Elastic Asset Allocation Strategy

To install Systematic Investor Toolbox (SIT) please visit About page.

The Elastic Asset Allocation Strategy(EAA) backtest and live signal. For more details please see SSRN paper

The EAA Strategy uses a geometrical weighted average of the historical returns, volatilities and correlations, using elasticities as weights:

asset’s attractivness = [return ^ wR] * [(1-correlation) ^ wC] / [volatility ^ wV]

where:

- return is average asset’s return over last year using different timeframes

- correlation is asset’s correlation with equal weight, market, index

- volatility is asset’s historical volatility

- wR, wC, wV are user elasticities

Load historical data from Yahoo Finance:

#*****************************************************************

# Load historical data

#*****************************************************************

library(SIT)

load.packages('quantmod')

tickers = '

US.STOCKS = VTI + VTSMX

FOREIGN.STOCKS = VEU + FDIVX

EMERGING.MARKETS=EEM + VEIEX

US.10YR.GOV.BOND = IEF + VFITX

REAL.ESTATE = VNQ + VGSIX

COMMODITIES = DBC + CRB

CASH = BND + VBMFX

'

# load saved Proxies Raw Data, data.proxy.raw

load('data.proxy.raw.Rdata')

data <- new.env()

getSymbols.extra(tickers, src = 'yahoo', from = '1970-01-01', env = data, raw.data = data.proxy.raw, auto.assign = T, set.symbolnames = T, getSymbols.fn = getSymbols.fn, calendar=calendar)

for(i in data$symbolnames) data[[i]] = adjustOHLC(data[[i]], use.Adjusted=T)

bt.prep(data, align='remove.na', dates='::')

print(last(data$prices))| US.STOCKS | FOREIGN.STOCKS | EMERGING.MARKETS | US.10YR.GOV.BOND | REAL.ESTATE | COMMODITIES | CASH | |

|---|---|---|---|---|---|---|---|

| 2016-06-24 | 104.05 | 41.22 | 32.65 | 112.21 | 84.86 | 15.01 | 83.7 |

#*****************************************************************

# Setup

#*****************************************************************

data$universe = data$prices > 0

# do not allocate to CASH

data$universe$CASH = NA

prices = data$prices * data$universe

n = ncol(prices)Code Strategy Rules:

#*****************************************************************

# Code Strategy

#******************************************************************

ret = diff(log(prices))

n.top = 3

mom.lookback = 80

vol.lookback = 12*22

cor.lookback = 12*22

weight=list(r=1, v=0, c=0.5, s=2)

hist.vol = sqrt(252) * bt.apply.matrix(ret, runSD, n = vol.lookback)

#mean of cumulative returns of 1, 3, 6, and 12 month periods

mom = (prices / mlag(prices, 22)-1 + prices / mlag(prices, 3*22)-1

+ prices / mlag(prices, 6*22)-1 + prices / mlag(prices, 12 * 22)-1)/22

mkt.ret = rowMeans(ret, na.rm=T)

#*****************************************************************

# Compute Correlation to Market

#******************************************************************

mkt.cor = data$weight * NA

for(i in period.ends[period.ends > cor.lookback]){

index = (i - cor.lookback):i

hist = ret[index,]

include.index = !is.na(colSums(hist))

if(any(include.index))

mkt.cor[i,include.index] = cor(hist[,include.index], mkt.ret[index], use='complete.obs',method='pearson')

}

avg.rank = (mom^weight$r * (1 - mkt.cor)^weight$c / hist.vol^weight$v) ^ weight$s

meta.rank = br.rank(avg.rank[period.ends,])

#absolute momentum filter

weight = (meta.rank <= n.top)/rowSums(meta.rank <= n.top, na.rm=T) * (mom[period.ends,] > 0)

# otherwise, it's weight is allocated to cash

weight$CASH = 1 - rowSums(weight,na.rm=T)

obj$weights$strategy = weight

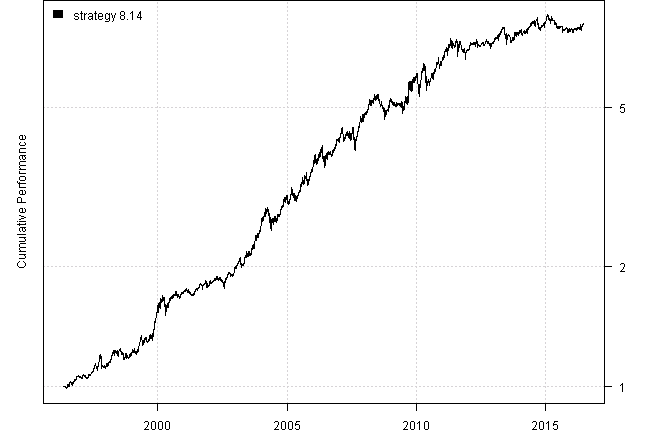

#Strategy Performance:

