

data$weight[] = NA

data$weight[period.ends0,] = ntop(position.score[period.ends1,], 1)

models[[paste0('mom60',name)]] = bt.run.share(data, clean.signal=F, commission = commission, trade.summary=T, silent=T)

return = prices / mlag(prices,60) - 1 + prices / mlag(prices,120) - 1

position.score = iif(return < 0, NA, return)

data$weight[] = NA

data$weight[period.ends0,] = ntop(position.score[period.ends1,], 1)

models[[paste0('mom120',name)]] = bt.run.share(data, clean.signal=F, commission = commission, trade.summary=T, silent=T)

models

}

#*****************************************************************

# Setup

#******************************************************************

prices.adj = data$prices

prices.split = data.price$prices

all.models = list()

all.models = c(all.models, run.strategy(prices.adj, data, 'Adjusted'))

all.models = c(all.models, run.strategy(prices.split, data.price, 'Actual'))

all.models = c(all.models, run.strategy(prices.split, data, 'Hybrid'))

#*****************************************************************

# Create Report

#*****************************************************************

models = all.models[grep('mom60', names(all.models))]

plotbt(models, plotX = T, log = 'y', LeftMargin = 3, main = NULL)

mtext('Cumulative Performance', side = 2, line = 1)

print(plotbt.strategy.sidebyside(models, make.plot=F, return.table=T, perfromance.fn=engineering.returns.kpi))| mom60Adjusted | mom60Actual | mom60Hybrid | |

|---|---|---|---|

| Period | Jan2002 - Mar2015 | Jan2002 - Mar2015 | Jan2002 - Mar2015 |

| Cagr | 18.05 | 15.02 | 17.22 |

| Sharpe | 0.89 | 0.76 | 0.85 |

| DVR | 0.85 | 0.73 | 0.82 |

| R2 | 0.95 | 0.96 | 0.96 |

| Volatility | 21.26 | 21.33 | 21.33 |

| MaxDD | -33.49 | -35.99 | -33.74 |

| Exposure | 94.36 | 92.44 | 92.44 |

| Win.Percent | 63.76 | 62.33 | 63.01 |

| Avg.Trade | 1.69 | 1.49 | 1.67 |

| Profit.Factor | 2.24 | 1.98 | 2.15 |

| Num.Trades | 149 | 146 | 146 |

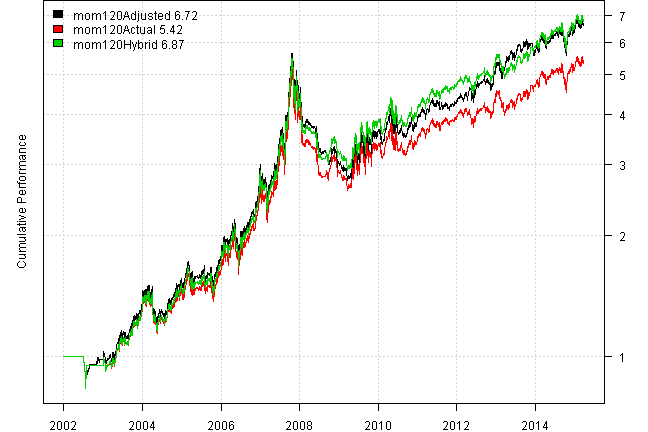

models = all.models[grep('mom120', names(all.models))]

plotbt(models, plotX = T, log = 'y', LeftMargin = 3, main = NULL)

mtext('Cumulative Performance', side = 2, line = 1)

print(plotbt.strategy.sidebyside(models, make.plot=F, return.table=T, perfromance.fn=engineering.returns.kpi))| mom120Adjusted | mom120Actual | mom120Hybrid | |

|---|---|---|---|

| Period | Jan2002 - Mar2015 | Jan2002 - Mar2015 | Jan2002 - Mar2015 |

| Cagr | 15.47 | 13.61 | 15.66 |

| Sharpe | 0.76 | 0.69 | 0.77 |

| DVR | 0.7 | 0.64 | 0.73 |

| R2 | 0.92 | 0.92 | 0.94 |

| Volatility | 22.21 | 22.08 | 22.07 |

| MaxDD | -51.75 | -49.93 | -47.15 |

| Exposure | 94.36 | 92.47 | 92.47 |

| Win.Percent | 62.42 | 60.96 | 61.64 |

| Avg.Trade | 1.49 | 1.37 | 1.54 |

| Profit.Factor | 2 | 1.9 | 2.02 |

| Num.Trades | 149 | 146 | 146 |

In agreement with source Adjusted and Hybrid outperform Actual.

(this report was produced on: 2015-03-31)