| strategy | |

|---|---|

| Period | May1996 - Jun2016 |

| Cagr | 10.98 |

| Sharpe | 1.03 |

| DVR | 0.99 |

| R2 | 0.96 |

| Volatility | 10.66 |

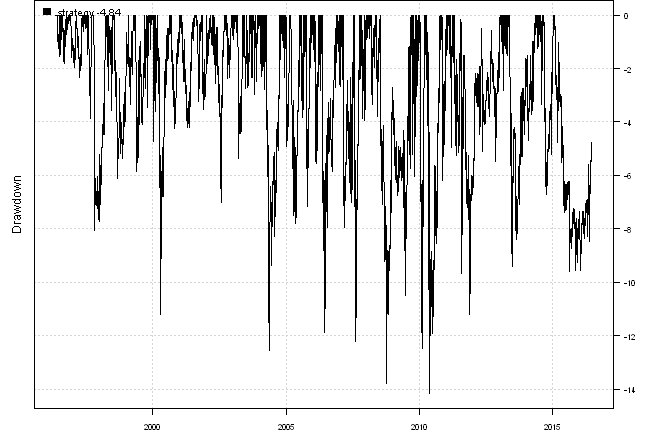

| MaxDD | -14.18 |

| Exposure | 99.72 |

| Win.Percent | 62.77 |

| Avg.Trade | 0.35 |

| Profit.Factor | 2.03 |

| Num.Trades | 658 |

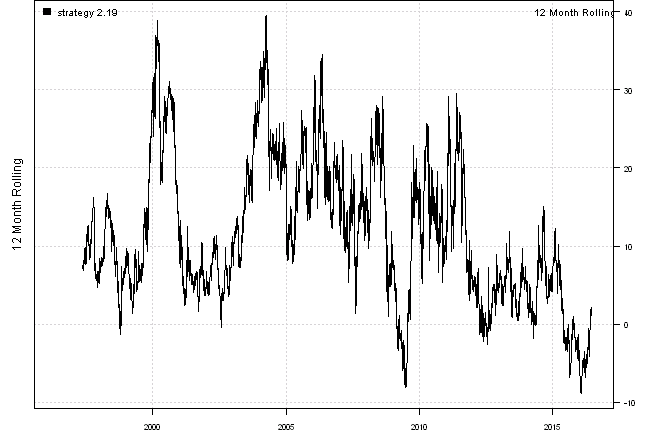

#Monthly Results for strategy :

| Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | Year | MaxDD | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1996 | 1.3 | 0.2 | -0.2 | 1.7 | 2.2 | 1.7 | -0.9 | 6.2 | -1.8 | |||||

| 1997 | 0.2 | 0.1 | -1.0 | 1.5 | 0.9 | 1.0 | 4.5 | -3.5 | 7.3 | -3.9 | -1.0 | 1.6 | 7.4 | -8.1 |

| 1998 | 0.1 | 2.2 | 3.3 | 1.5 | -0.6 | 1.2 | -0.6 | -4.0 | 2.5 | -0.6 | 0.2 | 2.4 | 7.6 | -6.1 |

| 1999 | 1.7 | -2.9 | 1.6 | 6.7 | -3.3 | 3.6 | -1.8 | 1.4 | 1.9 | 1.5 | 7.0 | 10.5 | 30.6 | -5.8 |

| 2000 | -2.1 | 4.8 | -0.2 | -5.0 | 2.6 | 3.5 | 1.0 | 2.4 | -0.9 | -1.5 | 3.0 | 0.9 | 8.3 | -11.2 |

| 2001 | 0.7 | -0.4 | -1.4 | -0.8 | 1.0 | 2.2 | 0.9 | 1.9 | -0.3 | 1.8 | -1.7 | 0.1 | 4.1 | -4.2 |

| 2002 | 1.1 | 1.3 | 0.7 | 0.2 | 0.1 | -1.3 | -0.9 | 2.9 | 2.8 | -0.9 | -0.5 | 4.1 | 10.0 | -7.0 |

| 2003 | 2.5 | 3.0 | -2.8 | -0.4 | 4.6 | 0.5 | 0.6 | 4.3 | 0.4 | 5.3 | 1.1 | 6.8 | 28.7 | -5.4 |

| 2004 | 3.1 | 4.3 | 2.5 | -8.4 | 1.9 | -0.4 | 0.2 | 2.7 | 2.0 | 3.2 | 4.7 | 1.4 | 18.0 | -12.6 |

| 2005 | -3.5 | 6.6 | -2.0 | -3.1 | 1.7 | 3.0 | 6.3 | 1.0 | 3.8 | -4.7 | 3.1 | 3.7 | 16.3 | -7.8 |

| 2006 | 8.9 | -3.6 | 3.6 | 2.4 | -4.8 | 1.1 | 2.8 | 0.5 | -0.8 | 3.3 | 3.4 | 2.0 | 19.7 | -11.9 |

| 2007 | 3.2 | -2.3 | -0.6 | 1.4 | 0.8 | -1.6 | -1.4 | 0.7 | 4.0 | 8.9 | -1.4 | 1.7 | 13.8 | -12.2 |

| 2008 | 2.5 | 4.1 | 0.2 | 1.0 | 2.7 | 0.7 | -3.0 | -1.4 | -3.7 | -2.3 | 3.9 | 5.1 | 9.9 | -13.8 |

| 2009 | -2.7 | -0.7 | 1.1 | -0.6 | -0.3 | -1.3 | 4.5 | 0.8 | 7.4 | -2.6 | 5.7 | 2.0 | 13.5 | -7.7 |

| 2010 | -7.1 | 2.8 | 8.2 | 1.7 | -7.6 | -0.3 | 3.7 | -0.4 | 5.3 | 3.0 | -1.1 | 3.6 | 11.3 | -14.2 |

| 2011 | 2.9 | 4.2 | 0.5 | 4.4 | -1.7 | -2.7 | 3.1 | -0.5 | -4.0 | -0.4 | -1.3 | 1.4 | 5.6 | -11.2 |

| 2012 | 2.6 | 0.6 | 0.6 | 1.5 | -2.7 | -0.1 | 1.5 | 0.0 | 0.1 | -1.1 | 0.5 | 1.3 | 4.7 | -5.0 |

| 2013 | 1.9 | 0.3 | 2.4 | 3.2 | -3.7 | -2.4 | 2.1 | -3.7 | 2.0 | 2.8 | 0.9 | 1.2 | 6.9 | -9.4 |

| 2014 | -2.5 | 1.9 | 0.5 | 1.5 | 1.0 | 1.8 | -1.2 | 3.3 | -5.4 | 1.6 | 1.3 | 0.6 | 4.2 | -6.7 |

| 2015 | 4.5 | -2.5 | 0.3 | -2.3 | -1.2 | -1.5 | 1.1 | -2.2 | 0.6 | 0.0 | -0.5 | 0.5 | -3.4 | -9.6 |

| 2016 | -0.4 | 0.8 | 0.4 | -0.8 | 1.2 | 1.9 | 3.2 | -3.0 | ||||||

| Avg | 0.9 | 1.2 | 0.9 | 0.3 | -0.4 | 0.5 | 1.2 | 0.3 | 1.3 | 0.8 | 1.4 | 2.5 | 10.8 | -8.3 |

#Trades for strategy :

| strategy | weight | entry.date | exit.date | nhold | entry.price | exit.price | return |

|---|---|---|---|---|---|---|---|

| CASH | 100 | 2015-08-31 | 2015-09-30 | 30 | 80.38 | 80.87 | 0.6 |

| CASH | 100 | 2015-09-30 | 2015-10-30 | 30 | 80.87 | 80.89 | 0.03 |

| REAL.ESTATE | 33.3 | 2015-10-30 | 2015-11-30 | 31 | 77.22 | 76.74 | -0.21 |

| CASH | 66.7 | 2015-10-30 | 2015-11-30 | 31 | 80.89 | 80.57 | -0.26 |

| REAL.ESTATE | 33.3 | 2015-11-30 | 2015-12-31 | 31 | 76.74 | 78.14 | 0.61 |

| CASH | 66.7 | 2015-11-30 | 2015-12-31 | 31 | 80.57 | 80.43 | -0.12 |

| REAL.ESTATE | 33.3 | 2015-12-31 | 2016-01-29 | 29 | 78.14 | 75.46 | -1.15 |

| CASH | 66.7 | 2015-12-31 | 2016-01-29 | 29 | 80.43 | 81.39 | 0.8 |

| CASH | 100 | 2016-01-29 | 2016-02-29 | 31 | 81.39 | 82.09 | 0.85 |

| US.10YR.GOV.BOND | 33.3 | 2016-02-29 | 2016-03-31 | 31 | 109.92 | 109.85 | -0.02 |

| CASH | 66.7 | 2016-02-29 | 2016-03-31 | 31 | 82.09 | 82.65 | 0.45 |

| US.10YR.GOV.BOND | 33.3 | 2016-03-31 | 2016-04-29 | 29 | 109.85 | 109.68 | -0.05 |

| REAL.ESTATE | 33.3 | 2016-03-31 | 2016-04-29 | 29 | 83.05 | 81.1 | -0.78 |

| CASH | 33.3 | 2016-03-31 | 2016-04-29 | 29 | 82.65 | 82.81 | 0.06 |

| US.STOCKS | 33.3 | 2016-04-29 | 2016-05-31 | 32 | 105.51 | 107.34 | 0.58 |

| US.10YR.GOV.BOND | 33.3 | 2016-04-29 | 2016-05-31 | 32 | 109.68 | 109.57 | -0.03 |

| REAL.ESTATE | 33.3 | 2016-04-29 | 2016-05-31 | 32 | 81.1 | 82.92 | 0.75 |

| US.10YR.GOV.BOND | 33.3 | 2016-05-31 | 2016-06-24 | 24 | 109.57 | 112.21 | 0.8 |

| REAL.ESTATE | 33.3 | 2016-05-31 | 2016-06-24 | 24 | 82.92 | 84.86 | 0.78 |

| CASH | 33.3 | 2016-05-31 | 2016-06-24 | 24 | 82.8 | 83.7 | 0.36 |

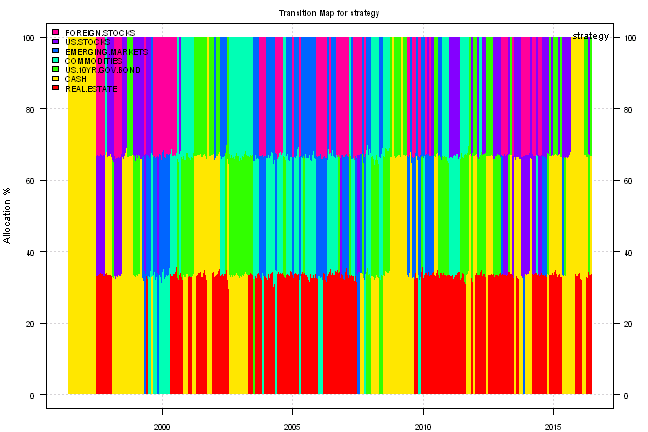

#Signals for strategy :

| US.STOCKS | FOREIGN.STOCKS | EMERGING.MARKETS | US.10YR.GOV.BOND | REAL.ESTATE | COMMODITIES | CASH | |

|---|---|---|---|---|---|---|---|

| 2014-10-30 | 0 | 0 | 0 | 33 | 33 | 0 | 33 |

| 2014-11-26 | 33 | 0 | 0 | 0 | 33 | 0 | 33 |

| 2014-12-30 | 0 | 0 | 0 | 33 | 33 | 0 | 33 |

| 2015-01-29 | 0 | 0 | 0 | 33 | 33 | 0 | 33 |

| 2015-02-26 | 33 | 0 | 0 | 0 | 33 | 0 | 33 |

| 2015-03-30 | 0 | 0 | 0 | 33 | 33 | 0 | 33 |

| 2015-04-29 | 33 | 0 | 33 | 0 | 0 | 0 | 33 |

| 2015-05-28 | 33 | 0 | 0 | 33 | 0 | 0 | 33 |

| 2015-06-29 | 33 | 0 | 0 | 0 | 0 | 0 | 67 |

| 2015-07-30 | 33 | 0 | 0 | 0 | 0 | 0 | 67 |

| 2015-08-28 | 0 | 0 | 0 | 0 | 0 | 0 | 100 |

| 2015-09-29 | 0 | 0 | 0 | 0 | 0 | 0 | 100 |

| 2015-10-29 | 0 | 0 | 0 | 0 | 33 | 0 | 67 |

| 2015-11-27 | 0 | 0 | 0 | 0 | 33 | 0 | 67 |

| 2015-12-30 | 0 | 0 | 0 | 0 | 33 | 0 | 67 |

| 2016-01-28 | 0 | 0 | 0 | 0 | 0 | 0 | 100 |

| 2016-02-26 | 0 | 0 | 0 | 33 | 0 | 0 | 67 |

| 2016-03-30 | 0 | 0 | 0 | 33 | 33 | 0 | 33 |

| 2016-04-28 | 33 | 0 | 0 | 33 | 33 | 0 | 0 |

| 2016-05-27 | 0 | 0 | 0 | 33 | 33 | 0 | 33 |

For your convenience, the Strategy-EAA report can also be downloaded and viewed the pdf format.

(this report was produced on: 2016-06-25)